|

|

市場調査レポート

商品コード

1266271

キャリアニュートラル部門の2022年のOPEXでは光熱費が急増:多くのキャリアニュートラル事業者にとって光熱費は最大の運営費用であり、OPEX (ex-D&A) の最大80%を占めることもEnergy Costs Spike 2022 Opex for Carrier-neutral Sector: For Many Carrier-neutral Operators, Energy is Largest Operational Expense and Can Account for Up to 80% of Opex (ex-D&A), Costs Surged in 2022 for Many |

||||||

|

|

|||||||

| キャリアニュートラル部門の2022年のOPEXでは光熱費が急増:多くのキャリアニュートラル事業者にとって光熱費は最大の運営費用であり、OPEX (ex-D&A) の最大80%を占めることも |

|

出版日: 2023年04月20日

発行: MTN Consulting, LLC

ページ情報: 英文 6 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

光熱費は、インフラに特化したキャリアニュートラルネットワークオペレーター (CNNO) の運営費用の大部分を占めており、OPEX (ex-D&A) の30%以上、最大で80%を光熱費に費やすことがあります。

当レポートでは、セルタワー、データセンター、ファイバーネットワークオペレーターによるエネルギー支出に関するデータを示し、そのデータの意味と今後の方向性について論じています。

図表

調査対象

掲載企業

|

|

目次

- サマリー

- CNNO:他のオペレータータイプよりもエネルギー集約型

- ネットワークの持続可能性:CNNOから始める必要がある

- 影響

- 付録

List of Figures

- Figure 1: Power intensity by operator type (MWh consumed per US$1M in revenue)

- Figure 2: Utilities spend as a % of opex (excluding depreciation & amortization), 2020-22

- Figure 3: Utilities vs. D&A costs as a percentage of total opex, 2022

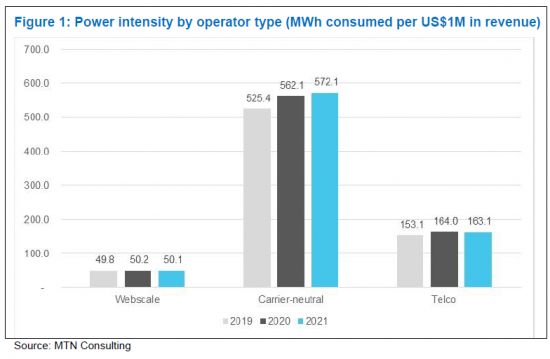

This brief presents data on energy spending by operators of cell towers, data centers, and fiber networks, and discusses the implications of the data and likely future directions. Utilities represent a large portion of operating expenses for these infrastructure-focused companies, which we track as "carrier-neutral network operators" (CNNOs). CNNOs also spend more than other types of operators. Webscale spending on power is miniscule relative to their size, less than 1% of opex (ex-D&A). Telcos spend a few % of opex (ex-D&A) on utilities. But CNNOs can spend more than 30% and up to 80% of opex (ex-D&A) on utilities.

VISUALS

Coverage

Companies mentioned:

|

|

Table of Contents

- Summary

- CNNOs are more energy-intensive than other operator types

- Sustainability in networks needs to start with CNNOs

- Implications

- Appendix