|

市場調査レポート

商品コード

1892864

STEM玩具市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測STEM Toys Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| STEM玩具市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年12月03日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

概要

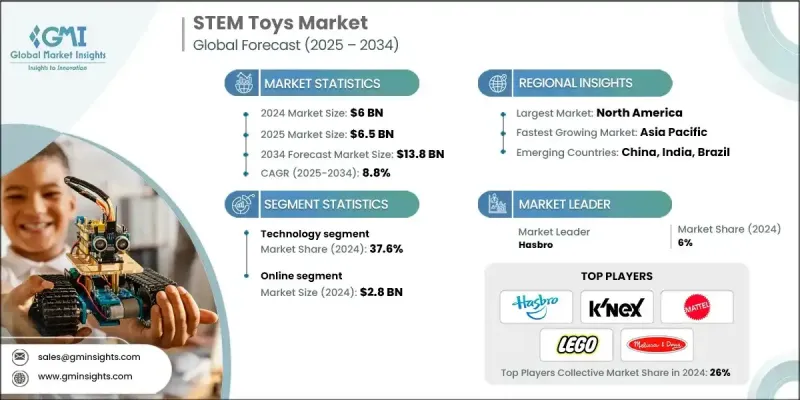

世界のSTEM玩具市場は、2024年に60億米ドルと評価され、2034年までにCAGR8.8%で成長し、138億米ドルに達すると予測されています。

この市場拡大は、子どもの批判的思考力、創造性、問題解決能力を育む玩具に対する保護者や教育関係者の関心の高まりに牽引されています。STEMベースの製品が世界的に注目を集める中、娯楽玩具メーカーは教育玩具やインタラクティブ玩具をラインナップに追加し、製品ポートフォリオの多様化を加速させています。伝統的な遊びとSTEM学習を組み合わせることで、企業は娯楽性と教育性の両立を実現し、娯楽と並行してスキル育成を重視する保護者のニーズに応えています。STEM玩具を他の人気子供向け製品と統合することで、製品の価値認識が高まり、情報に基づいた購買判断が促進され、販売数量も増加します。教育と娯楽の融合は、学習とレジャーの両方の機会を提供する革新的で魅力的な玩具に対する強い市場需要を生み出しており、STEM玩具は世界中のメーカーにとって重要な焦点となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年度 | 2025-2034 |

| 開始時価値 | 60億米ドル |

| 予測金額 | 138億米ドル |

| CAGR | 8.8% |

技術分野は2024年に37.6%のシェアを占めました。工学ベースのおもちゃは、子どもたちが積極的に創造し、実験し、問題を解決することを可能にし、実践的で多感覚的な学習体験を提供します。これらの製品はまた、共同遊びを促進し、建設や工学の課題に取り組む中で、子どもたちがコミュニケーション能力やチームワークスキルを育むのに役立ちます。

オンライン販売セグメントは2024年に28億米ドルの売上を生み出しました。eコマースプラットフォームにより、メーカーは顧客との直接的な関係を維持し、パーソナライズされたパッケージを提供し、統合サービスを実現できます。オンラインチャネルはまた、企業が貴重な消費者インサイトを収集し、アフターサポートを改善し、サービス契約や部品供給を通じて顧客生涯価値を最大化する手段となります。

米国STEM玩具市場は2024年に84.5%のシェアを占め、18億米ドルの収益を貢献しました。同地域の堅牢な物流インフラ、高い技術導入率、革新的な教育玩具に対する強い消費者需要が、世界をリードする市場としての地位を確立しています。政府主導の施策や教育プログラムがSTEM学習を継続的に推進しており、市場のさらなる成長を支えています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 早期教育に対する保護者の関心の高まり

- 先進技術(AI/ML/AR)の統合

- 政府の取り組みとカリキュラムの整合性

- 業界の潜在的リスク&課題

- 高度なロボット工学およびコーディングキットの高コスト

- 画面ベースのデジタルエンターテインメントとの競合

- 機会

- 新興経済国における未開拓市場

- 物理的遊びとデジタル遊びの融合(STEAM)

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 規制情勢

- 規格およびコンプライアンス要件

- 地域別規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 科学

- 技術

- エンジニアリング

- 数学

第6章 市場推計・予測:年齢層別、2021-2034

- 主要動向

- 0~3歳

- 3~8歳

- 8~12歳

- 12歳以上

第7章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- オンライン

- オフライン

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- BanBao

- Bandai

- Gigotoys

- Goldlok Toys

- Guangdong Loongon

- Guangdong Qman Culture Communication

- Hasbro

- K’NEX

- LEGO Group

- Mattel

- Melissa and Doug

- ShanTou LianHuan Toys and Crafts

- Spin Master

- TAKARA TOMY

- Vtech