|

|

市場調査レポート

商品コード

1172495

業界再編の中でのキャリアニュートラルの成長鈍化 (2022年):市場の年間収益が1,000億米ドルに迫り、オペレーター業界の健全性を支える中心的存在だが、経済的な圧力には弱く、プライベートエクイティ企業が台頭するCarrier-neutral Growth Slows in 2022 Amid Consolidation: Market Approaches $100B in Annual Revenues, Still Central to Operator Industry Health, But Not Immune to Economic Pressures, Private Equity Players Ramp Up |

||||||

|

|

|||||||

| 業界再編の中でのキャリアニュートラルの成長鈍化 (2022年):市場の年間収益が1,000億米ドルに迫り、オペレーター業界の健全性を支える中心的存在だが、経済的な圧力には弱く、プライベートエクイティ企業が台頭する |

|

出版日: 2022年12月14日

発行: MTN Consulting, LLC

ページ情報: 英文 8 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

CNNOの収益は、2022年第3四半期に約239億米ドルに達し (対前年成長率 (YoY) 3%増)、年率換算では948億米ドルの規模となりました (YoY6%増)。これは、2021年の年間成長率 (12.5%) や、2011年~2021年の平均年間成長率 (16.6%) を大きく下回っています。2021年には企業合併・買収 (M&A) や設備投資が相次ぎましたが、収益成長にはまだあまり貢献していません。その要因として、販売サイクルの長期化、リース契約の再交渉圧力、市場の成熟に伴う価格競争の激化、ドル高などが挙げられます。一方、CNNOセクターの収益性は向上しています。平均フリーキャッシュフローマージンは、2011年から21年のほとんどの期間においてマイナスでしたが、ここ3期の四半期は11~14%の範囲に収まっています。金利が上昇するなか、CNNOはこれ以上の負債を負うことに消極的で、代わりに利益率の増加に焦点をあてています。CNNOはネットワークの経済性を改善し、より多くのトラフィックをオンネットで維持し、主要顧客にエンド・ツー・エンドのサービスを提供し、インフラの種類を超えたクロスセルを行うためにネットワークの構築を続けていくと思われます。

当レポートでは、世界のキャリアニュートラル・ネットワークオペレーター (CNNO) 市場の2022年第3四半期 (3Q22) までの最新情勢について調査しております。

本文中の図表

当レポートで言及された企業

|

|

目次

- 概要

- キャリアニュートラル市場における独自の課題の分析

- 市場の総収益額と成長率

- 主要企業の概要

- 設備投資額:今後2年間で企業合併・買収 (M&A) を上回る可能性と、技術コンポーネントの拡大

- 統合型ビジネスモデル:PEセクターの後押しを受けた拡大傾向

- 付録

List of Figures and Tables

- Figure 1: CNNO revenues, capex and M&A spending, annualized, 1Q14-3Q22

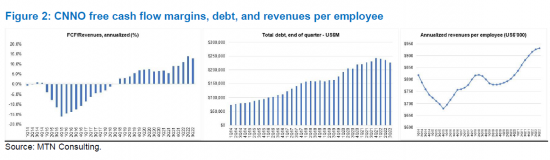

- Figure 2: CNNO free cash flow margins, debt, and revenues per employee

- Table 1: Overview of key CNNOs - recent financial metrics and M&A activity

This short note provides a brief review of the development of the carrier-neutral network operator (CNNO) market through the third quarter of 2022 (3Q22).

VISUALS

CNNO revenues were approximately $23.9 billion (B) in 3Q22, up 3% YoY, and $94.8B for the annualized 3Q22 period (4Q21-3Q22), up 6% YoY. These growth rates are significantly less than the 12.5% growth seen in CY2021 and the average growth over the 2011-21 period of 16.6% per year. That's despite the acquisition spree the sector observed in 2021, when M&A spend of $42.1B easily outpaced capex of $31.4B. This M&A and capex spending have expanded the asset base of the sector, but not helped much with revenue growth, yet. Companies point to longer sales cycles, pressure to renegotiate leases, increased price competition as the market matures, and appreciation of the US dollar among the factors keeping a check on revenue growth. However, there are signs that the CNNO sector is becoming more profitable: average free cash flow margin has been in the 11-14% range for the last three quarters, while it was negative for most of the 2011-21 period. Debt remains high, totaling $225B in 3Q22, only slightly down from 3Q21; with higher interest rates, CNNOs are reluctant to take on more debt, instead focusing on margin growth. CNNOs will continue to build out their networks to improve network economics, keep more traffic on-net, provide key customers more of an end-to-end service, and cross sell across infrastructure types.

Private equity firms continue to invest heavily in the sector, and many have "digital infrastructure" funds aiming to combine assets across the three main infrastructure classes: towers, data centers, and fiber. As we argued in a July 2021 report, we continue to expect that "A new breed of integrated owners of infrastructure network assets will emerge over the next 2-3 years, converging towers, data centers, and fiber networks." PE firms' capital inflows are pushing this integration. A large group of well-funded PE firms are pursuing digital infrastructure opportunities. Some are explicitly aiming to assemble portfolios of integrated assets, and/or cobble them together into larger CNNOs able to address multi-sector opportunities from a position of massive scale. Ultimately most PEs do aim for liquidity events from these past investments, though some are content with the relatively steady cash flows spun off by CNNOs.

We will be formally updating our operator forecast soon. This update will include revised projections for the market, incorporating actual market data as reported through 3Q22.

Companies Mentioned:

|

|

Table of Contents

- Summary

- Measurement a unique challenge in carrier-neutral market

- Top line market growth

- Overview of key companies

- Capex likely to exceed M&A in next 2 years, and tech component will rise

- Integrated business models also to pick up, with boost from PE sector

- Appendix