|

|

市場調査レポート

商品コード

1429254

核融合市場:現状分析と予測(2030-2040年)Nuclear Fusion Market: Current Analysis and Forecast (2030-2040) |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 核融合市場:現状分析と予測(2030-2040年) |

|

出版日: 2024年01月30日

発行: UnivDatos Market Insights Pvt Ltd

ページ情報: 英文 147 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 目次

核融合市場は、原子力エネルギーに対する政府資金の増加により、CAGR約6%の安定した成長が見込まれています。さらに、持続可能なエネルギー源に対するニーズの高まり、気候変動や化石燃料埋蔵量の枯渇に対する懸念の高まりにより、核融合は、排出物のない事実上無限のエネルギー供給を提供し、世界のエネルギー需要に対応する可能性があることから、主流に躍り出た。さらに、技術の進歩は、核融合の実現可能性と商業的実行可能性を著しく高めています。プラズマ閉じ込め、超伝導磁石、核融合炉の設計における革新は、より効率的でコンパクトな核融合炉の開発につながった。これらの技術的進歩は投資家の信頼を高め、この分野に多額の資金を引き寄せています。例えば、2022年12月、米国エネルギー省から核融合科学における重要な科学的進歩が発表されました。驚くべきことに、核融合反応を起こすのに必要なエネルギー量を上回るエネルギーが得られ、画期的な成果が示されました。

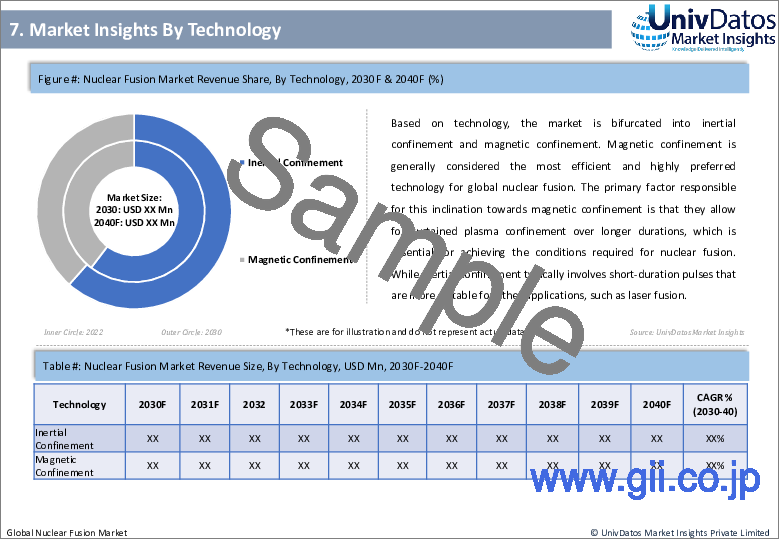

技術に基づき、市場は慣性閉じ込めと磁気閉じ込めに二分されます。磁場閉じ込めは、一般的に最も効率的で、世界の核融合に非常に好まれる技術と考えられています。磁場閉じ込めへの傾斜の主な要因は、磁場閉じ込めが、核融合に必要な条件を達成するために不可欠な、より長い時間にわたる持続的なプラズマ閉じ込めを可能にするからです。慣性閉じ込めが一般的に短時間のパルスを必要とするのに対し、磁気閉じ込めはレーザー核融合など他の応用に適しています。さらに、トカマクやステラレータのような磁気閉じ込め技術は拡張性が高く、より大型で強力な装置に発展させることができます。この拡張性により、長期的にはより大量の核融合エネルギーの生産が可能になります。これに加えて、磁場閉じ込め方式はプラズマの形状と安定性をよりよく制御できるため、より効率的な原子炉設計が可能になります。これにより、核融合反応を制御し、エネルギー出力を最大化する能力が高まる。

燃料に基づき、市場は重水素-三重水素、重水素、重水素ヘリウム3、陽子ホウ素に区分されます。現在、世界的に核融合に最も効率的で非常に好まれる燃料は、重水素-三重水素(D-T)燃料の組み合わせのようです。水素の同位体である重水素は、海水中で容易に入手できるため、豊富に存在します。一方、トリチウムは自然界に存在しないため、核融合炉内で生成または増殖させる必要があります。しかし、トリチウムは比較的豊富なリチウムから生成することができます。さらに、D-T核融合は核融合を達成するために必要な温度が最も低いため、他の燃料の組み合わせに比べて、核融合の達成と維持が比較的容易です。これに加えて、D-T核融合は他の燃料の組み合わせと比べて、単位質量あたりのエネルギー出力が最も高いです。この高いエネルギー出力は、商用核融合発電の燃料として好まれる一因となっています。

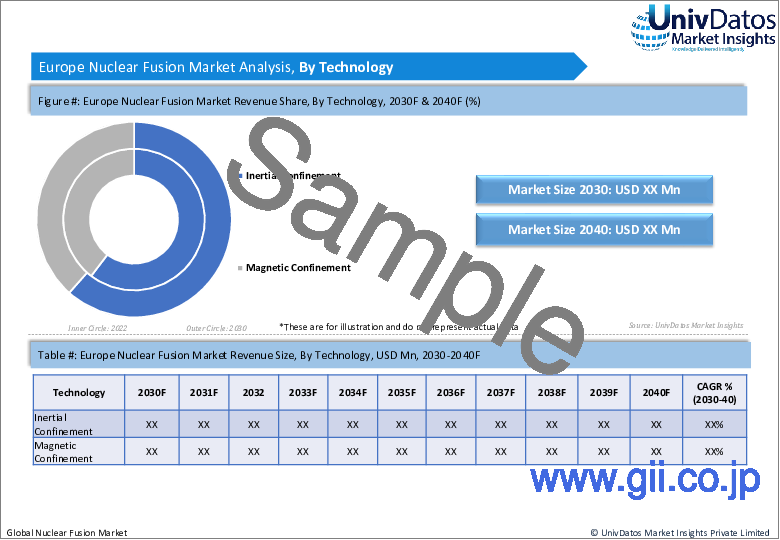

核融合の市場導入に関する理解を深めるため、市場は北米(米国、カナダ、その他北米地域)、欧州(ドイツ、英国、フランス、スペイン、イタリア、その他欧州地域)、アジア太平洋地域(中国、日本、インド、その他アジア太平洋地域)、世界のその他の地域における世界のプレゼンスに基づいて分析されています。欧州は目覚ましい発展を遂げ、核融合発電の領域におけるフロントランナーとして広く認知されています。この分野における欧州の進歩には数多くの要因が寄与しており、その顕著な例のひとつが国際熱核融合実験炉(ITER)です。ITERプロジェクトのホスト国として、欧州はフランスにある世界最大の核融合実験施設を誇っています。この協力的な試みには、欧州の数カ国を含む35カ国が参加しており、核融合研究のリーダーとしての欧州の地位を大幅に強化しています。さらに欧州は、核融合エネルギーの発展に尽力する研究機関や大学間の強固なパートナーシップを育んできました。欧州核融合開発協定(EFDA)とEUROfusionコンソーシアムは、このような協力関係の代表例であり、核融合エネルギーの発展のために科学者、技術者、リソースを結集しています。さらに、英国のジョイント・ヨーロピアン・トーラス(JET)やドイツのヴェンデルシュタイン7-X施設のような施設が、核融合研究における欧州のリーダーシップにおいて極めて重要な役割を果たしています。

目次

第1章 市場イントロダクション

- 市場の定義

- 主な目標

- ステークホルダー

- 制限事項

第2章 調査手法または前提

- 調査プロセス

- 調査手法

- 回答者プロファイル

第3章 市場要約

第4章 エグゼクティブサマリー

第5章 COVID-19が核融合市場に与える影響

第6章 核融合市場収益 , 2020-2030年

第7章 技術別の市場洞察

- 慣性閉じ込め

- 磁気閉じ込め

第8章 燃料別の市場洞察

- 重水素トリチウム

- 重水素

- 重水素ヘリウム3

- プロトンボロン

第9章 地域別の市場洞察

- 北米

- 米国

- カナダ

- その他北米地域

- 欧州

- ドイツ

- 英国。

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

第10章 核融合市場力学

- 市場促進要因

- 市場の課題

- 影響分析

第11章 核融合市場機会

第12章 核融合市場動向

第13章 需要側と供給側の分析

- 需要側分析

- 供給側分析

第14章 バリューチェーン分析

第15章 競合シナリオ

- 競合情勢

- ポーターのファイブフォース分析

第16章 企業プロファイル

- First Light Fusion Ltd

- Zap Energy Inc.

- Renaissance Fusion

- Lockheed Martin Corporation

- TAE Technologies, Inc.

- Commonwealth Fusion Systems

- Marvel Fusion GmbH

- General Fusion

- KYOTO FUSIONEERING LTD.

- Tokamak Energy Ltd

第17章 免責事項

Nuclear fusion, in the context of physics and energy production, refers to a process in which two or more atomic nuclei join together to form a new, heavier nucleus. This merging of atomic nuclei releases an immense amount of energy. It is the fundamental mechanism by which stars, including our Sun, generate heat and light. Nuclear fusion has the potential to revolutionize energy production due to numerous benefits. It produces vast amounts of energy, is virtually limitless in terms of fuel availability, and generates significantly less radioactive waste compared to nuclear fission (the splitting of heavy atomic nuclei). Furthermore, fusion reactions do not release greenhouse gases or contribute to the long-lived radioactive waste associated with conventional power sources.

The Nuclear Fusion Market is expected to grow at a steady CAGR of around 6% owing to the increased government funding for nuclear energy. Furthermore, the increasing need for sustainable energy sources and rising concerns over climate change and depleting fossil fuel reserves have catapulted nuclear fusion into the mainstream due to its potential to provide an emission-free, virtually limitless energy supply, addressing global energy demands. Moreover, advancements in technology have significantly enhanced the feasibility and commercial viability of nuclear fusion. Innovations in plasma confinement, superconducting magnets, and fusion reactor designs have led to the development of more efficient and compact fusion reactors. These technological advancements have bolstered investor confidence and attracted substantial funding to the sector. For instance, in December 2022, a significant scientific advancement in nuclear fusion science was announced by the U.S. Department of Energy. Remarkably, the fusion reaction yielded more energy than the amount required to initiate it, marking a groundbreaking achievement.

Based on technology, the market is bifurcated into inertial confinement and magnetic confinement. Magnetic confinement is generally considered the most efficient and highly preferred technology for global nuclear fusion. The primary factor responsible for this inclination towards magnetic confinement is that, they allow for sustained plasma confinement over longer durations, which is essential for achieving the conditions required for nuclear fusion. While inertial confinement typically involves short-duration pulses that are more suitable for other applications, such as laser fusion. Furthermore, magnetic confinement technologies, such as tokamaks and stellarators, are more scalable and can be developed into larger and more powerful devices. This scalability enables the production of more significant amounts of fusion energy in the long run. In addition to this, The magnetic confinement approach provides better control over the shape and stability of the plasma, allowing for more efficient reactor designs. This enhances the ability to control fusion reactions and maximize energy output.

Based on fuels, the market is segmented into deuterium-tritium, deuterium, deuterium helium3, and proton boron. The most efficient and highly preferred fuel for nuclear fusion globally currently seems to be the deuterium-tritium (D-T) fuel combination. Primary factors that are responsible for this include abundance, where deuterium, an isotope of hydrogen, is readily available in seawater, making it abundant. Tritium, on the other hand, is not naturally occurring and needs to be produced or bred within the fusion reactor. However, tritium can be bred from lithium, which is also relatively abundant. Furthermore, D-T fusion has the lowest temperature requirements for achieving fusion, making it relatively easier to achieve and sustain compared to other fuel combinations. In addition to this, D-T fusion offers the highest energy output per unit mass compared to other fuel combinations. This higher energy output contributes to its preference as a fuel for commercial fusion power generation.

For a better understanding of the market adoption of nuclear fusion, the market is analyzed based on its worldwide presence in countries such as North America (The U.S., Canada, and the Rest of North America), Europe (Germany, The U.K., France, Spain, Italy, Rest of Europe), Asia-Pacific (China, Japan, India, Rest of Asia-Pacific), Rest of World. Europe has made remarkable strides and is widely recognized as a frontrunner in the realm of nuclear fusion power generation. Numerous factors have contributed to Europe's progress in this domain, with one notable example being the International Thermonuclear Experimental Reactor (ITER). As the host of the ITER project, Europe boasts the world's largest experimental fusion facility, situated in France. This collaborative endeavor involves 35 countries, including several European nations, and has significantly bolstered Europe's position as a leader in nuclear fusion research. Moreover, Europe has fostered robust partnerships among research institutions and universities dedicated to advancing fusion energy. The European Fusion Development Agreement (EFDA) and the EUROfusion consortium are prime illustrations of such collaborations, uniting scientists, engineers, and resources for the advancement of fusion energy. Additionally, Europe's research infrastructure for nuclear fusion is firmly established, with facilities like the Joint European Torus (JET) in the United Kingdom and the Wendelstein 7-X facility in Germany playing pivotal roles in Europe's leadership in fusion research.

Some of the major players operating in the market include First Light Fusion Ltd; Zap Energy Inc.; Renaissance Fusion; Lockheed Martin Corporation; TAE Technologies, Inc.; Commonwealth Fusion Systems; Marvel Fusion GmbH; General Fusion; KYOTO FUSIONEERING LTD.; and Tokamak Energy Ltd

TABLE OF CONTENTS

1 MARKET INTRODUCTION

- 1.1. Market Definitions

- 1.2. Main Objective

- 1.3. Stakeholders

- 1.4. Limitation

2 RESEARCH METHODOLOGY OR ASSUMPTION

- 2.1. Research Process of the Nuclear Fusion Market

- 2.2. Research Methodology of the Nuclear Fusion Market

- 2.3. Respondent Profile

3 MARKET SYNOPSIS

4 EXECUTIVE SUMMARY

5 IMPACT OF COVID-19 ON THE NUCLEAR FUSION MARKET

6 NUCLEAR FUSION MARKET REVENUE (USD BN), 2020-2030F.

7 MARKET INSIGHTS BY TECHNOLOGY

- 7.1. Inertial Confinement

- 7.2. Magnetic Confinement

8 MARKET INSIGHTS BY FUELS

- 8.1. Deuterium tritium

- 8.2. Deuterium

- 8.3. Deuterium Helium3

- 8.4. Proton Boron

9 MARKET INSIGHTS BY REGION

- 9.1. North America

- 9.1.1. The U.S.

- 9.1.2. Canada

- 9.1.3. Rest of North America

- 9.2. Europe

- 9.2.1. Germany

- 9.2.2. The U.K.

- 9.2.3. France

- 9.2.4. Italy

- 9.2.5. Spain

- 9.2.6. Rest of Europe

- 9.3. Asia-Pacific

- 9.3.1. China

- 9.3.2. India

- 9.3.3. Japan

- 9.3.4. South Korea

- 9.3.5. Rest of Asia-Pacific

- 9.4. Rest of the World

10 NUCLEAR FUSION MARKET DYNAMICS

- 10.1. Market Drivers

- 10.2. Market Challenges

- 10.3. Impact Analysis

11 NUCLEAR FUSION MARKET OPPORTUNITIES

12 NUCLEAR FUSION MARKET TRENDS

13 DEMAND AND SUPPLY-SIDE ANALYSIS

- 13.1. Demand Side Analysis

- 13.2. Supply Side Analysis

14 VALUE CHAIN ANALYSIS

15 COMPETITIVE SCENARIO

- 15.1. Competitive Landscape

- 15.1.1. Porters Fiver Forces Analysis

16 COMPANY PROFILED

- 16.1. First Light Fusion Ltd

- 16.2. Zap Energy Inc.

- 16.3. Renaissance Fusion

- 16.4. Lockheed Martin Corporation

- 16.5. TAE Technologies, Inc.

- 16.6. Commonwealth Fusion Systems

- 16.7. Marvel Fusion GmbH

- 16.8. General Fusion

- 16.9. KYOTO FUSIONEERING LTD.

- 16.10. Tokamak Energy Ltd