|

市場調査レポート

商品コード

1910591

リチウムイオン電池セパレータ:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Lithium-ion Battery Separator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| リチウムイオン電池セパレータ:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 165 Pages

納期: 2~3営業日

|

概要

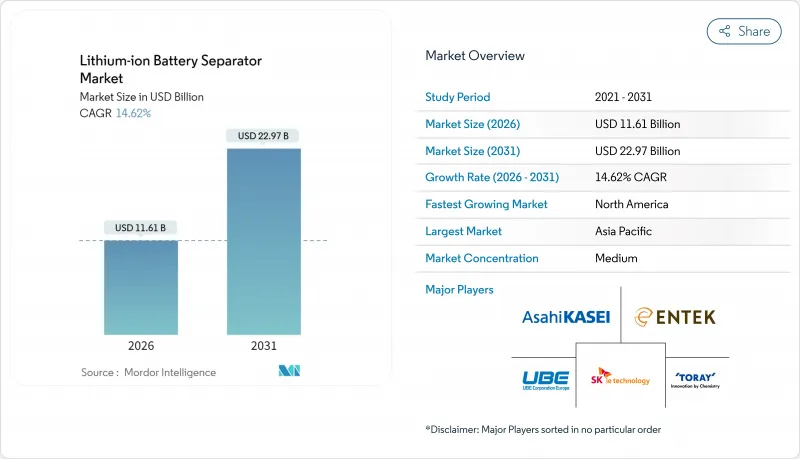

リチウムイオン電池用セパレータ市場は、2025年の101億3,000万米ドルから2026年には116億1,000万米ドルへ成長し、2026年から2031年にかけてCAGR 14.62%で推移し、2031年には229億7,000万米ドルに達すると予測されております。

新たな需要は電気自動車(EV)および大規模蓄電システムに起因しており、これらは高ニッケル化学組成や過酷な急速充電プロファイルに耐える超薄型セラミックコーティング膜をますます要求しています。湿式プロセスによるポリオレフィン製セパレータが依然として主流ですが、自動車メーカーが熱伝播防止対策を強化するにつれ、コーティング加工品が急速に成長しています。資本は国内調達義務のある地域へ流入しています。旭化成の15億6,000万カナダドル規模のオンタリオ複合施設は、供給構造を再編する先駆者優遇策の好例です。一方、北米の税額控除、欧州のバッテリー規制、中国のギガファクトリー建設は、世界の貿易フローを分断し、地域調達を認証しつつコスト効率的な樹脂統合を習得したサプライヤーを優遇しています。

世界リチウムイオン電池セパレーター市場の動向と洞察

リチウムイオン電池価格の低下

2024年にはパック価格が100米ドル/kWhを下回りました。これは炭酸リチウムコストの低下と中国のセル過剰生産能力が寄与しています。価格弾力性の拡大により新興市場でのEV普及が進み、セパレーターの平方メートル当たりの需要も連動して増加しています。セルメーカーがライン効率化のためにコーティング工程を外部委託する傾向が強まり、コーティングフィルムのシェアが拡大。これにより新規統合工場の20%利益率目標が支えられています。コスト低下は技術更新サイクルの短縮も促し、耐久性を損なわずに薄膜化が進んでいます。

加速する世界のEV普及

2024年の世界のEV販売台数は1,700万台を突破し、約21億平方メートルのセパレーター材料を消費しました。高ニッケル正極材は発熱を増加させるため、200℃以上でも安定するセラミックコーティングまたはアラミド強化セパレーターの採用が求められます。ホンダの2040年以降のロードマップなど、自動車メーカーの電動化への取り組みにより、複数年にわたるセパレーター契約が締結され、市場の変動が緩和されます。

ポリオレフィン樹脂の需給不均衡

超高分子量ポリエチレンの生産能力は2022年以降、需要を8ポイント下回っており、樹脂価格の高騰と非統合型メーカーの苦境を招いています。旭化成の自社樹脂供給網は変動を緩和し、スポット樹脂競合他社と比較してライン速度を倍増させています。北米の供給不足により、新規参入企業は樹脂の輸入や、セピオン社のアラミド混紡樹脂などの代替ポリマーの採用を余儀なくされています。

セグメント分析

2025年時点で、湿式法ポリオレフィンはリチウムイオン電池用セパレータ市場の60.05%を占めております。この地位は均一な気孔率と1マイクロメートル未満の気孔制御技術によって築かれたものです。しかしながら、セラミックコーティング品はCAGR22.05%で拡大しており、175℃以上のシャットダウン温度を要求する自動車向け契約を獲得しています。インラインコーティングは成形とスラリー塗布を一体化し、歩留まり損失を2%未満に削減、利益率を5~7ポイント向上させます。

未コーティングのポリオレフィンは依然としてコスト重視のデバイス向けですが、スマートフォンでさえもより薄いコーティング分離膜へ移行する中、その存在感は薄れつつあります。PVDF-HFPブレンドなどの機能性ポリマーオーバーレイは、電解液接触角を5°未満に抑え、形成時間を40%短縮し、第三の技術フロンティアを示唆しています。

ポリプロピレンの48.02%というシェアは、成熟した押出ラインと低樹脂コストを反映しています。ポリエチレンは130℃の融点シャットダウン特性により湿式プロセス配合で引き続き優位ですが、多層PP/PE/PP積層構造が自動車向け出荷量の3分の1を占めるようになりました。不織布アラミドナノファイバー膜は、300℃での寸法安定性と200MPaを超える引張強度を維持しますが、価格は15~25米ドル/kgです。

低温重縮合によるコスト削減により、3年以内にアラミド価格が半減する可能性があり、高級電気自動車や航空宇宙分野での採用拡大が見込まれます。リサイクル課題は依然として存在します。ポリオレフィンフィルムはダウンサイクルが可能ですが、アラミドにはリサイクル経路がなく、欧州の2027年規制枠組みにおいて課題となっています。

リチウムイオン電池用セパレータ市場レポートは、セパレータタイプ(湿式プロセス、乾式プロセス、セラミックコーティング)、素材(ポリプロピレン、不織布その他)、厚さ(15ミリメートル以下、16~20ミリメートル、それ以上)、形状(パウチ型、円筒形、角形)、コーティング(無コーティングポリオレフィン、インラインセラミック、その他)、用途(自動車用EV、その他)、地域(北米、アジア太平洋、その他)で分類されています。

地域別分析

2025年時点で、アジア太平洋地域はリチウムイオン電池用セパレータ市場の49.75%を占めており、中国が世界の生産能力の75%を占めることで牽引されております。中国企業は樹脂の統合と労働力の優位性により、セパレータコストを日本の競合他社より30~40%削減いたしました。日本のシェアは、東レと住友化学が汎用品グレードから撤退し固体電池のニッチ市場へ移行したため、2018年の35%から2021年には20%に低下しました。韓国のSK IEテクノロジーは欧州で47.5GWhの電池生産能力を保有していますが、2024年には2,910億ウォンの損失を計上し、利益率の圧迫を示しています。

北米はCAGR21.43%で最も成長が速い地域であり、インフレ抑制法の優遇措置と50億米ドル超のセパレーター投資発表が後押ししています。旭化成のオンタリオ工場は2027年までに年間7億平方メートルの生産能力と地域シェア30%を目標としており、マイクロポーラス社とセピオン社はそれぞれバージニア州とカリフォルニア州で生産能力を拡大中です。政策の安定性は依然として重要であり、税額控除の廃止は資産の遊休化を招く恐れがあります。

欧州市場は、カーボンフットプリント規制と再生材含有率規制により、現地生産が優遇される構造です。SK IEテクノロジーのポーランド工場は3億4,000万m2の生産能力を追加しますが、同社の財務的圧迫が長期供給の見通しを不透明にしています。欧州のセルメーカーであるノースボルト、ACC、ヴェルコルは自社製セパレーターの開発を進めており、既存メーカーへの圧力をさらに強めています。南米と中東・アフリカ地域は依然として小規模ですが、ブラジルにおける2024年の15万台のEV導入やサウジアラビアの産業政策により、2027年以降に小規模な現地生産能力が生まれる可能性があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- リチウムイオン電池価格の低下傾向

- 加速する世界の電気自動車普及

- 据置型エネルギー貯蔵プロジェクトの急速な成長

- 国内電池サプライチェーンに対する政府の優遇措置

- 高ニッケル正極材向け超薄型セパレーターのOEM推進

- 地域別分離器ギガファクトリーを推進する現地化義務

- 市場抑制要因

- ポリオレフィン樹脂の需給不均衡

- 厳格な安全・品質認証のタイムライン

- 湿式プロセスラインにおける溶剤回収コストの課題

- 使用済み分離装置のリサイクル経路の制限

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- セパレータ別

- 湿式プロセス・ポリオレフィン

- ドライプロセス・ポリオレフィン

- セラミックコーティング

- 材料別

- ポリプロピレン(PP)

- ポリエチレン(PE)

- 多層PP/PE/PP

- 不織布およびその他

- 厚さ別

- 15マイクロメートル以下

- 16~20µm

- 21~25µm

- 25µm以上

- 電池の形状別

- パウチ型電池

- 円筒形電池

- 角形電池

- コーティング技術別

- インラインセラミックコーティング

- オフラインセラミックコーティング

- 機能性ポリマーコーティング

- 無コーティングポリオレフィン

- 用途別

- 自動車EV

- 民生用電子機器

- 据置型エネルギー貯蔵

- 産業用工具および電動工具

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- 北欧諸国

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- オーストラリアおよびニュージーランド

- その他アジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動き(M&A、提携、PPA)

- 市場シェア分析(主要企業の市場順位・シェア)

- 企業プロファイル

- Asahi Kasei Corporation

- Toray Industries Inc.

- SK IE Technology Co. Ltd

- Entek International LLC

- Ube Corporation

- Sumitomo Chemical Co. Ltd

- Celgard LLC(Polypore)

- W-Scope Corporation

- Shenzhen Senior Technology

- Cangzhou Mingzhu Plastic

- Suzhou GreenPower

- Sinoma Science & Tech

- Dreamweaver International

- Gellec Co. Ltd

- Zhongke Science & Tech

- Mitsubishi Paper Mills

- Foshan Jinhui Hi-Tech

- Freudenberg Performance Materials

- Xiangyang Xingyuan

- Teijin Ltd

- Others(validated niche players)