|

市場調査レポート

商品コード

1666908

地域暖房パイプラインネットワークの市場機会、成長促進要因、産業動向分析、2025~2034年予測District Heating Pipeline Network Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 地域暖房パイプラインネットワークの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2024年12月16日

発行: Global Market Insights Inc.

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

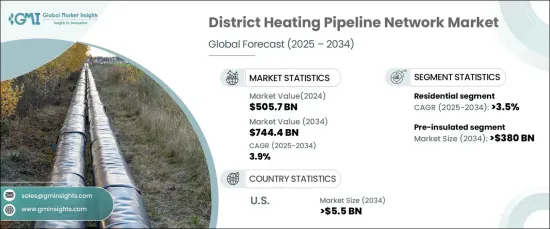

世界の地域暖房パイプラインネットワーク市場は、2024年に5,057億米ドルと評価され、2025年から2034年にかけて3.9%のCAGRで安定成長すると予測されています。

この成長は、持続可能なエネルギー技術への転換と、エネルギー効率の高い暖房システムへの需要の高まりを反映しています。地域暖房パイプラインは、熱損失を減らし、省エネルギーを改善し、世界の持続可能性目標に沿うことで、現代のエネルギー課題に対する解決策を提供します。

都市人口が拡大し、各国政府がエネルギー基準を厳格化するにつれ、地域暖房ソリューションの採用は加速しています。これらのシステムはエネルギー効率を高めるだけでなく、二酸化炭素排出量を大幅に削減するため、スマートシティ構想の要となっています。バイオマス、太陽熱、地熱などの再生可能エネルギーを統合できることから、強靭で環境に優しいインフラを構築する上で、その重要性が強調されています。さらに、エネルギーコストの削減や長期的な運用効率といった経済的メリットもあり、地域暖房パイプラインは世界中の住宅、商業、工業用途にとって魅力的な投資先となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 5,057億米ドル |

| 予測金額 | 7,444億米ドル |

| CAGR | 3.9% |

地域暖房用パイプラインネットワークは、持続可能なインフラへの投資の増加により、2034年までに3,800億米ドルを生み出すと予測されています。これらのパイプラインは高温に耐え、比類のない耐久性を実現するよう設計されているため、大規模な暖房が必要な地域に最適です。その革新的な設計は熱損失を最小限に抑え、エネルギー消費を最適化し、大規模な都市プロジェクトをサポートします。開発者がエネルギー効率の高い技術を優先する中、プレインシュレーテッドパイプラインは、近代的で持続可能な暖房システムの代名詞となっています。熱効率の低下を抑え、温室効果ガスの排出量を削減するパイプラインの役割は、環境基準の達成を目指す都市にとって極めて重要なソリューションとなっています。

住宅分野では、地域暖房パイプライン市場は2034年まで3.5%の成長率が予測されています。人口密度の高い都市部では、環境に優しい暖房ソリューションへの嗜好が高まっていることが、この成長を後押しする重要な要因となっています。地域暖房システムは、家庭の暖房と給湯にシームレスで費用対効果の高い方法を提供する一方、個々の暖房ユニットへの依存を軽減します。再生可能エネルギー源との互換性がさらにその魅力を高め、家庭がより環境に優しいエネルギーオプションへと移行することを可能にします。政府がカーボンニュートラルとエネルギー効率を重視する中、地域暖房システムの住宅採用は急増し、将来の都市計画に不可欠な要素となることが予想されます。

米国では、地域暖房パイプラインネットワーク市場は2034年までに55億米ドルを生み出すと予測されています。都市開発とエネルギー効率の高いインフラへの多額の投資が、この成長を後押ししています。全国の都市は、エネルギー義務化と脱炭素化の目標を達成するため、先進的な地域暖房システムを導入しています。熱損失を削減し、運転効率を向上させることができるプレインシュレーテッドパイプラインは、都市暖房プロジェクトに不可欠なものとなりつつあります。自治体が温室効果ガス排出量の削減や再生可能エネルギーの導入に努める中、最先端の暖房ソリューションに対する需要は高まり続けており、米国は地域暖房ネットワークにとって極めて重要な市場となっています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:パイプ別、2021~2034年

- 主要動向

- プレインシュレーテッドパイプライン

- ポリマー

第6章 市場規模・予測:直径別、2021~2034年

- 主要動向

- 20~100 mm

- 101~300 mm

- 300 mm以上

第7章 市場規模・予測:用途別、2021~2034年

- 主要動向

- 住宅用

- 商業用

- 産業用

第8章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- ポーランド

- スウェーデン

- ロシア

- イタリア

- 英国

- フィンランド

- デンマーク

- アジア太平洋

- 中国

- 日本

- 韓国

第9章 企業プロファイル

- Aquatherm

- Brugg Pipes

- CPV

- Golan Plastic Products

- Isoplus

- Ke Kelit

- Logstor

- Mannesmann Line Pipe

- Microflex

- Perma-Pipe

- Pipelife

- Rehau

- Thermaflex

- Uponor

The Global District Heating Pipeline Network Market, valued at USD 505.7 billion in 2024, is set to grow at a steady CAGR of 3.9% between 2025 and 2034. This growth reflects a transformative shift toward sustainable energy technologies and a heightened demand for energy-efficient heating systems. District heating pipelines offer a solution to modern energy challenges by reducing heat loss, improving energy conservation, and aligning with global sustainability goals.

As urban populations expand and governments enforce stricter energy standards, the adoption of district heating solutions is poised to accelerate. These systems not only enhance energy efficiency but also significantly lower carbon emissions, making them a cornerstone of smart city initiatives. Their ability to integrate renewable energy sources such as biomass, solar thermal, and geothermal energy underscores their importance in creating resilient, eco-friendly infrastructure. Furthermore, the economic benefits-reduced energy costs and long-term operational efficiency-make district heating pipelines an attractive investment for residential, commercial, and industrial applications worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $505.7 Billion |

| Forecast Value | $744.4 Billion |

| CAGR | 3.9% |

The pre-insulated district heating pipeline network is anticipated to generate USD 380 billion by 2034, driven by increasing investments in sustainable infrastructure. These pipelines are engineered to endure high temperatures and deliver unmatched durability, making them ideal for regions with extensive heating requirements. Their innovative design minimizes heat loss, optimizes energy consumption, and supports large-scale urban projects. As developers prioritize energy-efficient technologies, pre-insulated pipelines have become synonymous with modern, sustainable heating systems. Their role in reducing thermal inefficiencies and lowering greenhouse gas emissions positions them as a pivotal solution for cities aiming to achieve environmental benchmarks.

In the residential sector, the district heating pipeline market is projected to grow at a rate of 3.5% through 2034. The rising preference for eco-friendly heating solutions in densely populated urban areas is a key factor propelling this growth. District heating systems provide a seamless and cost-effective method for heating homes and supplying hot water while reducing reliance on individual heating units. Their compatibility with renewable energy sources further enhances their appeal, enabling households to transition toward greener energy options. With governments emphasizing carbon neutrality and energy efficiency, residential adoption of district heating systems is expected to surge, making them an integral part of future urban planning.

In the United States, the district heating pipeline network market is forecasted to generate USD 5.5 billion by 2034. Significant investments in urban development and energy-efficient infrastructure are driving this growth. Cities across the country are implementing advanced district heating systems to meet energy mandates and decarbonization goals. Pre-insulated pipelines, with their ability to reduce thermal losses and improve operational efficiency, are becoming indispensable for urban heating projects. As municipalities strive to lower greenhouse gas emissions and incorporate renewable energy into their frameworks, the demand for cutting-edge heating solutions continues to rise, positioning the US as a pivotal market for district heating networks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Pipe, 2021 – 2034 (km & USD Billion)

- 5.1 Key trends

- 5.2 Pre-insulated steel

- 5.3 Polymer

Chapter 6 Market Size and Forecast, By Diameter, 2021 – 2034 (km & USD Billion)

- 6.1 Key trends

- 6.2 20-100 mm

- 6.3 101-300 mm

- 6.4 ≥300 mm

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (km & USD Billion)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (km & USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 Poland

- 8.3.3 Sweden

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 UK

- 8.3.7 Finland

- 8.3.8 Denmark

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

Chapter 9 Company Profiles

- 9.1 Aquatherm

- 9.2 Brugg Pipes

- 9.3 CPV

- 9.4 Golan Plastic Products

- 9.5 Isoplus

- 9.6 Ke Kelit

- 9.7 Logstor

- 9.8 Mannesmann Line Pipe

- 9.9 Microflex

- 9.10 Perma-Pipe

- 9.11 Pipelife

- 9.12 Rehau

- 9.13 Thermaflex

- 9.14 Uponor