分子診断:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Molecular Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

- 発行日

- ページ情報

- 英文 233 Pages

- 納期

- 2~3営業日

- 商品コード

- 2044101

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

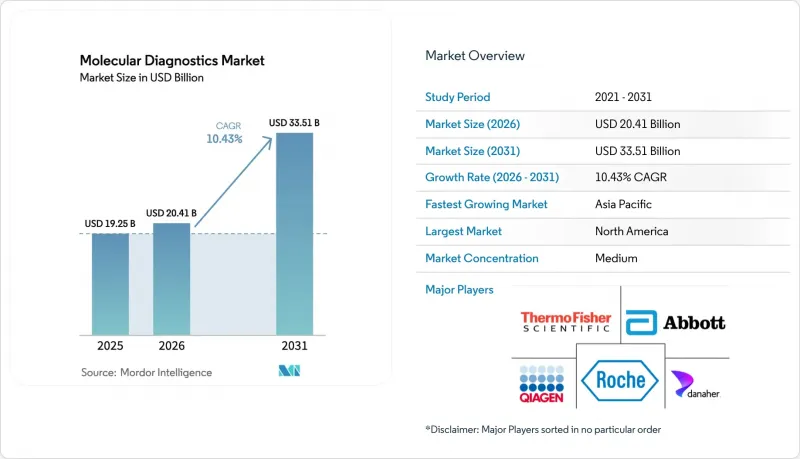

分子診断市場の規模は、2026年に204億1,000万米ドルに達すると見込まれており、2031年までに335億1,000万米ドルまで成長し、CAGRは10.43%になると予測されています。

ゲノムプロファイリングに対する保険適用範囲の拡大や、検査室開発検査(LDT)に対するより明確な規制プロセスの確立により、プレシジョン・メディシンが研究段階から日常的な医療へと移行する動きが促進されています。ゲノム1つあたり200米ドル未満のシーケンシング費用、迅速な全ゲノム解析プラットフォームに対するFDAのブレークスルーデバイス指定、およびCLIA免除検査の小売クリニックでの導入により、臨床へのアクセスが拡大しています。一方、欧州連合(EU)の体外診断用医療機器規則(IVDR)は、市販後監視を強化し、中小メーカーの利益率を圧迫しており、統合プラットフォームへの需要を集中させています。検査単価の低下、病院における多項目症候群パネルの導入、および製薬企業による社内ゲノムサービスへの垂直統合が相まって、腫瘍学、感染症、および公衆衛生プログラム全体での採用を加速させています。

世界の分子診断市場の動向と洞察

迅速なポイント・オブ・ケア分子診断への需要の高まり

ポイント・オブ・ケア(POC)プラットフォームは、診断サイクルを数日から数分に短縮し、即時の処方決定を可能にするとともに、救急診療所における不適切な抗生物質の使用を31%削減しています。ハンドヘルドシステムは15分以内に結果を提供し、電子カルテと連携することで、処理能力が収益性を左右する小売クリニックのワークフローに適合します。保険者は、再入院の減少による下流のコスト削減を認識しており、同等の償還制度により、中央検査室が従来持っていたコスト面での優位性は失われつつあります。小売薬局チェーンは2025年に呼吸器パネル検査の全国展開を発表し、大量検査を救急部門から移行させています。CLIA免除の認可が慢性疾患検査へと拡大するにつれ、消費者主導の検査はプライマリケア受診の日常的な要素となる見込みです。

コンパニオン診断と標的療法の統合

規制当局は現在、コンパニオン診断をほとんどの標的療法の前提条件と見なしています。FDAは2024年に、KRAS、NTRK、HER2のバイオマーカーと薬剤の組み合わせについて追加の承認を行い、単一ランによるゲノムプロファイリングの有用性を拡大しました。EMAのガイダンスでは、最初の医薬品申請時に検証データの提出が義務付けられており、これにより診断・治療薬の開発サイクルは短縮されますが、投資のハードルは高まっています。日本の迅速審査制度により、希少疾病用医薬品のコンパニオン診断の承認期間が10ヶ月に短縮され、希少な変異に対する検査法の開発が促進されています。腫瘍変異負荷(TMB)とマイクロサテライト不安定性(MSI)スコアを単一のワークフローに統合することで、組織の節約と報告の迅速化が図られ、マルチバイオマーカーパネルが標準治療となっています。製薬企業は、医薬品の市場アクセスを確保するために診断法の研究開発への資金提供を増加させており、それによってバリューチェーン全体でのインセンティブの整合が図られています。

高水準な分子プラットフォームの高額な資本コストと運用コスト

ベンチトップ型シーケンサーの価格は50万米ドル、ハイスループットシステムは100万米ドルを超えるため、地域病院にとっては導入の障壁となっています。年間30万米ドルを超える試薬費は、すでに厳しい検査室の利益率を圧迫しており、包括的なプロファイル1件あたりの試薬費と分析費の平均コストは1,200米ドルですが、メディケアの支払額は検査1件あたり3,000米ドルです。リースや試薬レンタル契約は設備投資コストを相殺しますが、検査室を複数年にわたる契約に縛り付けてしまいます。検査件数の少ない医療機関は外部委託モデルに頼らざるを得ず、7~10日という結果が出るまでの期間を受け入れざるを得ず、その結果、治療開始が遅れてしまいます。このように、経済的な障壁が分散化を制限しており、特に資金調達が困難な新興市場において顕著です。

地域別分析

北米は2025年の収益の42.54%を占め、これは一人当たりの支出額の高さと、保険者による精密診断の急速な導入に牽引されたものです。2025年のCMS(米国医療保険サービスセンター)による料金表の引き下げにより、複雑度の低いゲノム検査の利益率が圧迫され、検査機関は償還率の高い腫瘍学パネルを優先するようになりました。カナダでは、抗うつ薬および抗凝固薬に対するファーマコゲノミクスの保険適用範囲が拡大され、プライマリケアにおける予防的な遺伝子型解析が広まりました。2024年には液体生検の検査件数が米国で200万件を超え、世界の検査件数の80%を占めました。

アジア太平洋地域は、集団ゲノミクスへの資金提供の増加を背景に、CAGR11.35%で成長すると予測されています。日本が2028年までに100万人のゲノム解読を目指す18億米ドルのイニシアチブにより、国内の機器販売が加速しています。中国では2024年にNGSがんパネルが70%の償還対象に加わったことで、一線都市において検査件数が3桁の伸びを示しています。インドの民間病院では自己負担の患者向けにNGS腫瘍プロファイリングを導入しており、一方、韓国のメーカーは東南アジア全域へPCRパネルの輸出を拡大しています。

欧州では、IVDR(体外診断用医療機器規則)に関連した製品の回収が相次ぎ、中小IVD企業の38%が撤退を検討しているため、供給が逼迫しています。サウジアラビアのヒトゲノム計画やUAEの新生児シーケンス計画により、中東はゲノムインフラ投資の新たなホットスポットとなりつつあります。ブラジルの公的医療サービスは2024年、結核およびHIVの薬剤耐性に関する分子検査に資金を提供し、予算の制約にもかかわらず導入を促進しました。したがって、地域ごとの勢いは、償還制度の安定性と国内の製造能力にかかっており、これらの要因が2031年までの市場シェアの変動を左右することになります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 迅速なポイントオブケア分子診断に対する需要の高まり

- コンパニオン診断と標的療法の統合

- シーケンスコストの低下と臨床用NGSの保険償還範囲の拡大

- 感染症管理のための多重症候群パネルの登場

- CLIA免除プラットフォームおよび小売クリニックを通じた検査の分散化

- 政府資金による全ゲノム解析およびパンデミック対策プログラム

- 市場抑制要因

- 高水準な分子プラットフォームにおける高い資本コストおよび運営コスト

- 複雑かつ変化し続ける規制の枠組み(EU IVDR、FDA LDT規則)

- 広範なゲノムプロファイリングおよび液体生検に関する償還の不確実性

- 熟練した分子検査室の人材不足

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 技術別

- PCR

- 次世代シーケンシング(NGS)

- イン・シチュ・ハイブリダイゼーション

- チップおよびマイクロアレイ

- 質量分析

- その他の技術

- 用途別

- 感染症

- 腫瘍学

- ファーマコゲノミクス

- 微生物学

- 遺伝性疾患スクリーニング

- ヒト白血球抗原(HLA)タイピング

- 血液スクリーニング

- 製品別

- 試薬・キット

- 機器・システム

- ソフトウェア・サービス

- 検体タイプ別

- 血液、血清、血漿

- 尿

- その他の検体タイプ(唾液、組織、スワブ)

- エンドユーザー別

- 病院

- 診断・検査機関

- 学術・研究機関

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- 10x Genomics

- Abbott Laboratories

- Agilent Technologies Inc.

- Becton, Dickinson And Company

- bioMerieux SA

- Bio-Rad Laboratories Inc.

- Danaher

- DiaSorin S.p.A.

- Exact Sciences Corporation

- F. Hoffmann-La Roche Ltd

- Guardant Health

- Hologic Inc.

- Illumina Inc.

- Labcorp

- Qiagen N.V.

- Seegene Inc.

- Siemens Healthineers AG

- Sysmex Corporation

- Thermo Fisher Scientific Inc.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 233 Pages

- 納期

- 2~3営業日