コネクテッドカーサービスの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Connected Vehicle Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750294

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

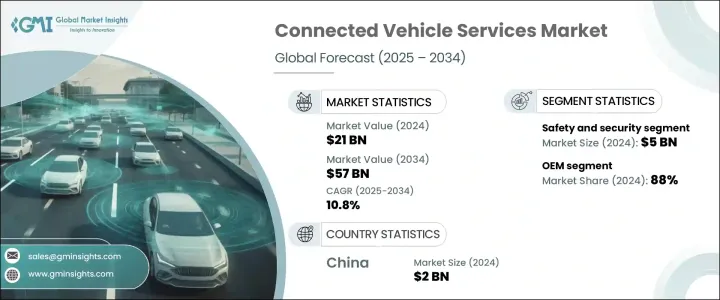

世界のコネクテッドカーサービスの市場規模は、2024年に210億米ドルとなり、CAGR 10.8%で成長し、2034年には570億米ドルに達すると推定されます。

この成長の原動力は、従来の自動車からソフトウェア定義の自動車への移行が進み、自動車サービスの開発、提供、収益化の方法が大きく変化していることです。従来の自動車とは異なり、最新の自動車は、購入後もリアルタイムのアップデートやオンデマンドサービスを可能にする、適応可能なソフトウェアプラットフォームを中心に設計されています。このダイナミックな設計により、メーカーは遠隔診断、運転支援、システムアップグレードなどの機能を無線アップデートで導入し、顧客満足度とサービス範囲の両方を向上させることができます。その結果、コネクテッドカーサービスは、よりスマートで、より応答性が高く、より安全なモビリティソリューションに対する需要の高まりに後押しされ、自動車開発戦略の基本要素となっています。

消費者は、安全性と利便性を確保しながら運転体験を向上させるコネクティビティ機能を自動車に内蔵することをますます期待するようになっています。この需要シフトにより、自動車メーカーはインフォテインメント、安全警告、ナビゲーション、遠隔操作などのサービスを新モデルに直接統合する必要に迫られています。継続的に機能を更新し、パーソナライズされたサービスを提供する能力は、自動車をデジタルプラットフォームに変え、サブスクリプションベースのサービスモデルを後押ししています。メーカー各社は現在、予知保全アラート、使用状況の追跡、音声アシスト・コマンドなどを通じてユーザー体験を強化することに注力しています。自動車がAIとIoT技術を統合し続ける中、拡張性のあるテレマティクスと強力なクラウド機能を提供する主要企業は、リードする立場にあります。加えて、データプライバシー、サイバーセキュリティ、車両安全性に関する世界の規制の進化により、サービス提供モデルが再構築されつつあり、国際基準を満たすインフラとコンプライアンス態勢を備えた企業が有利になっています。サービスベースの提供へのシフトは、自動車エコシステムにおける長期的な顧客エンゲージメントと継続的な収益創出の舞台を整えつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 210億米ドル |

| 予測金額 | 570億米ドル |

| CAGR | 10.8% |

サービス別に見ると、市場は遠隔操作、安全・セキュリティ、ナビゲーション・インフォテインメント、運転支援、車両管理、その他に分けられます。安全・セキュリティ分野は2024年の市場をリードし、約50億米ドルを生み出し、市場シェア全体の25%以上を占めます。消費者は、緊急警報、衝突検知、盗難防止、ロードサービスなどのリアルタイム機能を非常に重視しており、これらは認知された車両安全性と実際の車両安全性の両方に大きく貢献しています。これらのサービスは、個人ユーザーだけでなく、車両追跡、ドライバーの行動分析、リスク評価のためにリアルタイムモニタリングに依存しているフリートオペレーターや保険会社からも評価されています。これらの機能は、安心感を提供することで、顧客の嗜好やブランドロイヤルティを高めます。

コネクテッドカーサービス市場は、最終用途別にOEM市場とアフターマーケット市場に分類されます。2024年には、OEMセグメントが市場全体の約88%のシェアを占めています。自動車メーカーは、ナビゲーション、診断、リモートアクセス機能などの統合サービスを提供するために、生産段階でハードウェアとソフトウェアを組み込むようになってきています。消費者は、信頼できるメーカーが提供するコネクテッドサービスが車両にプリインストールされていれば、それを利用する傾向が強いです。OEMは、サービスインフラを完全にコントロールできるため、アップデートの提供、データ収集、新機能の展開を独自に行うことができ、収益化の可能性を高め、顧客との関係を強化できるというメリットがあります。

自動車のコネクティビティは通常、組み込み型、テザリング型、統合型に分類されます。このうち、組み込み型コネクティビティが2024年の市場をリードしました。これらのシステムは、内蔵のSIMカードやモデムを介して継続的なインターネットアクセスを提供し、中断のないサービス提供を可能にする能力で支持されています。遠隔診断、OTAアップデート、予知保全などの機能をシームレスに提供できるため、所有体験が向上します。OEMも車両管理者も、集中制御と外部依存のない一貫したユーザーエクスペリエンスを提供できる組み込みシステムを好んでいます。

車両タイプ別に見ると、市場は乗用車、商用車、二輪車、三輪車、オフロード車両に区分されます。乗用車は世界的に販売台数が多いため、2024年の市場をリードしました。新車の大半がコネクテッドシステムを搭載するようになったため、統合サービスへの需要が大幅に拡大しました。消費者は、安全通知、ドライバープロファイル、モバイルデバイス統合などの先進機能が標準装備されることを期待しており、自動車メーカーはサービスのバンドルとデジタル強化を主要な差別化要因として優先させています。こうしたデジタルサービスの提供は、最新の自動車マーケティング戦略や顧客維持の取り組みにとって不可欠なものとなりつつあります。

地域別では、アジア太平洋地域が2024年に35%以上の最大市場シェアを占め、中国が20億米ドルの推定額で大きく貢献しています。同地域は、強力な生産能力と、コネクテッドカーやインテリジェントカー技術に対する消費者の高い準備態勢から恩恵を受けています。この地域のメーカーは、スマートモビリティに対する需要の高まりに対応するため、自動車のデジタル機能の強化に注力しています。アジア太平洋地域のインフラ、特に堅牢な4Gおよび5Gネットワークは、クラウド処理、OTAアップデート、位置情報機能など、コネクテッドサービスに必要なリアルタイムのデータ交換をサポートしています。

コネクテッドカーサービス市場を形成する主要企業には、AT&T、Bosch、BMW、Continental、General Motors、Ford、Geotab、HERE Technologies、Harman International、Verizon Connectなどがあります。これらの企業は、先進的なテレマティクス、クラウドインフラ、サービスベースのモデルを活用し、進化する消費者の需要に応えるとともに、市場全体でコンプライアンスやデータセキュリティの課題に取り組んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 自動車メーカー

- 自動車技術プロバイダー

- クラウドおよびITサービスプロバイダー

- 最終用途

- 利益率分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- ユースケース

- 保険

- シェアードモビリティ

- フリート管理

- その他

- トップコネクテッドカーサービス

- 規制情勢

- 影響要因

- 促進要因

- ソフトウェア定義車両への移行

- 4G/5GおよびV2X接続の拡張

- 車内の安全性、利便性、効率性に対する需要の高まり

- フリート管理と商用テレマティクス

- 業界の潜在的リスク&課題

- サイバーセキュリティとデータプライバシーのリスク

- 技術統合にかかる高コスト

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:サービス別、2021~2034年

- 主要動向

- 安全・セキュリティ

- リモート操作

- ナビゲーション・インフォテインメント

- 車両管理

- 運転支援

- その他

第6章 市場推計・予測:コネクティビティ別、2021~2034年

- 主要動向

- 埋め込み型

- テザリング型

- 統合型

第7章 市場推計・予測:車両別、2021~2034年

- 主要動向

- 乗用車

- セダン

- SUV

- ハッチバック

- 商用車

- 小型商用車

- 中型商用車

- 大型商用車

- 二輪車・三輪車

- オフロード車両

第8章 市場推計・予測:最終用途別、2021~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- AT&T

- BMW

- Bosch

- Continental

- Ford

- General Motors

- Geotab

- Harman

- HERE Technologies

- Hyundai

- Ituran

- Nissan

- Octo Telematics

- Qualcomm

- Sierra Wireless

- SiriusXM Connected Vehicle Services

- Tesla

- Toyota

- Verizon Connect

- Volkswagen

- Zubie

目次

The Global Connected Vehicle Services Market was valued at USD 21 billion in 2024 and is estimated to grow at a CAGR of 10.8% to reach USD 57 billion by 2034. This growth is driven by the increasing transition from traditional vehicles to software-defined vehicles, which has significantly reshaped how automotive services are developed, offered, and monetized. Unlike conventional vehicles, modern vehicles are designed around adaptable software platforms that enable real-time updates and on-demand services even after purchase. This dynamic architecture allows manufacturers to introduce features like remote diagnostics, driver assistance, and system upgrades through over-the-air updates, enhancing both customer satisfaction and service scope. As a result, connected vehicle services have become a fundamental component of automotive development strategies, driven by rising demand for smarter, more responsive, and safer mobility solutions.

Consumers are increasingly expecting their vehicles to offer built-in connectivity features that improve the driving experience while ensuring safety and convenience. This demand shift is compelling automakers to integrate services like infotainment, safety alerts, navigation, and remote controls directly into new models. The ability to continuously update features and provide personalized services is turning vehicles into digital platforms, encouraging subscription-based service models. Manufacturers are now focusing on enhancing user experiences through predictive maintenance alerts, usage tracking, and voice-assisted commands. As vehicles continue to integrate AI and IoT technologies, companies offering scalable telematics and strong cloud capabilities are well-positioned to lead. In addition, evolving global regulations around data privacy, cybersecurity, and vehicular safety are reshaping service delivery models, favoring firms with the infrastructure and compliance readiness to meet international standards. The shift toward service-based offerings is setting the stage for long-term customer engagement and ongoing revenue generation in the automotive ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21 Billion |

| Forecast Value | $57 Billion |

| CAGR | 10.8% |

In terms of services, the market is divided into remote operations, safety and security, navigation and infotainment, driver assistance, vehicle management, and others. The safety and security segment led the market in 2024, generating approximately USD 5 billion and capturing over 25% of the total market share. Consumers place high importance on real-time features like emergency alerts, crash detection, theft prevention, and roadside assistance, which contribute significantly to both perceived and actual vehicle safety. These services are valued not only by individual users but also by fleet operators and insurers, who rely on real-time monitoring for vehicle tracking, driver behavior analysis, and risk assessment. These features often drive customer preference and brand loyalty by providing peace of mind.

By end use, the connected vehicle services market is classified into OEM and aftermarket segments. The OEM segment dominated the landscape in 2024, holding nearly 88% of the overall market share. Automakers are increasingly embedding hardware and software at the production stage to deliver integrated services such as navigation, diagnostics, and remote access capabilities. Consumers are more inclined to use connected services when they come pre-installed in the vehicle from a trusted manufacturer. OEMs benefit from full control over the service infrastructure, allowing them to offer updates, collect data, and roll out new features independently, which enhances monetization potential and strengthens customer relationships.

Connectivity in vehicles is typically categorized as embedded, tethered, or integrated. Among these, embedded connectivity led the market in 2024. These systems are favored for their ability to provide continuous internet access via built-in SIM cards and modems, enabling uninterrupted service delivery. Features such as remote diagnostics, OTA updates, and predictive maintenance can be delivered seamlessly, improving the ownership experience. OEMs and fleet managers alike prefer embedded systems for their centralized control and ability to provide a consistent user experience without external dependencies.

By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, two- and three-wheelers, and off-highway vehicles. Passenger vehicles led the market in 2024 due to high global sales volume. As the majority of new vehicles are now equipped with connected systems, the demand for integrated services has expanded significantly. Consumers expect advanced features like safety notifications, driver profiles, and mobile device integration to become standard, which pushes automakers to prioritize service bundling and digital enhancements as key differentiators. These digital offerings are becoming essential to modern automotive marketing strategies and customer retention efforts.

Regionally, Asia Pacific held the largest market share of over 35% in 2024, with China contributing significantly at an estimated value of USD 2 billion. The region benefits from strong production capabilities and high consumer readiness for connected and intelligent automotive technologies. Manufacturers in the region are focusing on enhancing the digital capabilities of their vehicles to cater to growing demands for smart mobility. The infrastructure in Asia Pacific, especially with robust 4G and 5G networks, supports real-time data exchange required for connected services, including cloud processing, OTA updates, and location-based functions.

Key companies shaping the connected vehicle services market include AT&T, Bosch, BMW, Continental, General Motors, Ford, Geotab, HERE Technologies, Harman International, and Verizon Connect. These players are leveraging advanced telematics, cloud infrastructure, and service-based models to meet evolving consumer demands while addressing compliance and data security challenges across markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Automotive manufacturers

- 3.2.2 Automotive technology providers

- 3.2.3 Cloud and IT Service providers

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Impact of Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook & future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Use cases

- 3.8.1 Insurance

- 3.8.2 Shared mobility

- 3.8.3 Fleet management

- 3.8.4 Others

- 3.9 Top connected vehicles services

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Shift toward software-defined vehicles

- 3.11.1.2 Expansion of 4G/5G and V2X connectivity

- 3.11.1.3 Increasing demand for in-vehicle safety, convenience and efficiency

- 3.11.1.4 Fleet management and commercial telematics

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 Cybersecurity and data privacy risks

- 3.11.2.2 High cost of technology integration

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Service, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Safety and security

- 5.3 Remote operations

- 5.4 Navigation and infotainment

- 5.5 Vehicle management

- 5.6 Driver assistance

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Embedded

- 6.3 Tethered

- 6.4 Integrated

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Passenger vehicle

- 7.2.1 Sedan

- 7.2.2 SUV

- 7.2.3 Hatchback

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

- 7.4 Two and three wheelers

- 7.5 Off-highway vehicles

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AT&T

- 10.2 BMW

- 10.3 Bosch

- 10.4 Continental

- 10.5 Ford

- 10.6 General Motors

- 10.7 Geotab

- 10.8 Harman

- 10.9 HERE Technologies

- 10.10 Hyundai

- 10.11 Ituran

- 10.12 Nissan

- 10.13 Octo Telematics

- 10.14 Qualcomm

- 10.15 Sierra Wireless

- 10.16 SiriusXM Connected Vehicle Services

- 10.17 Tesla

- 10.18 Toyota

- 10.19 Verizon Connect

- 10.20 Volkswagen

- 10.21 Zubie

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日