|

|

市場調査レポート

商品コード

1452525

欧州の航空付帯サービス:2030年までの市場予測 - 地域別分析 - タイプ別、航空会社別Europe Airline Ancillary Services Market Forecast to 2030 - Regional Analysis - by Type (Baggage Fees, On-Board Retail and A La Carte Services, Airline Retail, and FFP Mile Sales) and Carrier Type (Full-Service Carriers and Low-Cost Carriers) |

||||||

|

|||||||

|

|||||||

| 欧州の航空付帯サービス:2030年までの市場予測 - 地域別分析 - タイプ別、航空会社別 |

|

出版日: 2023年12月26日

発行: The Insight Partners

ページ情報: 英文 88 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

欧州の航空付帯サービス市場は、2022年に457億5,875万米ドルと評価され、2030年には1,882億1,230万米ドルに達すると予測され、2022年から2030年までのCAGRは19.3%で成長すると予測されています。

フリークエント・フライヤー・プログラムの利点が欧州の航空付帯サービス市場を活性化

フリークエント・フライヤー・プログラム(FFP)は、航空当局が常連客と良好な関係を維持するための忠実で長続きする方法です。このプログラムにより、航空会社はいくつかの提携取り決めや協力スキームを形成しています。これらには、競争運賃をもたらすコードシェア協定や、利益と市場シェアを拡大するためのサービスのバリエーションが含まれます。航空会社は、キャッシュバック特典、旅行保険、緊急医療サービス、空港ラウンジの利用などを通じて、フリークエント・フライヤーに常に特典ポイントを付与しています。同様に、世界中のトラベルクラブは、ブランド親和性をブランド・エクイティに変換し、加入料から新たな付帯収入を追加することで、航空会社のブランドを高めるための高度なサービスも提供しています。さらに、航空会社はフリークエント・フライヤーとの忠実な関係を維持するため、マージンを高め、乗客に付加価値サービスを提供することに絶えず注力しています。従って、このようなプログラムは欧州の航空付帯サービス市場の成長を促進します。

欧州の航空付帯サービス市場概要

欧州は、1日2万便以上のフライトがあり、毎年5億人以上の乗客が利用していることから、世界で最も忙しい空域であると認定されています。同地域の欧州の航空付帯サービス市場は、今後数年のうちに競合が激化することが予想され、各社は市場の激しい競争を勝ち抜くためにレッドオーシャン戦略をとることが期待されます。同地域はすでに、さまざまなテクノロジー企業がひしめく激戦区となっています。ここ数年、COVID-19パンデミックやウクライナ・ロシア戦争といった事態により、国際的にも国内的にも大きな混乱が起きています。ロシア・ウクライナ戦争とそれに伴う空域閉鎖は、航空会社の付帯サービス市場に大きな影響を与えました。ロシアが自国の領空を横切る路線の使用を禁止し、欧州連合(EU)がロシアの航空会社を禁止することで応酬したため、フライトがキャンセルされたり、コストのかかる迂回路を余儀なくされたりしています。このため、航空会社のシェアが低下し、貨物輸送に混乱が生じ、世界・サプライチェーンの課題が悪化しています。この戦争はまた、航空機リースにも影響を与え、航空会社にフライトの運休やキャンセルを促し、付帯サービス収入を減少させています。2022年6月、ルフトハンザ・グループは、戦争による欧州空域の制限のため、空の「大規模なボトルネック」につながるフライトのキャンセルと遅延を発表しました。こうした混乱は、スタッフの不足やリソースの制限など、航空会社が直面する課題をさらに悪化させ、乗客へのアンシラリーサービスの提供に影響を与えています。

欧州の航空付帯サービス市場の収益と2030年までの予測(10億米ドル)

欧州の航空付帯サービス市場のセグメンテーション

欧州の航空付帯サービス市場は、タイプ、航空会社タイプ、国に区分されます。

タイプ別では、手荷物料金、機内販売とアラカルトサービス、航空会社小売、FFPマイル販売に分けられます。手荷物料金は2022年に最大の市場シェアを占めました。

航空会社タイプ別では、欧州の航空付帯サービス市場はフルサービス航空会社と格安航空会社に二分されます。2022年の市場シェアは、フルサービスキャリアセグメントが大きいです。

国別に見ると、欧州の航空付帯サービス市場は、英国、ドイツ、フランス、スウェーデン、スペイン、ロシア、ノルウェー、デンマーク、フィンランド、オーストリア、その他欧州に区分されます。2022年の欧州の航空付帯サービス市場シェアは英国が独占しました。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 欧州の航空付帯サービス市場情勢

- エコシステム分析

- アンシラリーサービスの青写真

- 航空会社のアンシラリーサービスの有効化

- 航空付帯サービスの流通、収益分析、顧客体験管理

- バリューチェーンのベンダー一覧

第5章 欧州の航空付帯サービス市場:主要産業力学

- 欧州の航空付帯サービス市場:主要産業力学

- 市場促進要因

- 中間所得層の航空旅行選好の高まり

- マイレージプログラムのメリット

- 機内販売パートナーシップ

- 主な市場抑制要因

- 航空サービスのコスト削減

- 主な市場機会

- 新興企業による新たなアンシラリーレベニューの機会

- 今後の動向

- 機内Wi-Fiの普及拡大

- 促進要因と抑制要因の影響

第6章 航空付帯サービス市場:欧州市場分析

- 欧州の航空付帯サービス市場収益、2022年~2030年

- 欧州の航空付帯サービス市場予測・分析

第7章 航空付帯サービスの欧州市場分析:タイプ別

- 手荷物料金

- 機内販売とアラカルトサービス

- 航空小売

- FFPマイル販売

- その他

第8章 欧州の航空付帯サービス市場分析:航空会社別

- フルサービス航空会社

- 格安航空会社

第9章 欧州の航空付帯サービス市場:国別分析

- 英国

- ドイツ

- フランス

- スウェーデン

- スペイン

- ロシア

- ノルウェー

- デンマーク

- フィンランド

- オーストリア

- その他欧州

第10章 競合情勢

- 主要プレーヤー別ヒートマップ分析

- 企業のポジショニングと集中度

第11章 欧州の航空付帯サービス市場の業界情勢

- 市場の取り組み

- 新製品開発

第12章 企業プロファイル

- United Airlines Holdings Inc

- Delta Air Lines Inc

- EasyJet Plc

- Deutsche Lufthansa AG

- Ryanair Holdings Plc

- Air France KLM SA

第13章 付録

List Of Tables

- Table 1. Europe Airline Ancillary Services Market Segmentation

- Table 2. Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Billion)

- Table 3. Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Billion) - Type

- Table 4. Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Billion) - Carrier Type

- Table 5. UK: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Type

- Table 6. UK: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Carrier Type

- Table 7. Germany: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Type

- Table 8. Germany: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Carrier Type

- Table 9. France: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Type

- Table 10. France: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Carrier Type

- Table 11. Sweden: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Type

- Table 12. Sweden: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Carrier Type

- Table 13. Spain: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Type

- Table 14. Spain: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Carrier Type

- Table 15. Russia: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Type

- Table 16. Russia: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Carrier Type

- Table 17. Norway: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Type

- Table 18. Norway: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Carrier Type

- Table 19. Denmark: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Type

- Table 20. Denmark: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Carrier Type

- Table 21. Finland: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Type

- Table 22. Finland: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Carrier Type

- Table 23. Austria: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Type

- Table 24. Austria: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Carrier Type

- Table 25. Rest of Europe: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Type

- Table 26. Rest of Europe: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn) - By Carrier Type

- Table 27. Company Positioning & Concentration

- Table 28. List of Abbreviation

List Of Figures

- Figure 1. Europe Airline Ancillary Services Market Segmentation, By Country

- Figure 2. Ecosystem: Europe Airline Ancillary Services Market

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Europe Airline Ancillary Services Market Breakdown by Country, 2022 and 2030 (%)

- Figure 5. Europe Airline Ancillary Services Market Revenue (US$ Billion), 2022 - 2030

- Figure 6. Europe Airline Ancillary Services Market Share (%) - Type, 2022 and 2030

- Figure 7. Baggage Fees Market Revenue and Forecasts To 2030 (US$ Billion)

- Figure 8. On-Board Retail and A La Carte Services Market Revenue and Forecasts To 2030 (US$ Billion)

- Figure 9. Airline Retail Market Revenue and Forecasts To 2030 (US$ Billion)

- Figure 10. FFP Mile Sales Market Revenue and Forecasts To 2030 (US$ Billion)

- Figure 11. Others Market Revenue and Forecasts To 2030 (US$ Billion)

- Figure 12. Europe Airline Ancillary Services Market Share (%) - Carrier Type, 2022 and 2030

- Figure 13. Full-Service Carriers Market Revenue and Forecasts To 2030 (US$ Billion)

- Figure 14. Low-Cost Carriers Market Revenue and Forecasts To 2030 (US$ Billion)

- Figure 15. Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn)

- Figure 16. Europe Airline Ancillary Services Market Breakdown by Key Countries, 2022 and 2030 (%)

- Figure 17. UK: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn)

- Figure 18. Germany: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn)

- Figure 19. France: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn)

- Figure 20. Sweden: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn)

- Figure 21. Spain: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn)

- Figure 22. Russia: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn)

- Figure 23. Norway: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn)

- Figure 24. Denmark: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn)

- Figure 25. Finland: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn)

- Figure 26. Austria: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn)

- Figure 27. Rest of Europe: Europe Airline Ancillary Services Market Revenue and Forecasts To 2030 (US$ Bn)

- Figure 28. Heat Map Analysis By Key Players

The Europe airline ancillary services market was valued at US$ 45,758.75 million in 2022 and is expected to reach US$ 188,212.30 million by 2030; it is estimated to grow at a CAGR of 19.3% from 2022 to 2030.

Benefits of Frequent Flyer Program fuels the Europe Airline Ancillary Services Market

The frequent flyer program (FFP) is a loyal and long-lasting way for airline authorities to maintain a good relationship with their regular passengers. With this program, the airlines form several partnership arrangements and cooperative schemes. These include code-sharing agreements resulting in competitive fares and variations in the occurrence of services to increase profits and market share. The airlines constantly award reward points to its frequent flyers through cashback rewards, travel insurance, emergency medical services, and access to airport lounges. Similarly, Travel Clubs worldwide also offer advanced services to enhance airline brands by converting brand affinity into brand equity and adding new ancillary revenue from subscription fees. Further, the airlines are continuously focusing on boosting their margin and offering value-added services to the passengers to maintain a loyal relationship with frequent flyers. Thus, such programs drive the growth of the Europe airline ancillary services market.

Europe Airline Ancillary Services Market Overview

Europe accredits with having the world's busiest airspace by reporting more than 20,000 flights a day and ~ 500 million passengers flying every year. The Europe airline ancillary services market in the region is expected to become extensively competitive in the coming years, and the companies would be expected to follow the red-ocean strategy to survive the intense competition in the market. The region has already become a battleground for a mix of technology companies. Since the past couple of years, it has seen tremendous turbulence on the international and domestic front due to the situations such as the COVID-19 pandemic and Ukraine and Russia war. The Russia-Ukraine war and the resulting airspace closures have significantly impacted the airline ancillary services market. With Russia banning the use of routes crossing its airspace and the European Union reciprocating by banning Russian airlines, flights have been canceled or forced to take costly detours. This has led to a decline in airline shares and disruptions in cargo traffic, exacerbating global supply chain challenges. The war has also affected aircraft leasing and prompted airlines to suspend or cancel flights, reducing ancillary service revenues. In June 2022, Lufthansa Group announced flight cancellations and delays due to the restricted European airspace caused by the war, leading to "massive bottlenecks" in the sky. These disruptions have further exacerbated the challenges faced by airlines, including staff shortages and resource limitations, impacting the provision of ancillary services to passengers.

Europe Airline Ancillary Services Market Revenue and Forecast to 2030 (US$ Bn)

Europe Airline Ancillary Services Market Segmentation

The Europe airline ancillary services market is segmented into type, carrier type, and country.

Based on type, the Europe airline ancillary services market is divided into baggage fees, on-board retail and a la carte services, airline retail, and FFP mile sales. The baggage fees segment held the largest market share in 2022.

By carrier type, the Europe airline ancillary services market is bifurcated into full-service carriers and low-cost carriers. The full-service carriers segment held a larger market share in 2022.

Based on country, the Europe airline ancillary services market is segmented into the UK, Germany, France, Sweden, Spain, Russia, Norway, Denmark, Finland, Austria, and the Rest of Europe. The UK dominated the Europe airline ancillary services market share in 2022.

Air France KLM SA, Delta Air Lines Inc, Deutsche Lufthansa AG, EasyJet Plc, Ryanair Holdings Plc, and United Airlines Holdings Inc are some of the leading companies operating in the Europe airline ancillary services market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Europe Airline Ancillary Services Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.2.1 Ancillary Service Blueprint:

- 4.2.2 Airline Ancillary Service Enablement:

- 4.2.3 Airline Ancillary Services Distribution, Revenue Analytics And Customer Experience Management:

- 4.2.4 List of Vendors in the Value Chain:

5. Europe Airline Ancillary Services Market - Key Industry Dynamics

- 5.1 Europe Airline Ancillary Services Market - Key Industry Dynamics

- 5.2 Market Drivers

- 5.2.1 Rising Preference of Air Travel by Middle-Income Passengers

- 5.2.2 Benefits of Frequent Flyer Program

- 5.2.3 In-Flight Retail Partnerships

- 5.3 Key market restraints

- 5.3.1 Cost Cutting on Airline Services

- 5.4 Key market opportunities

- 5.4.1 Start-Ups Present New Ancillary Revenue Opportunities

- 5.5 Future trends

- 5.5.1 Increasing Deployment of In-Flight Wi-Fi

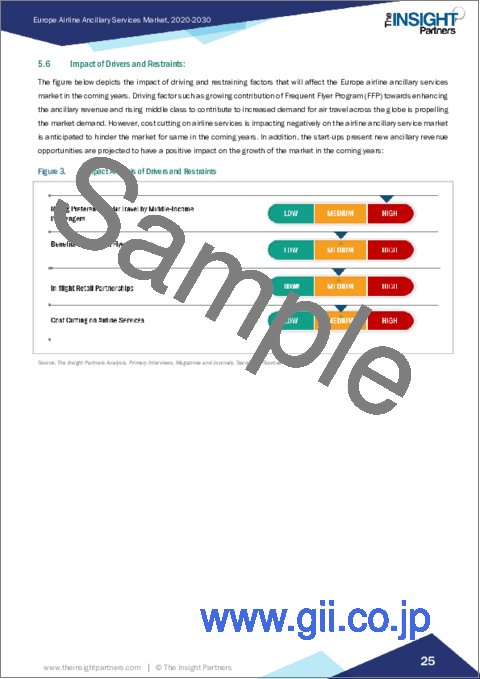

- 5.6 Impact of Drivers and Restraints:

6. Airline Ancillary Services Market - Europe Market Analysis

- 6.1 Europe Airline Ancillary Services Market Revenue (US$ Billion), 2022 - 2030

- 6.2 Europe Airline Ancillary Services Market Forecast and Analysis

7. Europe Airline Ancillary Services Market Analysis - Type

- 7.1 Baggage Fees

- 7.1.1 Overview

- 7.1.2 Baggage Fees Market Revenue, Revenue and Forecast to 2030 (US$ Billion)

- 7.2 On-Board Retail and A La Carte Services

- 7.2.1 Overview

- 7.2.2 On-Board Retail and A La Carte Services Market Revenue, Revenue and Forecast to 2030 (US$ Billion)

- 7.3 Airline Retail

- 7.3.1 Overview

- 7.3.2 Airline Retail Market Revenue and Forecast to 2030 (US$ Billion)

- 7.4 FFP Mile Sales

- 7.4.1 Overview

- 7.4.2 FFP Mile Sales Market Revenue and Forecast to 2030 (US$ Billion)

- 7.5 Others

- 7.5.1 Overview

- 7.5.2 Others Market Revenue and Forecast to 2030 (US$ Billion)

8. Europe Airline Ancillary Services Market Analysis - Carrier Type

- 8.1 Full-Service Carriers

- 8.1.1 Overview

- 8.1.2 Full-Service Carriers Market Revenue, and Forecast to 2030 (US$ Billion)

- 8.2 Low-Cost Carriers

- 8.2.1 Overview

- 8.2.2 Low-Cost Carriers Market Revenue, and Forecast to 2030 (US$ Billion)

9. Europe Airline Ancillary Services Market - Country Analysis

- 9.1 Overview

- 9.1.1 Europe Airline Ancillary Services Market Revenue and Forecasts and Analysis - By Countries

- 9.1.1.1 Europe Airline Ancillary Services Market Breakdown by Country

- 9.1.1.2 UK: Europe Airline Ancillary Services Market Revenue and Forecasts to 2030 (US$ Bn)

- 9.1.1.2.1 UK: Europe Airline Ancillary Services Market Breakdown by Type

- 9.1.1.2.2 UK: Europe Airline Ancillary Services Market Breakdown by Carrier Type

- 9.1.1.3 Germany: Europe Airline Ancillary Services Market Revenue and Forecasts to 2030 (US$ Bn)

- 9.1.1.3.1 Germany: Europe Airline Ancillary Services Market Breakdown by Type

- 9.1.1.3.2 Germany: Europe Airline Ancillary Services Market Breakdown by Carrier Type

- 9.1.1.4 France: Europe Airline Ancillary Services Market Revenue and Forecasts to 2030 (US$ Bn)

- 9.1.1.4.1 France: Europe Airline Ancillary Services Market Breakdown by Type

- 9.1.1.4.2 France: Europe Airline Ancillary Services Market Breakdown by Carrier Type

- 9.1.1.5 Sweden: Europe Airline Ancillary Services Market Revenue and Forecasts to 2030 (US$ Bn)

- 9.1.1.5.1 Sweden: Europe Airline Ancillary Services Market Breakdown by Type

- 9.1.1.5.2 Sweden: Europe Airline Ancillary Services Market Breakdown by Carrier Type

- 9.1.1.6 Spain: Europe Airline Ancillary Services Market Revenue and Forecasts to 2030 (US$ Bn)

- 9.1.1.6.1 Spain: Europe Airline Ancillary Services Market Breakdown by Type

- 9.1.1.6.2 Spain: Europe Airline Ancillary Services Market Breakdown by Carrier Type

- 9.1.1.7 Russia: Europe Airline Ancillary Services Market Revenue and Forecasts to 2030 (US$ Bn)

- 9.1.1.7.1 Russia: Europe Airline Ancillary Services Market Breakdown by Type

- 9.1.1.7.2 Russia: Europe Airline Ancillary Services Market Breakdown by Carrier Type

- 9.1.1.8 Norway: Europe Airline Ancillary Services Market Revenue and Forecasts to 2030 (US$ Bn)

- 9.1.1.8.1 Norway: Europe Airline Ancillary Services Market Breakdown by Type

- 9.1.1.8.2 Norway: Europe Airline Ancillary Services Market Breakdown by Carrier Type

- 9.1.1.9 Denmark: Europe Airline Ancillary Services Market Revenue and Forecasts to 2030 (US$ Bn)

- 9.1.1.9.1 Denmark: Europe Airline Ancillary Services Market Breakdown by Type

- 9.1.1.9.2 Denmark: Europe Airline Ancillary Services Market Breakdown by Carrier Type

- 9.1.1.10 Finland: Europe Airline Ancillary Services Market Revenue and Forecasts to 2030 (US$ Bn)

- 9.1.1.10.1 Finland: Europe Airline Ancillary Services Market Breakdown by Type

- 9.1.1.10.2 Finland: Europe Airline Ancillary Services Market Breakdown by Carrier Type

- 9.1.1.11 Austria: Europe Airline Ancillary Services Market Revenue and Forecasts to 2030 (US$ Bn)

- 9.1.1.11.1 Austria: Europe Airline Ancillary Services Market Breakdown by Type

- 9.1.1.11.2 Austria: Europe Airline Ancillary Services Market Breakdown by Carrier Type

- 9.1.1.12 Rest of Europe: Europe Airline Ancillary Services Market Revenue and Forecasts to 2030 (US$ Bn)

- 9.1.1.12.1 Rest of Europe: Europe Airline Ancillary Services Market Breakdown by Type

- 9.1.1.12.2 Rest of Europe: Europe Airline Ancillary Services Market Breakdown by Carrier Type

- 9.1.1 Europe Airline Ancillary Services Market Revenue and Forecasts and Analysis - By Countries

10. Competitive Landscape

- 10.1 Heat Map Analysis By Key Players

- 10.2 Company Positioning & Concentration

11. Europe Airline Ancillary Services Market Industry Landscape

- 11.1 Overview

- 11.2 Market Initiatives

- 11.3 New Product Developments

12. Company Profiles

- 12.1 United Airlines Holdings Inc

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Delta Air Lines Inc

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 EasyJet Plc

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Deutsche Lufthansa AG

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Ryanair Holdings Plc

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Air France KLM SA

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners

- 13.2 Word Index