|

市場調査レポート

商品コード

1910633

硬質プラスチック包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Rigid Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 硬質プラスチック包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

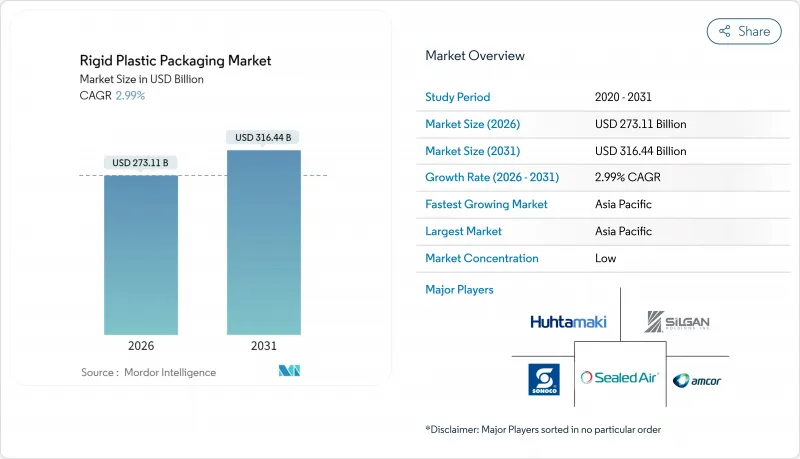

硬質プラスチック包装市場は、2025年の2,651億8,000万米ドルから2026年には2,731億1,000万米ドルへ成長し、2026年から2031年にかけてCAGR2.99%で推移し、2031年までに3,164億4,000万米ドルに達すると予測されております。

持続可能性への要請とサプライチェーンのレジリエンス需要に牽引され、量と価値創出のバランスが取れた着実な拡大段階が強調されています。硬質プラスチック包装市場は、耐衝撃性フォーマットを好む電子商取引の成長、単一素材設計を奨励する規制圧力、食品・ヘルスケア分野における単回使用需要を押し上げる人口動態動向の恩恵を受けています。生産者は拡大生産者責任(EPR)コスト曲線に対応するため再生材含有率の統合を強化し、リサイクル資産への垂直統合により原料の可視性を確保し、ポリマー価格変動への緩衝を図っています。アジア太平洋地域は規模・政策インセンティブ・急速な都市部消費で主導的立場にあり、欧州は厳格な循環型経済規制を活かし高級ソリューションを加速、北米は堅牢な容器を要するコールドチェーン物流を推進しています。主要コンバーターが調達力・技術革新の幅・コンプライアンス対応力を強化するため合併を進める中、競合激化により中小企業の参入障壁が再設定されています。

世界の硬質プラスチック包装市場の動向と洞察

循環型経済の義務化が再生材包装需要を牽引

現在63カ国がリサイクル可能性に応じて急激に増加するEPR(拡大生産者責任)費用を課しており、コスト構造を消費後再生材(PCR)原料と単一素材設計に有利にシフトさせています。PCR PETがバージン樹脂に対して10~15%のプレミアムを形成することで従来の価格階層が逆転し、コンバーターは買収や長期契約を通じて再生材供給を確保するよう促されています。デンマークの2025年データ報告規則への対応に伴い、デジタルトレーサビリティシステムが台頭し、エンドツーエンドの透明性が加速しています。EUのリサイクル義務期限が迫る中、食品グレードの認証取得が可能な洗浄・押出・化学リサイクル施設へ資本が流入。この要因が規模拡大投資の根拠となり、硬質プラスチック包装市場が数量指標から循環価値指標へ転換する流れを強化しています。

電子商取引の急増により、耐衝撃性のある出荷対応フォーマットへの需要が加速

消費者直販(D2C)物流では、一次容器が従来小売ルートより40%高い取扱力に晒され、ブランドオーナーの故障コストリスクが高まります。特に射出成形トレイや熱成形トレイといった硬質設計は二次包装なしで衝撃を吸収し、容積重量料金と破損返品を削減します。小売業者は自動倉庫で50kg超の積載に耐える頑丈な形態を推奨する「自社容器での出荷」プロトコルを義務付けています。現在、革新の焦点は内容物を保護しつつ樹脂使用量を削減するコーナー補強構造と内蔵クッションリブに注がれています。この構造要件は持続可能性の要請とも合致します。厚みのある再利用可能な硬質容器は、ラストマイル配送における使い捨て段ボール廃棄物を相殺するからです。こうした動向が硬質プラスチック包装市場の成長と革新を牽引しています。

高まるポリマー価格の変動性がコンバーターの利益率を圧迫

原料供給の混乱により、2024年には6か月間でポリエチレン価格が35%も変動し、固定価格契約に縛られたコンバーターを圧迫しました。ヘッジ能力が限られる中小企業は設備稼働率70%未満で操業し、運転資金ラインの契約違反リスクに直面しています。アジアのオレフィンクラッカーはマイナススプレッド対策として稼働率を削減し、樹脂供給を制約するとともにスポットプレミアムを押し上げています。硬質プラスチック包装市場はコストショックを不均等に吸収しており、世界の大手は規模の経済を活かした契約を活用する一方、地域企業は投資を遅らせ、生産能力の近代化が遅れています。

セグメント分析

2025年における硬質プラスチック包装市場規模の42.83%をボトル・ジャーが占め、飲料・パーソナルケア・市販薬分野での定着した需要を反映しています。優れた透明性・改ざん防止機能・ラベル適合性により、軽量化推進による単位樹脂使用量の削減が進んでも需要は安定しています。イノベーションとしては、使い捨てプラスチック規制に対応しリサイクル性を向上させるテザー付きキャップなどが挙げられます。成長は破壊的技術革新よりも飲料生産量に連動しており、このセグメントは大規模コンバーターにとって安定した収益基盤となっています。

パレットはシェアこそ小さいもの、RFID内蔵・IoT対応の積載容器を重視するEC自動化に牽引され、4.43%のCAGRで最も急成長する製品です。再利用可能なプラスチックパレットは耐久性と衛生面で木材を上回り、医薬品や生鮮食品のコールドチェーンにおいて極めて重要です。標準化された形状は高層倉庫のロボット化を促進し、シリアル化により資産追跡データサービスが実現され、付加収益を生み出します。小売業者がクローズドループ・プーリングシステムを導入する中、パレット供給業者は追跡ソフトウェアとハードウェアをセット化し、硬質プラスチック包装市場においてサービス主導の差別化を図っています。

PETは2025年、優れたバリア特性と確立されたボトル・トゥ・ボトルリサイクルループにより、硬質プラスチック包装市場シェアの31.05%を維持しました。欧州のデポジット制度はPET回収率76.7%を達成し、高PCR含有率によるEPR責任の軽減を可能にしています。しかしながら、政策やブランドの取り組みがバイオベース原料を優先する中、バイオプラスチックは4.98%のCAGRを示しています。中国におけるPBAT年産70万トン、PLA年産10万トンの生産能力拡大は供給を安定化させ、価格プレミアムを徐々に縮小させています。

バイオベース樹脂による温室効果ガス削減をカーボンクレジット制度が金銭化することで、ライフサイクル経済性が変化しています。主要飲料ブランドは100%バイオPETボトルの試験導入を進め、キャップメーカーのプログラムは植物由来HDPEへ移行中です。したがって、硬質プラスチック包装市場は、従来の石油化学チェーンにおけるコスト効率と、規制強化に備えたポートフォリオの将来性を確保する低炭素ポリマーへの戦略的多様化とのバランスを取っています。

本「硬質プラスチック包装レポート」は、製品タイプ別(ボトル・ジャー、トレイ・容器など)、素材別(ポリエチレン、ポリエチレンテレフタレート、ポリプロピレンなど)、エンドユーザー産業(食品、ヘルスケア、化粧品・パーソナルケア、工業など)、製造プロセス(射出成形、押出ブロー成形など)、地域別に分析しております。市場予測は金額ベース(米ドル)で提示されます。

地域別分析

アジア太平洋地域は2025年の硬質プラスチック包装売上高の38.85%を占め、5.62%のCAGRで拡大が見込まれています。これは、インドにおける14億6,000万米ドルの生産連動型投資(PLI)誘致と、地域のサプライチェーンを支える中国の生分解性プラスチックの拡大に支えられています。現地のコンバーターは世界のブランドと歩調を合わせ、輸送時の排出量を削減するため消費者の近くで生産拠点を設置し、生産能力を拡大しています。リサイクル可能またはバイオベースの包装材への規制転換は、技術移転提携を結ぶ企業に先行者優位性をもたらします。

北米では、電子商取引とコールドチェーン医薬品の拡大に伴い、長距離物流経路における製品品質を保持する堅牢な容器への需要が持続的に増加しています。州レベルの拡大生産者責任(EPR)提案により設計の見直しが促されていますが、実施時期のばらつきにより規制対応の急激な影響は緩和されています。高い平均所得水準がプレミアムな単回使用フォーマットを支え、高利益率の硬質プラスチックセグメントの販売数量を後押ししています。

欧州では需要量は成熟していますが、循環型経済に関する積極的な指令により高付加価値密度が特徴です。包装および包装廃棄物規制(PPWR)は単一素材ソリューションの導入を促進し、リサイクルインフラへの資本流入を加速させ、150億米ドル規模のコンプライアンス市場を形成しています。ドイツ、オランダ、フランスのイノベーションクラスターでは化学的リサイクルのパイロット事業が先行し、地域でのPCR(ポストコンシューマ再生材)供給を確保するとともに、アジア向け輸出ルートを確立しています。

南米、中東・アフリカ地域では、収集量の不足や政策の遅れにより、新興の機会が抑制されています。多国籍企業はモジュール式リサイクルプラントを展開し、現地のPCR(再生プラスチック)を確保するとともに、世界の含有率目標の達成を目指しています。南アフリカのEPR法(拡大生産者責任制度)やケニアの生産者責任法案は、設計基準の強化と適合性のある硬質プラスチックソリューションへの需要拡大につながる政策の収束を示しています。投資優遇措置と低い労働コストが押出機や射出成形ラインの移転を誘致し、これらの地域は硬質プラスチック包装市場における将来の輸出拠点としての地位を確立しつつあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 循環型経済の義務化が再生材含有包装の需要を牽引

- 電子商取引の急増により、耐衝撃性のある出荷対応フォーマットへの需要が加速しております

- 世帯規模の縮小傾向がシングルサーブ向け硬質容器需要を促進

- 2027年EUリサイクル目標達成に向けた高障壁単一素材ソリューションの導入

- 超頑丈な硬質コンテナを必要とするコールドチェーン物流の急速な成長

- 市場抑制要因

- 高まるポリマー価格の変動性がコンバーターの利益率を圧迫

- 消費者の柔軟性のある紙ベースの代替品への移行が増加

- 拡大生産者責任(EPR)費用による総所有コストの上昇

- 新興経済国におけるリサイクルインフラの不足がPCR供給を制限している

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- マクロ経済要因が市場に与える影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- 瓶・ジャー

- トレイ・び容器

- 中間バルクコンテナ(IBC)

- パレット

- その他の製品タイプ

- 素材別

- ポリエチレン(PE)

- ポリエチレンテレフタレート(PET)

- ポリプロピレン(PP)

- ポリスチレン(PS)および発泡ポリスチレン(EPS)

- バイオプラスチック

- その他の素材

- エンドユーザー産業別

- 食品

- 飲料

- ヘルスケア

- 化粧品・パーソナルケア

- 産業

- 建築・建設

- 自動車

- その他のエンドユーザー産業

- 製造工程別

- 射出成形

- 押出ブロー成形

- 射出ブロー成形

- ストレッチブロー成形

- 熱成形

- 回転成形

- 圧縮成形

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- メキシコ

- その他南米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ポーランド

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- タイ

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amcor plc

- Alpha Packaging Holdings, Inc.

- ALPLA Werke Alwin Lehner GmbH & Co KG

- Silgan Holdings Inc.

- Sealed Air Corporation

- Plastipak Holdings, Inc.

- Sonoco Products Company

- Resilux NV

- Graham Packaging Company, L.P.

- Greif, Inc.

- Mauser Packaging Solutions Holding Company

- Pact Group Holdings Ltd

- Gerresheimer AG

- Huhtamaki Oyj

- Coveris Management GmbH

- Logoplaste Consultores Tecnicos SA

- International Paper Company(DS Smith Plc)

- Weener Plastics Group BV

- Anchor Packaging LLC

- Visy Industries Holdings Pty Ltd

- Altium Packaging LLC

- Serioplast Group SpA

- Mpact Limited