|

市場調査レポート

商品コード

1441631

民間航空機材料:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Commercial Aircraft Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 民間航空機材料:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 92 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

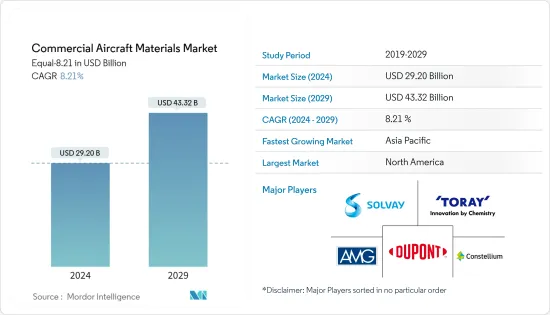

民間航空機材料市場規模は、2024年に292億米ドルと推定され、2029年までに433億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に8.21%のCAGRで成長します。

航空機に使用される材料の最適な特性は、高強度、軽量、優れた耐熱性です。これらの材料は耐久性があり、かなりの寿命を持っています。これまで、航空機の構造は主にチタン合金とアルミニウム合金に依存しており、これらの合金が全構成元素の約80%を占めていました。

金属合金よりも複合材料の使用が増加することで、将来的に市場が大きく推進されると予想されます。複合材料は、他の材料に比べて高い強度重量比、高温耐性、および耐破壊性を備えており、この要因が民間航空機製造における複合材料の大規模採用を促進しています。

軽量かつ燃料効率の高い航空機に対する需要の高まりは、世界の航空機材料市場の成長を促進する重要な要因です。航空機の軽量化により、運航に関連するコストが大幅に削減され、燃料効率が向上するため、航空機運航会社の収益性が向上します。

民間航空機材料市場の動向

ナローボディ航空機セグメントは予測期間中に最高の成長を遂げる

現在、狭胴機セグメントは旅客機カテゴリーの中で優勢であり、世界シェアの80%を占めています。格安航空会社の利用増加により、予測期間中も優位性が続くと予想されます。この要因により、短距離路線での低運航コストや燃料効率などの利点を備えた、新世代の狭胴機に対する膨大な需要が生じました。

航空会社は、特に短距離路線の航空会社にとって実現可能となったため、広胴機から狭胴機への移行を進めています。狭胴機の需要の急増により、OEMは航空機の生産を増加させています。セラミックおよび金属マトリックス複合材、繊維強化ポリマー、カーボンカーボン複合材などの複合材は、その優れた特性により航空機製造会社で使用されています。

いくつかの航空会社は、路線範囲と市場シェアを強化するための全体的な戦略の一環として、機材の拡充を実施しています。たとえば、2023年 6月に、IndiGoはエアバス A320ファミリー航空機を500機発注しました。燃料効率の高いA320NEOファミリー航空機により、インディゴは運航コストの削減と高水準の信頼性を備えた燃料効率の実現に重点を置き続けることができます。 2023年から2028年にかけて、約10,000機の狭胴機が世界中に納入される予定です。

北米は予測期間中も優位性を維持する

北米の民間航空産業は、長年にわたって世界の航空市場において重要な役割を果たしてきました。この地域における民間航空活動の需要は、飛行機で旅行する乗客数が毎年増加していることによって促進されています。 2022年、この地域の航空旅客数は60億人に達しました。米国が83%と最大のシェアを占め、続いてカナダ、メキシコ、北米のその他の地域がそれぞれ8%、6%、2%を占めています。

さらに、複合材料の需要の増加に伴い、企業は高度な複合材料を開発するための新しい施設を開設しています。たとえば、2021年 7月に、RTXの一部門であるプラットアンドホイットニーは、米国カールスバッドにセラミックマトリックス複合材料(CMC)エンジニアリングおよび開発施設を開設すると発表しました。施設の面積は60,000平方フィートを超えます。これは、航空宇宙用途向けのセラミックマトリックス複合材料(CMC)の開発、統合エンジニアリング、および低レート生産に使用されます。

航空機の近代化プログラムの一環として米国とカナダで運航している航空会社の膨大な注文が需要を押し上げています。 2023年5月、エア・カナダはボーイングB787ドリームライナーを最大20機購入する計画を発表しました。この地域の大手航空会社によるこうした新型航空機の発注により、今後数年間で航空機材料の需要が増加すると予想されています。

民間航空機材料業界の概要

民間航空機材料市場は、接着剤、化学薬品、複合材料、金属および非金属材料、プラスチックなどを提供するさまざまなプレーヤーによって細分化されています。市場の著名なプレーヤーには、ソルベイ SA、東レ株式会社、コンステリウム、デュポンなどがあります。

市場では、材料技術におけるコラボレーション、買収、革新が増加しており、市場の成長を支えています。たとえば、2021年 9月、Hexcel Corpは、ボーイング B777X用のHexPEKK-100材料で作られた航空宇宙構造物を製造する複数年契約を締結しました。この契約に基づき、HexPEKK部品は、航空機の気流ダクト用途やその他のサポート要素向けに、ハートフォード近郊のHexcelの積層造形施設で製造されます。航空機OEMとのこのようなパートナーシップは、今後数年間で同社の成長を推進すると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 航空機タイプ

- ナローボディ航空機

- ワイドボディ航空機

- リージョナルジェット

- 材料

- 複合材料

- アルミニウム合金

- 鋼鉄

- その他の材料

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- その他の中東およびアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Solvay SA

- Hexcel Corporation

- Toray Industries Inc.

- Constellium

- DuPont de Nemours Inc.

- Arconic Inc.

- ATI Inc.

- AMG Critical Materials NV

- Novelis Deutschland GmbH

- Notus Composites FZC

- VSMPO-AVISMA Corporation

第7章 市場機会と将来の動向

The Commercial Aircraft Materials Market size is estimated at USD 29.20 billion in 2024, and is expected to reach USD 43.32 billion by 2029, growing at a CAGR of 8.21% during the forecast period (2024-2029).

The optimal attributes for materials used in aircraft are high strength, low weight, and exceptional resistance to heat. These materials exhibit durability and possess a significant lifespan. In the past, aeronautical construction predominantly relied on titanium alloy and aluminum alloy, which comprised approximately 80% of all constituent elements.

Increasing the use of composite materials over metal alloys is expected to significantly drive the market in the future. Composites provide a high strength-to-weight ratio, high temperature, and fracture resistance over other materials, and this factor is fuelling the large-scale adoption of composites in commercial aircraft manufacturing.

The growing demand for aircraft that are both lightweight and fuel-efficient is a key factor driving the growth of the global aircraft materials market. Due to the reduced weight of the aircraft, the costs associated with operating the flights are significantly decreased, resulting in increased profitability for the aircraft operators because of improved fuel efficiency.

Commercial Aircraft Materials Market Trends

Narrow-body Aircraft Segment to Witness the Highest Growth During the Forecast Period

The narrowbody aircraft segment currently dominates the passenger aircraft category, with 80% of the global share. It is expected to continue its dominance during the forecast period due to the increase in the utilization of low-cost carriers. This factor resulted in huge demand for newer generation narrowbody aircraft, with advantages such as low cost of operation and fuel efficiency in short-haul routes.

Airline companies are shifting from widebody aircraft to narrowbody aircraft as they have become particularly doable for airlines for short-haul routes. The surge in demand for narrowbody aircraft is driving OEMs to increase their production of aircraft. Composites such as ceramic and metal matrix composites, fiber-reinforced polymers, carbon-carbon composites, etc., are used in aircraft manufacturing companies because of their favorable properties.

Several airlines are implementing fleet expansion as part of their overall strategies to enhance their route coverage and market share. For instance, in June 2023, IndiGo orders 500 Airbus A320 family aircraft. The fuel-efficient A320NEO family aircraft will allow IndiGo to maintain its strong focus on lowering operating costs and delivering fuel efficiency with high standards of reliability. During 2023-2028, around 10,000 narrowbody aircraft are expected to deliver across the globe.

North America to Continue its Dominance During the Forecast Period

The commercial aviation industry in North America has long been a significant player in the global aviation market. The demand for commercial aviation activity in the region is driven by the rising number of passengers traveling by air annually. In 2022, the region's air passenger traffic stood at 6 billion. The US accounted for the largest share which is 83%, followed by Canada, Mexico, and the Rest of North America accounted for 8%, 6%, and 2% respectively.

Furthermore, with the increasing demand for composites, companies are opening new facilities to develop advanced composites. For instance, in July 2021, Pratt & Whitney, a division of RTX, announced the inauguration of a ceramic matrix composites (CMCs) engineering & development facility in Carlsbad, the US. The facility has an area of over 60,000 square feet. It will be used for developing, integrating engineering, and low-rate production of Ceramic Matrix Composites (CMCs) for aerospace applications.

The huge order book of airlines operating in the US and Canada as a part of their fleet modernization programs is driving the demand. In May 2023, Air Canada announced that it is planning to purchase up to 20 Boeing B787 Dreamliners. Such orders for new aircraft by major airlines in the region are expected to boost the demand for aircraft materials in the coming years.

Commercial Aircraft Materials Industry Overview

The commercial aircraft materials market is fragmented due to various players providing adhesives, chemicals, composites, metals and non-metal materials, plastics, etc. Some of the prominent players in the market are Solvay SA, Toray Industries, Inc., Constellium, DuPont de Nemours, Inc., and AMG Critical Materials N.V., among others. Solvay is the major provider of composites to major aircraft programs like Airbus A220, Boeing B737, Boeing B777, Boeing B787 Dreamliner, COMAC C919, and Airbus A350. In addition to the aforementioned players, companies like General Plastics Manufacturing Company, Inc. and Alcoa Corporation provide plastic materials and metal. Alcoa Corporation provides metal and alloy products for Airbus A320, Airbus A330, Airbus A350, Boeing B737 MAX, Boeing B787 Dreamliner, and COMAC C919 aircraft programs.

The market is witnessing increased collaborations, acquisitions, and innovations in material technology, supporting the market growth. For instance, in September 2021, Hexcel Corp was awarded a multi-year contract to manufacture aerospace structures made with HexPEKK-100 material for the Boeing B777X. Under the agreement, the HexPEKK parts will be manufactured at Hexcel's additive manufacturing site near Hartford for airflow ducting applications and other supporting elements on the aircraft. Such partnerships with aircraft OEMs are expected to propel the company's growth in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Narrow-Body Aircraft

- 5.1.2 Wide-Body Aircraft

- 5.1.3 Regional Jets

- 5.2 Material

- 5.2.1 Composites

- 5.2.2 Aluminum Alloys

- 5.2.3 Steel

- 5.2.4 Other Materials

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Solvay SA

- 6.2.2 Hexcel Corporation

- 6.2.3 Toray Industries Inc.

- 6.2.4 Constellium

- 6.2.5 DuPont de Nemours Inc.

- 6.2.6 Arconic Inc.

- 6.2.7 ATI Inc.

- 6.2.8 AMG Critical Materials N.V.

- 6.2.9 Novelis Deutschland GmbH

- 6.2.10 Notus Composites FZC

- 6.2.11 VSMPO-AVISMA Corporation