|

市場調査レポート

商品コード

1684687

コネクテッドビークル技術市場の機会、成長促進要因、産業動向分析、2025年~2034年予測Connected Vehicle Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| コネクテッドビークル技術市場の機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月14日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

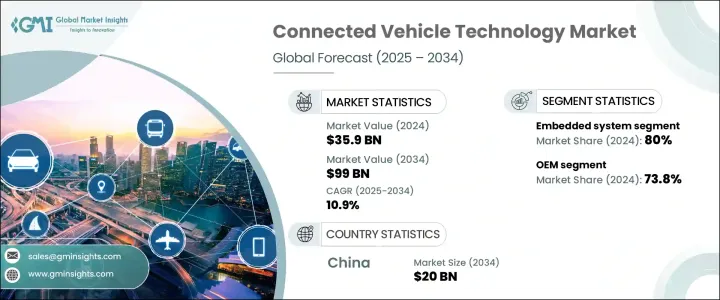

コネクテッドビークル技術の世界市場は、2024年に359億米ドルと評価され、2025年から2034年にかけてCAGR 10.9%で拡大する見通しです。

この成長の原動力となっているのは、デジタルソリューションの急速な普及と、よりスマートで安全かつ効率的な交通機関に対する需要の高まりです。この成長には、自動車の安全機能に対する減税や自動車購入に対する補助金といった政府の優遇措置が後押ししており、消費者とメーカーの双方が最先端の自動車技術を取り入れるようになっています。コネクティビティは現代の自動車設計に不可欠な要素となっており、自動車メーカーは先進的なテレマティクス、インフォテインメント、安全システムをモデルに組み込むことに注力しています。テクノロジーが進化を続ける中、人工知能、5Gネットワーク、クラウドベースのプラットフォームの利用が拡大し、V2X(Vehicle-to-Everything)通信が強化され、全体的な運転体験が向上し、より高い安全基準が確保されています。

電気自動車や自律走行車の人気が高まっていることも、市場拡大を後押ししています。これらの自動車は、ナビゲーション、診断、遠隔監視のために組み込みシステムに大きく依存しているからです。自動車メーカーは、サイバーセキュリティを維持しながらコネクティビティを強化する、安全で高性能なデジタル・ソリューションを開発するために、テクノロジー企業との協力関係を強めています。消費者の期待は、車内でのパーソナライズされたシームレスなデジタル体験へとシフトしており、自動車メーカーの技術革新をさらに後押ししています。OTA(Over-the-Air)アップデートの台頭により、自動車メーカーは購入後に車両の機能を強化し、最新のソフトウェア改良を常に反映させることができるようになりました。この動向により、コネクテッドビークル技術はオプションではなく必需品となり、世界の普及が加速しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 359億米ドル |

| 予測金額 | 990億米ドル |

| CAGR | 10.9% |

コネクテッドビークル技術の市場は、主にV2X通信と組み込みシステムに分けられます。組み込みシステムは、製造プロセスで車両に直接統合されるため、2024年に最大のシェアを占めました。これらのシステムには、テレマティクス、インフォテインメント、ナビゲーション・ソリューションが含まれ、ユーザー体験を向上させ、車両性能を高め、リアルタイムのデータ交換を可能にします。自律走行の推進に伴い、ADAS(先進運転支援システム)や予知保全ソリューションをサポートする組込みシステムの重要性はさらに高まっています。自動車メーカーは、AI主導のアナリティクスを活用して性能を最適化し、交通安全性を高めており、組込みシステムはコネクテッド・ビークルのエコシステムの基幹となっています。

コネクテッドビークル技術は、OEM(相手先ブランド製造)とアフターマーケットの2つの主要セグメントで利用されています。2024年には、OEMセグメントが73.8%という圧倒的な市場シェアを占め、これは業界が工場設置型のコネクティビティ・ソリューションに強く注力していることを反映しています。メーカー各社は、テレマティクスとV2X通信機能を新車に組み込み、シームレスなデジタル統合に対する消費者の需要の高まりに対応しています。このような直接的な統合は、車両の安全性を高め、性能を最適化し、運転効率を向上させるため、OEMを市場成長の主な促進要因として位置づけています。スマート製造とクラウドベースのプラットフォームに投資する自動車メーカーが増えるにつれ、コネクテッド・モビリティの未来を形作るOEMの役割は拡大し続けています。

中国のコネクテッドビークル技術市場は、積極的なマーケティング・キャンペーン、自動車販売の増加、ハイテク自動車機能に対する消費者の強い意欲に牽引され、2034年までに200億米ドルを創出する勢いです。排出量削減とスマート交通ソリューションの推進に取り組む同国の姿勢も、採用を加速させています。アジア太平洋地域は全体として急速な市場拡大を目の当たりにしており、政府や自動車業界のリーダーたちがこの分野におけるデジタルトランスフォーメーションを積極的に推進しています。北米も、高度なコネクティビティ機能に対する消費者の関心が高まるにつれ、同様の勢いを見せています。現在では、統合されたデジタル・ソリューションを搭載した自動車を優先的に購入する自動車購入者が増加しており、コネクテッドビークル技術が自動車産業の将来における中核的な要素であることを確固たるものにしています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 自動車OEM

- 技術プロバイダー

- 通信事業者

- プラットフォーム開発企業

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- コネクテッドビークル技術の使用事例

- テクノロジーとイノベーションの展望

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 安全機能に対する需要の高まり

- 5Gコネクティビティの進歩

- AIと機械学習の統合

- 政府による規制とインセンティブの拡大

- 業界の潜在的リスク&課題

- データのプライバシーとセキュリティに関する懸念

- 導入コストの高さ

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- V2X通信

- 組み込みシステム

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

- 電気自動車(EV)

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 自律走行

- モビリティ・アズ・ア・サービス(MaaS)

- インフォテインメント

- フリート管理

- 安全とセキュリティ

- 車両診断とメンテナンス

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Aptiv

- Atos

- AWS

- Bosch

- Cisco

- Continental

- Denso

- Ericsson

- Harman(Samsung Electronics)

- IBM

- Infineon Technologies

- Intel

- Microsoft

- Mobileye

- NXP Semiconductors

- Orange

- Qualcomm

- Telenor

- Verizon

- Vodafone

The Global Connected Vehicle Technology Market, valued at USD 35.9 billion in 2024, is set to expand at a CAGR of 10.9% between 2025 and 2034. The growth is driven by the rapid adoption of digital solutions and the increasing demand for smarter, safer, and more efficient transportation. This growth is fueled by government incentives such as tax breaks on vehicle safety features and subsidies for car purchases, which encourage both consumers and manufacturers to embrace cutting-edge automotive technologies. Connectivity has become an essential aspect of modern vehicle design, with automakers focusing on integrating advanced telematics, infotainment, and safety systems into their models. As technology continues to evolve, the growing use of artificial intelligence, 5G networks, and cloud-based platforms is enhancing vehicle-to-everything (V2X) communication, improving overall driving experiences, and ensuring higher safety standards.

The rising popularity of electric and autonomous vehicles is also propelling market expansion, as these vehicles rely heavily on embedded systems for navigation, diagnostics, and remote monitoring. Automakers are increasingly collaborating with technology companies to develop secure, high-performance digital solutions that enhance connectivity while maintaining cybersecurity. Consumer expectations are shifting towards personalized, seamless digital experiences within their vehicles, further pushing manufacturers to innovate. With the rise of over-the-air (OTA) updates, car manufacturers can now enhance vehicle functionality post-purchase, keeping cars up to date with the latest software improvements. This trend is making connected vehicle technology a necessity rather than an option, accelerating its adoption worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $35.9 Billion |

| Forecast Value | $99 Billion |

| CAGR | 10.9% |

The market for connected vehicle technology is primarily divided into V2X communication and embedded systems. Embedded systems commanded the largest share in 2024 due to their direct integration into vehicles during the manufacturing process. These systems include telematics, infotainment, and navigation solutions that improve user experience, enhance vehicle performance, and enable real-time data exchange. With the push toward autonomous driving, embedded systems are becoming even more critical, supporting advanced driver-assistance systems (ADAS) and predictive maintenance solutions. Automakers are leveraging AI-driven analytics to optimize performance and increase road safety, making embedded systems the backbone of the connected vehicle ecosystem.

Connected vehicle technology is utilized by two major segments: original equipment manufacturers (OEMs) and the aftermarket. In 2024, the OEM segment held a commanding 73.8% market share, reflecting the industry's strong focus on factory-installed connectivity solutions. Manufacturers are embedding telematics and V2X communication capabilities into new vehicles, addressing growing consumer demands for seamless digital integration. This direct integration enhances vehicle safety, optimizes performance, and improves driving efficiency, positioning OEMs as the primary drivers of market growth. As more automakers invest in smart manufacturing and cloud-based platforms, the role of OEMs in shaping the future of connected mobility continues to expand.

China connected vehicle technology market is on track to generate USD 20 billion by 2034, driven by aggressive marketing campaigns, increasing vehicle sales, and a strong consumer appetite for high-tech automotive features. The country's commitment to reducing emissions and advancing smart transportation solutions is also accelerating adoption. The Asia-Pacific region as a whole is witnessing rapid market expansion, with governments and automotive leaders actively promoting digital transformation in the sector. North America is experiencing similar momentum as consumer interest in advanced connectivity features grows. A rising number of car buyers now prioritize vehicles equipped with integrated digital solutions, solidifying connected vehicle technology as a core component of the automotive industry's future.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Automotive OEMs

- 3.1.2 Technology providers

- 3.1.3 Telecommunication companies

- 3.1.4 Platform developers

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Use cases of connected vehicle technology

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing demand for safety features

- 3.8.1.2 Advancements in 5G connectivity

- 3.8.1.3 Integration of AI and machine learning

- 3.8.1.4 Growing government regulations and incentives

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Data privacy and security concerns

- 3.8.2.2 High cost of implementation

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021-2034, ($Bn)

- 5.1 Key trends

- 5.2 V2X communication

- 5.3 Embedded system

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021-2034, ($Bn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicle

- 6.3.1 Light Commercial Vehicles (LCVs)

- 6.3.2 Heavy Commercial Vehicles (HCVs)

- 6.4 Electric Vehicles (EVs)

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034, ($Bn)

- 7.1 Key trends

- 7.2 Autonomous driving

- 7.3 Mobility as a Service (MaaS)

- 7.4 Infotainment

- 7.5 Fleet management

- 7.6 Safety and security

- 7.7 Vehicle diagnostics and maintenance

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034, ($Bn)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aptiv

- 10.2 Atos

- 10.3 AWS

- 10.4 Bosch

- 10.5 Cisco

- 10.6 Continental

- 10.7 Denso

- 10.8 Ericsson

- 10.9 Harman (Samsung Electronics)

- 10.10 IBM

- 10.11 Infineon Technologies

- 10.12 Intel

- 10.13 Microsoft

- 10.14 Mobileye

- 10.15 NXP Semiconductors

- 10.16 Orange

- 10.17 Qualcomm

- 10.18 Telenor

- 10.19 Verizon

- 10.20 Vodafone