地域暖房:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

District Heating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689777

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

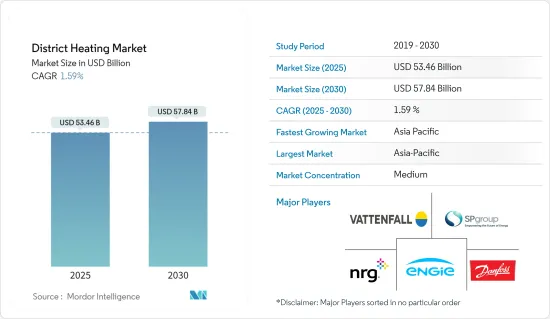

地域暖房の市場規模は2025年に534億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは1.59%で、2030年には578億4,000万米ドルに達すると予測されます。

地域エネルギーは、世界経済が設定した積極的な気候目標に支えられ、世界的に急成長している産業です。初期の評価によると、これらの地域冷暖房会社は、別の保有構造によって、より驚異的な成長と価値の可能性を生み出す事業として認識されています。地域暖房の供給に電動ヒートポンプを含めることで、より高い再生可能エネルギーレベルを熱目的に利用することができ、エネルギーシステム間の統合とバランスを生み出すことができます。世界的に風力タービンの生産能力が急増している中、大型ヒートポンプは、持続的なグリーンエネルギー開発と2050年までの化石燃料からの脱却において重要な役割を果たすと思われます。

主なハイライト

- 地域暖房は、高断熱パイプラインの配電網を通じて、熱エネルギーを温水の形で建物(住宅や商業施設)に供給する方法です。産業プロセスの地域暖房への転換は、産業やプロセスの種類によって熱負荷が異なるため、産業用地域暖房の利用拡大の可能性は限られています。

- しかし、地域暖房への転換は、電気の使用を11%、化石燃料の使用を40%削減し、産業界全体の最終エネルギー使用量を6%削減しました。

- 産業プロセスの転換により、全世界の二酸化炭素排出量を年間11万2,000トン削減できる可能性があります。しかし、住宅・商業市場が大きなシェアを占めると予想されます。

- 約6,000万人のEU市民が地域暖房を利用しており、さらに1億4,000万人が、少なくとも1つの地域暖房システムがある都市に住んでいます。EUとIEAの報告によると、DHは6,000の地域冷暖房ネットワークを介してEUの熱需要の約11~12%を満たしています。

- 機械学習により、顧客データと運転データから熱負荷を予測し、天気予報、祝日、平日などのデータと合わせて、熱生産を最適化し計画することで、熱損失を減らし、ピーク負荷に対応することです。この可能性は、漏水、非効率的な暖房システム、または単一部品に関連する故障によるエラーを特定するための故障検出におけるインテリジェント・アルゴリズムにまで拡大されます。

- 2024年6月、スウェーデンのSMRプロジェクト開発会社カーンフル・ネクストは、スウェーデンの地域暖房にSMRを導入するため、フィンランドのSteady Energy社と戦略的に提携しました。この提携は、カルンフル独自の資金調達構造と供給モデルを活用し、Steady Energyの有名な地域暖房用原子炉をスウェーデン市場に導入することを目的としています。

地域暖房市場の動向

住宅が成長を牽引

- 地域暖房は、世界中の先進国で一般的に使用されています。地域暖房には、安全性と信頼性の向上、低排出ガス、燃料の柔軟性向上(特にバイオマスやゴミなどの代替燃料を利用する場合)など、個別の建物設備に比べていくつかの利点があります。

- 地域暖房は、一戸建て住宅、集合住宅、高層ビル、メガタウンシップなどで広く利用されています。地域暖房を必要とする主な住宅用途は、空間暖房と給湯です。地域暖房市場は、デンマーク、アイスランド、ドイツ、米国、その他のEU諸国、カナダなど、寒冷気候の国々で確立されています。

- しかし、再生可能エネルギー源を動力源とする地域暖房ネットワークは、排出量を大幅に削減し、政府が排出削減目標を達成するのに役立つ可能性があります。様々な政府が、補助金、助成金、エネルギー税などの法的責任やインセンティブを設け、熱発電における再生可能エネルギーの割合を高めています。

- さらに、地域暖房は、以前は主に発電所、廃棄物発電施設、産業活動の製品別を利用していました。しかし、スウェーデンは現在、より多くの再生可能エネルギーを取り入れています。競合により、この地域密着型の電力は、全国トップの家庭用暖房産業に上り詰めました。

- BDHによると、2023年、ドイツではおよそ79万500台のガス暖房システムが販売されました。このうち、約9万4,000台が従来の低温技術を採用し、69万6,500台以上がコンデンシングボイラー技術を選択しています。

アジア太平洋地域が地域暖房市場で大きなシェアを占める

- 中国市場の成長を牽引している主な理由は、可処分所得の増加、CO2排出に関する懸念の増大、冷暖房システムの高い使用率です。さらにOECDは、インドと中国の一人当たりGDPが2060年までに7倍になると予測しています。

- アジア太平洋地域の政府も、地元企業と協力して家庭用市場を開拓しています。例えば、北京区暖房集団は中国の大手暖房会社です。同社は、北京中央政府と軍隊、中国大使館、重要な企業や組織、一般市民に暖房ソリューションを提供しています。また、他の省でも多数のプロジェクトを抱えています。

- 近代的な地域暖房システムは、大気汚染が長期的な経済的出費と数十万人の早期死亡の原因となっている東南アジア諸国にとって特に重要です。東南アジアにおける冷房の未来』では、2040年までに予想されるエネルギー消費、ピーク電力需要、CO2排出量の伸びを調査しています。

- インドとオーストラリアは、この地域の2大マーケットプレースです。この地域市場は、地域冷暖房ソリューションへの投資の増加や、これらのソリューションを促進するための政府活動の活発化によって上昇しています。

- エネルギー危機と気候変動に対応するため、韓国政府はゼロ・エネルギー・ビルディングを推進する国家計画を策定し、最近の動向では、これらの計画を達成するため、新築および既存の建物に対するいくつかのエネルギー効率化政策が策定されています。

地域暖房産業の概要

地域暖房市場の競争は緩やかで、多くの世界企業や地域企業が存在します。これらの企業は、世界的に消費者層を広げようと懸命に努力しています。予測期間中に競争上の優位性を獲得するため、革新的ソリューションの開発における研究開発費、戦略的提携、その他の有機的・無機的成長戦術も優先しています。

2023年5月、バッテンフォールABとコカ・コーラは、スウェーデンでの協業を発表し、2040年までにバリューチェーン全体でネット・ゼロ・エミッションを達成するという野心的な気候変動目標を設定しました。両社は、電気輸送の電力需要を満たすため、3つの充電ステーションを備えたパイロット・プロジェクトを開始しました。

2023年3月、NRGエナジー社はビビント・スマートホーム社の買収を完了し、NRGの消費者重視の成長戦略を加速させ、消費者に家庭の電力供給、保護、管理をインテリジェントに行うシンプルでコネクテッドな体験を提供します。NRGはエネルギーと家庭向けサービスの交差点に位置し、卓越した顧客経験に支えられた独自のエンド・ツー・エンドのスマートホーム・エコシステムを提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の市場への影響

- 地域暖房移行に関する政府の取り組みとプログラム

- 地域暖房の主要動向とイノベーション

第5章 市場力学

- 市場促進要因

- エネルギー効率が高く費用対効果の高い暖房システムに対する需要の高まり

- 都市化と工業化の進展

- 市場抑制要因

- 高いインフラコスト

第6章 市場セグメンテーション

- プラントタイプ別

- ボイラー

- 熱電併給(CHP)

- 熱源別

- 石炭

- 天然ガス

- 再生可能エネルギー

- 石油・石油製品

- 用途別

- 住宅

- 商業・工業

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Vattenfall AB

- SP Group

- Danfoss Group

- Engie

- NRG Energy Inc.

- Statkraft AS

- Logstor AS

- Shinryo Corporation

- Vital Energi Ltd

- Gteborg Energi

- Alfa Laval AB

- Ramboll Group AS

- Keppel Corporation Limited

- FVB Energy

第8章 投資分析

第9章 将来の機会

目次

The District Heating Market size is estimated at USD 53.46 billion in 2025, and is expected to reach USD 57.84 billion by 2030, at a CAGR of 1.59% during the forecast period (2025-2030).

District energy is a quick-growing industry globally, supported by the aggressive climate objectives set by the global economies. Based on initial assessments, these district heating and cooling companies have been recognized as operations that could produce more extraordinary growth and value potential with an alternative holding structure. By including electrically powered heat pumps in the district heating supply, higher renewable energy levels can be used for thermal purposes, generating integration and balance between energy systems. With a burgeoning global wind turbine capacity, big heat pumps will play a meaningful role in the sustained global green energy development and phasing out fossil fuels by 2050.

Key Highlights

- District heating provides a method of delivering thermal energy to buildings (homes and commercial space) in the form of hot water through a distribution network of highly insulated pipelines. The potential for increased use of industrial district heating is limited because conversions of industrial processes to district heating involve varying heat loads amongst types of industries and processes.

- However, the conversion to district heating serves an 11% reduction in the use of electricity and a 40% reduction in the use of fossil fuels, with a total energy end-use saving of 6% among industries.

- Converting the industrial processes has led to a potential reduction of global carbon dioxide emissions by 112,000 tons per year. However, the residential and commercial markets are expected to hold a significant share.

- Approximately 60 million EU citizens are served by district heating, and an additional 140 million people live in cities with at least one district heating system. According to reports by the EU and the IEA, DH meets around 11-12% of the EU's heat demand via 6,000 district heating and cooling networks.

- With machine learning, the idea is to predict heat loads from customer data and operational data, along with weather forecasts, national holidays, weekdays, etc., to optimize and plan heat production, thereby lowering heat loss and handling peak loads. The potential is extended to intelligent algorithms in fault detection to identify leakages, inefficient heating systems, or errors from failure related to single components.

- In June 2024, Swedish SMR project developer Karnfull Next has strategically partnered with Finnish counterpart Steady Energy to introduce SMRs for district heating in Sweden. The collaboration aims to capitalize on Karnfull's unique financing structures and delivery models to introduce Steady Energy's renowned district heating reactors to the Swedish market.

District Heating Market Trends

Residential to Witness the Growth

- District heating is commonly used in industrialized nations worldwide. It has several advantages over individual building equipment, including improved safety and dependability, lower emissions, and greater fuel flexibility, particularly when utilizing alternative fuels such as biomass or garbage.

- District heating is widely utilized in single-family houses, multi-family dwellings, high-rise buildings, and mega townships. The primary home uses that require district heating are space and water heating. District heating markets are well-established in several cold-climate nations, such as Denmark, Iceland, Germany, the United States, other EU countries, and Canada.

- However, the District heating networks powered by renewable energy sources may significantly reduce emissions and help governments meet their emission reduction objectives. Various governments have established statutory responsibilities and incentives, such as grants, subsidies, and energy taxes, to boost the percentage of renewables in heat generation.

- Moreover, District heating was previously primarily powered by byproducts of power plants, waste-to-energy facilities, and industrial activities. However, Sweden is now incorporating more renewable energy sources into the mix. Due to competition, this localized kind of electricity has risen to the national top home-heating industry.

- According to BDH, in 2023, Germany saw sales of approximately 790,500 gas heating systems. Among these, approximatly 94,000 employed traditional low-temperature technology, with the majority, over 696,500, opting for condensing boiler technology.

Asia-Pacific Holds a Significant Share in the District Heating Market

- The primary reasons driving the market's growth in China are rising disposable income, increased worries about CO2 emissions, and high usage of heating and cooling systems. Moreover, OECD states that projections for India and China's per capita GDP might climb sevenfold by 2060.

- Governments in the Asia-Pacific region are also collaborating with local businesses to develop the home market. For example, the Beijing District Heating Group is a major heating firm in China. The firm provided heating solutions to the central Beijing government and army, Chinese embassies, significant corporations and organizations, and the general people. It also has a large number of projects in other provinces.

- Modern district heating systems are especially important for Southeast Asian countries, where air pollution causes long-term economic expenses and hundreds of thousands of premature fatalities. The Future of Cooling in Southeast Asia investigates the anticipated growth in energy consumption, peak power demand, and CO2 emissions by 2040.

- India and Australia are two of the region's biggest marketplaces. The regional market is rising due to increased investment in district heating and cooling solutions and increased government activities to promote these solutions.

- To respond to energy crises and climate change, the South Korean government established a national plan to promote zero energy buildings, and several energy efficiency policies for new and existing buildings in recent years have been developed to achieve these plans.

District Heating Industry Overview

The district heating market is moderately competitive and has many global and regional players. These companies are working hard to broaden their consumer base globally. To gain a competitive advantage during the predicted term, they also prioritize R&D expenditure in developing innovative solutions, strategic collaborations, and other organic and inorganic growth tactics.

In May 2023, Vattenfall AB and Coca-Cola announced the collaboration in Sweden and have set ambitious climate targets for net zero emissions across their entire value chains by 2040. The companies have initiated a pilot project with three charging stations to meet the need for powering electric transport.

In March 2023, NRG Energy Inc completed its acquisition of Vivint Smart Home, Inc. by accelerating NRG's consumer-focused growth strategy and offering consumers simple, connected experiences to power, protect, and manage their homes intelligently. NRG is at the intersection of energy and home services, with a unique end-to-end smart home ecosystem underpinned by our exceptional customer experience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

- 4.5 Government Initiatives and Programs on District Heating Transition

- 4.6 Key Trends and Innovations in District Heating

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Augmented Demand for Energy-efficient and Cost-effective Heating Systems

- 5.1.2 Rising Urbanization and Industrialization

- 5.2 Market Restraints

- 5.2.1 High Infrastructure Cost

6 MARKET SEGMENTATION

- 6.1 By Plant Type

- 6.1.1 Boiler

- 6.1.2 Combined Heat and Power (CHP)

- 6.2 By Heat Source

- 6.2.1 Coal

- 6.2.2 Natural Gas

- 6.2.3 Renewables

- 6.2.4 Oil and Petroleum Products

- 6.3 By Application

- 6.3.1 Residential

- 6.3.2 Commercial and Industrial

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Vattenfall AB

- 7.1.2 SP Group

- 7.1.3 Danfoss Group

- 7.1.4 Engie

- 7.1.5 NRG Energy Inc.

- 7.1.6 Statkraft AS

- 7.1.7 Logstor AS

- 7.1.8 Shinryo Corporation

- 7.1.9 Vital Energi Ltd

- 7.1.10 Gteborg Energi

- 7.1.11 Alfa Laval AB

- 7.1.12 Ramboll Group AS

- 7.1.13 Keppel Corporation Limited

- 7.1.14 FVB Energy

8 INVESTMENT ANALYSIS

9 FUTURE OPPORTUNITIES

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日