|

|

市場調査レポート

商品コード

1494561

欧州のコネクテッド車両市場:2030年までの予測- 地域別分析- 技術、コネクティビティ、用途別Europe Connected Vehicle Market Forecast to 2030 - Regional Analysis - by Technology (5G, 4G/LTE, and 3G & 2G), Connectivity (Integrated, Tethered, and Embedded), and Application (Telematics, Infotainment, Driving Assistance, and Others) |

||||||

|

|||||||

|

|||||||

| 欧州のコネクテッド車両市場:2030年までの予測- 地域別分析- 技術、コネクティビティ、用途別 |

|

出版日: 2024年04月05日

発行: The Insight Partners

ページ情報: 英文 95 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

欧州のコネクテッド車両市場は、2022年に126億2,537万米ドルと評価され、2030年には464億3,082万米ドルに達すると予測され、2022年から2030年までのCAGRは17.7%を記録すると推定されます。

コネクティビティ技術の進歩が欧州のコネクテッド車両市場を促進

コネクティビティ技術の進歩は、自動車の展望を根本的に変えており、コネクテッド車両市場に与えるプラスの影響は顕著かつ広範囲に及んでいます。こうした進歩は、コネクティッド化が進む消費者の生活に自動車を適合させることで、消費者の需要に拍車をかけています。消費者は、自動車がスマートフォンやスマートホームと同レベルのコネクティビティを提供することを期待しています。より高速で信頼性の高い4Gや5Gネットワーク、強化されたオンボード・コンピューティング・パワーなどの進歩は、運転体験を向上させる幅広い機能を可能にします。例えば、リアルタイムの交通情報、天気予報、シームレスなスマートフォンとの連携、車内Wi-Fiなどがあります。移動中もつながっていられるという魅力は、コネクテッド・カーに対する消費者の関心を高める大きな要因であり、市場成長にプラスの影響を与えています。業界の主なプレーヤーは、より優れた、より効率的な車両接続性を提供する技術を開発し、採用しています。たとえば、2022年にFord Motors社は、同社のピックアップトラックにSnapdragonの5G Modem-RFの使用を開始しました。同年、クアルコムはデジタル・シャーシ接続自動車技術を発表しました。デジタルシャーシは、車両テレマティクス、デジタルコックピット、ADAS(先進運転支援システム)用のクラウドプラットフォームの集合体です。

欧州のコネクテッド車両市場概要

欧州の自動車産業は、卓越したエンジニアリング、革新性、品質の伝統で知られ、世界の自動車業界の礎石となってきました。同産業は世界生産の20%を占めています。コネクテッド車両の採用は欧州全域で勢いを増しています。この採用は、消費者の嗜好だけでなく、ADAS(先進運転支援システム)やV2X(Vehicle-to-Everything)通信の導入を促す規制措置や安全基準によっても推進されています。欧州各国政府は、交通安全の向上と排出ガス削減のため、コネクテッド車両の導入を積極的に支援しています。協調型インテリジェント交通システム(C-ITS)は、EUのコネクテッド車両・プロジェクトの一つです。このシステムの導入が成功すれば、車両と道路インフラ間の情報交換が可能になります。C-ROADSプラットフォームは、欧州全域でC-ITSの統一的な運用を可能にするもので、道路当局や事業者との緊密な協力のもとに開発が進められています。ドイツ、スペイン、フランス、英国など、多くの著名な欧州諸国は、コネクテッド・モビリティに適したインフラ整備に多額の投資を行っています。例えば、スペインは初のインテリジェント高速道路を建設中です。このプロジェクトでは、Kapsch TrafficComのテクノロジーとソフトウェアが、2024年までにビルバオ近郊の高速道路A8の60km区間のデジタル化を可能にします。

欧州のコネクテッド車両市場の収益と2030年までの予測(金額)

欧州のコネクテッド車両市場のセグメンテーション

欧州のコネクテッド車両市場は、技術、接続性、用途、国によって区分されます。技術に基づき、欧州のコネクテッド車両市場は5G、4G/LTE、3G &2Gに分類されます。4G/LTEセグメントは2022年に最大の市場シェアを占めました。

接続性によって、欧州のコネクテッド車両市場は統合型、テザー型、組み込み型に分類されます。組み込み型セグメントが2022年に最大の市場シェアを占めました。

用途別では、欧州のコネクテッド車両市場はテレマティクス、インフォテインメント、運転支援、その他に分類されます。2022年にはインフォテインメントセグメントが最大の市場シェアを占めました。

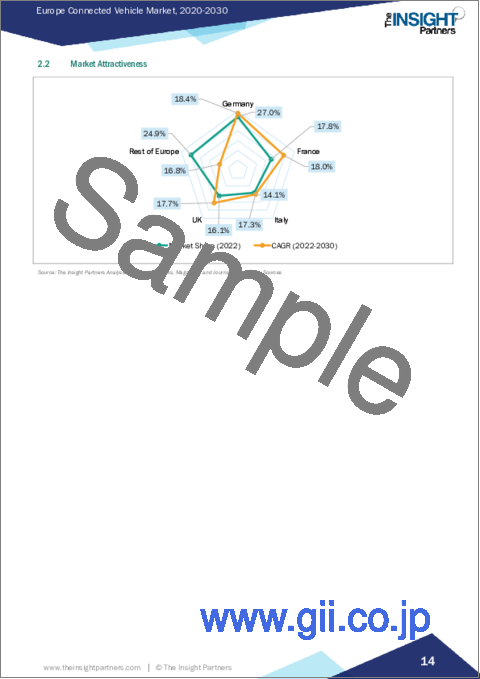

国別に見ると、欧州のコネクテッド車両市場はドイツ、フランス、イタリア、英国、その他欧州に区分されます。2022年の欧州のコネクテッド車両市場シェアはドイツが独占。

AT&T、Audi AG、Bayerische Motoren Werke AG、Continental AG、Denso、General Motors Co、Harman International Industries Inc、Robert Bosch GmbH、Visteon Corp、Vodafone Group Plcは、欧州のコネクテッド車両市場で事業を展開している主要企業の一部です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 欧州のコネクテッド車両市場情勢

- エコシステム分析

- 自動車メーカーとOEM

- ティア1サプライヤー

- ティア2およびティア3サプライヤー

- 通信プロバイダー

- 技術プロバイダー

- 政府規制および標準化団体

- データプロバイダー

- 物流・流通

- サービスおよびメンテナンス・プロバイダー

- エンドユーザー

- アフターマーケットプロバイダー

第5章 欧州のコネクテッド車両市場- 主要産業力学

- コネクテッド車両市場- 主要産業力学

- 市場促進要因

- 運転支援システムの需要拡大

- コネクティビティ技術の進歩

- 市場抑制要因

- データのプライバシーとセキュリティに関する懸念

- 初期コストの高さと手頃さへの懸念

- 市場機会

- スマートシティへの取り組みの増加

- 自律走行車の普及

- 今後の動向

- コネクテッド車両のデータ収益化

- 促進要因と抑制要因の影響

第6章 コネクテッド車両市場- 欧州市場分析

- 欧州のコネクテッド車両市場収益、2022年~2030年

- 欧州のコネクテッド車両市場の予測と分析

第7章 欧州のコネクテッド車両市場分析:技術別

- コネクテッド車両市場、技術別(2022年、2030年)

- 5G

- 4G

- 3G・2G

第8章 欧州のコネクテッド車両市場分析:コネクティビティ別

- コネクテッド車両市場:コネクティビティ別(2022年、2030年)

- 統合型

- テザリング

- 組み込み型

第9章 欧州のコネクテッド車両市場分析:用途別

- コネクテッド車両市場:用途別(2022年、2030年)

- テレマティクス

- インフォテインメント

- 運転支援

- その他

第10章 欧州のコネクテッド車両市場:国別分析

- 欧州

- ドイツ

- フランス

- イタリア

- 英国

- その他欧州

第11章 業界情勢

- 市場イニシアティブ

- 新製品開発

- 合併と買収

第12章 企業プロファイル

- Harman International Industries Inc

- Robert Bosch GmbH

- AT&T Inc

- Denso Corp

- Visteon Corp

- Continental AG

- Audi AG

- General Motors Co

- Bayerische Motoren Werke AG

- Vodafone Group Plc

第13章 付録

List Of Tables

- Table 1. Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Million)

- Table 2. Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Million) - Technology

- Table 3. Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Million) - Connectivity

- Table 4. Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Million) - Application

- Table 5. Germany Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Technology

- Table 6. Germany Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Connectivity

- Table 7. Germany Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Application

- Table 8. France Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Technology

- Table 9. France Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Connectivity

- Table 10. France Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Application

- Table 11. Italy Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Technology

- Table 12. Italy Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Connectivity

- Table 13. Italy Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Application

- Table 14. UK Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Technology

- Table 15. UK Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Connectivity

- Table 16. UK Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Application

- Table 17. Rest of Europe Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Technology

- Table 18. Rest of Europe Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Connectivity

- Table 19. Rest of Europe Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn) - Application

List Of Figures

- Figure 1. Connected Vehicle Market Segmentation, By Country

- Figure 2. Ecosystem: Connected Vehicle Market

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Connected Vehicle Market Revenue (US$ Million), 2022 - 2030

- Figure 5. Connected Vehicle Market Share (%) - Technology, 2022 and 2030

- Figure 6. 5G Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 7. 4G Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 8. 3G & 2G Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 9. Connected Vehicle Market Share (%) - Connectivity, 2022 and 2030

- Figure 10. Integrated Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 11. Tethered Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 12. Embedded Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 13. Connected Vehicle Market Share (%) - Application, 2022 and 2030

- Figure 14. Telematics Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 15. Infotainment Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 16. Driving assistance Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 17. Others Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 18. Connected Vehicle Market Breakdown by Key Country, 2022 and 2030 (%)

- Figure 19. Germany Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn)

- Figure 20. France Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn)

- Figure 21. Italy Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn)

- Figure 22. UK Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn)

- Figure 23. Rest of Europe Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn)

The Europe connected vehicle market was valued at US$ 12,625.37 million in 2022 and is expected to reach US$ 46,430.82 million by 2030; it is estimated to record a CAGR of 17.7% from 2022 to 2030.

Advancements in Connectivity Technology Fuel Europe Connected Vehicle Market

Advancements in connectivity technology fundamentally reshape the automotive landscape, and their positive impact on the connected vehicle market is notable and far-reaching. These advancements are fueling consumer demand by aligning vehicles with their increasingly connected lives. Consumers expect their cars to offer the same level of connectivity as their smartphones and smart homes. Advancements such as faster and more reliable 4G and 5G networks and enhanced onboard computing power enable a wide range of features that enhance the driving experience. Some features include real-time traffic updates, weather forecasts, seamless smartphone integration, and in-car Wi-Fi. The allure of staying connected while moving is a significant driver of consumer interest in connected vehicles, positively impacting market growth. Key players in the industry are developing and adopting technologies that provide better and more efficient vehicle connectivity. For example, in 2022, Ford Motors started using Snapdragon's 5G Modem-RF in its pick-up trucks. In the same year, Qualcomm introduced its digital chassis-connected car technologies. Digital Chassis is collection of cloud platforms for vehicle telematics, digital cockpit and advance driver assistance system.

Europe Connected Vehicle Market Overview

Europe automotive industry has long been a cornerstone of the global automotive landscape, known for its tradition of engineering excellence, innovation, and quality. The industry is accounting for ~20% of global production. The adoption of connected vehicles is gaining momentum across the continent. The adoption is not only driven by consumer preferences but also by regulatory measures and safety standards that encourage the implementation of advanced driver assistance systems (ADAS) and vehicle-to-everything (V2X) communication. European governments are actively supporting the deployment of connected vehicles to enhance road safety and reduce emissions. Cooperative Intelligent Transport Systems (C-ITS) is one of the EU's connected vehicle projects. Successful implementation of this system will enable information exchange between vehicles and the road infrastructure. The C-ROADS Platform, which enables the uniform deployment of C-ITS operations throughout Europe, is being developed in close collaboration with road authorities and operators. Many notable European countries, such as Germany, Spain, France, and the UK, are investing heavily to develop suitable infrastructure for connected mobility. For instance, Spain is building its first intelligent highways. In this project, Kapsch TrafficCom's technology and software will enable the digitalization of a 60-kilometer section of the A8 motorway near Bilbao by 2024.

Europe Connected Vehicle Market Revenue and Forecast to 2030 (US$ Million)

Europe Connected Vehicle Market Segmentation

The Europe connected vehicle market is segmented based on technology, connectivity, application, and country. Based on technology, the Europe connected vehicle market is categorized into 5G, 4G/LTE, and 3G & 2G. The 4G/LTE segment held the largest market share in 2022.

By on connectivity, the Europe connected vehicle market is segmented into integrated, tethered, and embedded. The embedded segment held the largest market share in 2022.

In terms of application, the Europe connected vehicle market is categorized into telematics, infotainment, driving assistance, and others. The infotainment segment held the largest market share in 2022.

Based on country, the Europe connected vehicle market is segmented into Germany, France, Italy, the UK, and the Rest of Europe. Germany dominated the Europe connected vehicle market share in 2022.

AT&T, Audi AG, Bayerische Motoren Werke AG, Continental AG, Denso, General Motors Co, Harman International Industries Inc, Robert Bosch GmbH, Visteon Corp, and Vodafone Group Plc are some of the leading companies operating in the Europe connected vehicle market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Europe Connected Vehicle Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.2.1 Automakers and OEMs

- 4.2.2 Tier 1 Suppliers

- 4.2.3 Tier 2 and Tier 3 Suppliers

- 4.2.4 Telecommunications Providers

- 4.2.5 Technology Providers

- 4.2.6 Government Regulations and Standards Bodies

- 4.2.7 Data Providers

- 4.2.8 Logistics and Distribution

- 4.2.9 Service and Maintenance Providers

- 4.2.10 End Users

- 4.2.11 Aftermarket Providers

5. Europe Connected Vehicle Market - Key Industry Dynamics

- 5.1 Connected Vehicle Market - Key Industry Dynamics

- 5.2 Market Drivers

- 5.2.1 Growing Demand for Driving Assistance System

- 5.2.2 Advancements in Connectivity Technology

- 5.3 Market Restraints

- 5.3.1 Data Privacy and Security Concerns

- 5.3.2 High Initial Costs and Affordability Concerns

- 5.4 Market Opportunities

- 5.4.1 Increasing Smart City Initiatives

- 5.4.2 Adoption of Autonomous vehicles

- 5.5 Future Trends

- 5.5.1 Connected Car Data Monetization

- 5.6 Impact of Drivers and Restraints:

6. Connected Vehicle Market - Europe Market Analysis

- 6.1 Europe Connected Vehicle Market Revenue (US$ Million), 2022 - 2030

- 6.2 Europe Connected Vehicle Market Forecast and Analysis

7. Europe Connected Vehicle Market Analysis - Technology

- 7.1 Connected Vehicle Market, By Technology (2022 and 2030)

- 7.2 5G

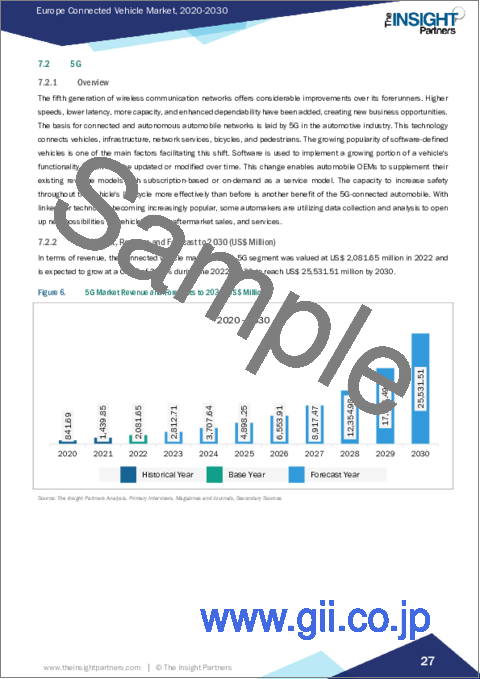

- 7.2.1 Overview

- 7.2.2 5G Market, Revenue and Forecast to 2030 (US$ Million)

- 7.3 4G

- 7.3.1 Overview

- 7.3.2 4G Market, Revenue and Forecast to 2030 (US$ Million)

- 7.4 3G & 2G

- 7.4.1 Overview

- 7.4.2 3G & 2G Market, Revenue and Forecast to 2030 (US$ Million)

8. Europe Connected Vehicle Market Analysis - Connectivity

- 8.1. Connected Vehicle Market, By Connectivity (2022 and 2030)

- 8.2 Integrated

- 8.2.1 Overview

- 8.2.2 Integrated Market, Revenue and Forecast to 2030 (US$ Million)

- 8.3 Tethered

- 8.3.1 Overview

- 8.3.2 Tethered Market, Revenue and Forecast to 2030 (US$ Million)

- 8.4 Embedded

- 8.4.1 Overview

- 8.4.2 Embedded Market, Revenue and Forecast to 2030 (US$ Million)

9. Europe Connected Vehicle Market Analysis - Application

- 9.1. Connected Vehicle Market, By Application (2022 and 2030)

- 9.2 Telematics

- 9.2.1 Overview

- 9.2.2 Telematics Market, Revenue and Forecast to 2030 (US$ Million)

- 9.3 Infotainment

- 9.3.1 Overview

- 9.3.2 Infotainment Market, Revenue and Forecast to 2030 (US$ Million)

- 9.4 Driving assistance

- 9.4.1 Overview

- 9.4.2 Driving assistance Market, Revenue and Forecast to 2030 (US$ Million)

- 9.5 Others

- 9.5.1 Overview

- 9.5.2 Others Market, Revenue and Forecast to 2030 (US$ Million)

10. Europe Connected Vehicle Market - Country Analysis

- 10.1 Europe

- 10.1.1 Overview

- 10.1.2 Europe Connected Vehicle Market Revenue and Forecasts and Analysis - By Country

- 10.1.2.1 Germany Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn)

- 10.1.2.1.1 Germany Connected Vehicle Market Breakdown by Technology

- 10.1.2.1.2 Germany Connected Vehicle Market Breakdown by Connectivity

- 10.1.2.1.3 Germany Connected Vehicle Market Breakdown by Application

- 10.1.2.2 France Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn)

- 10.1.2.2.1 France Connected Vehicle Market Breakdown by Technology

- 10.1.2.2.2 France Connected Vehicle Market Breakdown by Connectivity

- 10.1.2.2.3 France Connected Vehicle Market Breakdown by Application

- 10.1.2.3 Italy Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn)

- 10.1.2.3.1 Italy Connected Vehicle Market Breakdown by Technology

- 10.1.2.3.2 Italy Connected Vehicle Market Breakdown by Connectivity

- 10.1.2.3.3 Italy Connected Vehicle Market Breakdown by Application

- 10.1.2.4 UK Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn)

- 10.1.2.4.1 UK Connected Vehicle Market Breakdown by Technology

- 10.1.2.4.2 UK Connected Vehicle Market Breakdown by Connectivity

- 10.1.2.4.3 UK Connected Vehicle Market Breakdown by Application

- 10.1.2.5 Rest of Europe Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn)

- 10.1.2.5.1 Rest of Europe Connected Vehicle Market Breakdown by Technology

- 10.1.2.5.2 Rest of Europe Connected Vehicle Market Breakdown by Connectivity

- 10.1.2.5.3 Rest of Europe Connected Vehicle Market Breakdown by Application

- 10.1.2.1 Germany Connected Vehicle Market Revenue and Forecasts To 2030 (US$ Mn)

11. Industry Landscape

- 11.1 Overview

- 11.2 Market Initiative

- 11.3 New Product Development

- 11.4 Merger and Acquisition

12. Company Profiles

- 12.1 Harman International Industries Inc

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Robert Bosch GmbH

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 AT&T Inc

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Denso Corp

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Visteon Corp

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Continental AG

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Audi AG

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 General Motors Co

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 Bayerische Motoren Werke AG

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 Vodafone Group Plc

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 Key Developments

13. Appendix

- 13.1 About The Insight Partners