|

市場調査レポート

商品コード

1685793

北米の分子診断:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)North America Molecular Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の分子診断:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 96 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

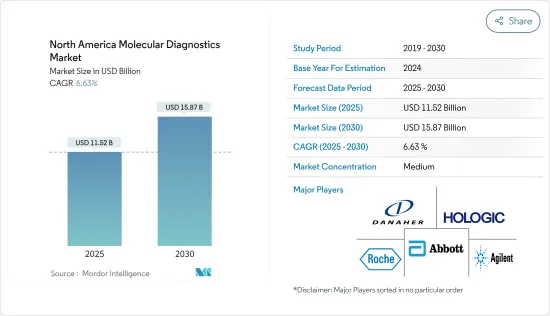

北米の分子診断市場規模は2025年に115億2,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは6.63%で、2030年には158億7,000万米ドルに達すると予測されます。

COVID-19は調査対象市場に大きな影響を与えました。ここ数年、COVID-19を検出するために分子診断が広く用いられています。感染症の迅速診断に対する需要の高まりに対応するため、さまざまな市場企業が革新的なポイントオブケア分子診断を発売しています。例えば、2022年7月、簡便な分子診断ソリューションの世界的プロバイダーであるBioGX社は、同社のpixlプラットフォーム上でCEマークを取得したポイントオブケア(POC)、3遺伝子マルチプレックスCOVID-19検査を発売しました。また、2021年4月には、サーモフィッシャーサイエンティフィック社が、高感度PCR検査を迅速にスケールアップするためのツールであるTaqPath COVID-19ハイスループット・コンボ・キットを用いたアンプリチュード・ソリューションについて、FDAから緊急使用承認(EUA)を取得しました。分子診断市場の成長は、COVID-19の症例数が減少しているため、現状では若干下支えされています。しかし、同地域では複数の用途で分子診断の需要が高く、分子診断の技術的進歩が進んでいることから、予測期間中は安定した成長が見込まれます。

同市場は主に、ポイントオブケア診断に対する需要の増加、薬理ゲノミクスの最近の進歩、細菌やウイルスの大規模な流行によって牽引されています。

分子診断検査は、正確かつ迅速で、さらに感染負荷を測定できなければならないです。米国における感染症やがん患者の増加により、従来の診断法から分子診断法へと移行する傾向が見られます。例えば、米国小児科学会が発表したデータによると、2022年3月、米国では100万人以上がB型肝炎に長期感染しており、赤ん坊の頃にB型肝炎に感染した人は、生涯のうちに90%の確率で肝臓がんなどの重篤な慢性疾患を発症するといいます。薬理ゲノミクスと相まって、分子検査によってこれらの疾患を早期に特定することが容易になっており、市場の成長を促進すると期待されています。

in-situハイブリダイゼーションは、保存された組織切片や細胞調製物から特定のmRNA配列を探し出し検出するために使用される、分子診断学分野で成長中の技術です。複数の市場参入企業による発売により、分子診断用製品の利用可能性が高まると予想されます。例えば、BIO-TECHNEは2021年4月、DNAコピー数や構造変異を発色検出するNOVEL DNASCOPE In Situ Hybridizationアッセイを発売しました。RNAscopeテクノロジーは先進的なin situハイブリダイゼーション(ISH)アッセイで、無傷の細胞や組織で直接、単一細胞の解像度で単一分子の遺伝子発現を可視化することができます。技術の進歩や製品の発売により、遺伝性疾患のスクリーニングやがんの検出など様々な用途でのin situハイブリダイゼーションの利用が促進されると期待されています。

市場参入企業による戦略的イニシアティブも市場の成長を後押ししています。例えば、2021年2月、Bio-Rad Laboratories Inc.は、マルチターゲットReliance SARS-CoV-2、FluA、FluB、RT-PCR、Reliance SARS-CoV-2 RT-PCRアッセイキットについてFDAからEUA承認を取得しました。マルチターゲットアッセイキットは、1回のマルチプレックス反応でSARS-CoV-2、インフルエンザA、インフルエンザBを同時に検出・鑑別します。このような発売も、予測期間中の市場成長に寄与すると予想されます。

したがって、感染症への高い負荷や、製品上市の増加につながる分子診断への需要の高まりといった前述の要因から、調査対象市場は分析期間中に成長を遂げると予測されます。しかし、厳しい規制の枠組みが市場の成長を阻害する可能性が高いです。

北米の分子診断市場の動向

オンコロジー分野が予測期間中に大きな市場シェアを占める見込み

腫瘍学は腫瘍やがんの診断と治療を扱う。同分野の高成長は、世界中で様々な種類のがんの負担が増加していることに起因しています。がんは罹患率および死亡率の主要原因の1つです。

米国がん協会(American Cancer Society)のがん統計2022によると、米国では2022年に191万8030人の新規がん患者が発生すると予測されています。乳がんは290,560人、白血病は60,650人、リンパ腫は89,010人が2022年に米国で新たに発症すると推定されています。また、2021年11月のカナダがん統計報告書によると、カナダ人の5人に2人が生涯にがんと診断される可能性があると推定されています。それによると、2021年には推定229,200人のカナダ人ががんと診断されると予測されています。このように、がんの負担の増加やがんの早期発見に対する人々の意識の高まりは、予測期間中に分子診断の利用を増加させると推定されます。

同地域の市場企業が採用する腫瘍学目的の分子診断製品拡大のための戦略的イニシアチブは、市場成長を促進すると予想されます。例えば、2022年11月、ロシュはELAHEREの対象となる卵巣がん患者を同定する初のIHCベースのコンパニオン診断薬として、VENTANA FOLR1(FOLR1-2.1)RxDxアッセイのFDA承認を取得しました。このような進歩や承認は、予測期間中の同分野の成長を後押しすると予想されます。

したがって、がんの有病率の高さ、がん検出における分子診断の利点、市場参入企業が採用する戦略的イニシアティブなどの要因により、予測期間中に同分野が拡大すると予想されます。

米国が予測期間中に大きな市場シェアを占める見込み

米国は、がんや感染症の罹患率の上昇、より良いヘルスケアインフラ、利用可能な技術に関する人々やヘルスケア業界利害関係者の認識、同地域における業界企業の強い存在感などの要因により、大きな市場シェアを占めると予想されます。

同国では、様々な疾患に関する調査研究に分子診断が使用されており、これが市場成長を促進すると期待されています。例えば、米国国立衛生研究所(NIH)の2022年最新情報によると、米国における遺伝子検査のための研究支出は2021年に2億1,200万米ドル、新興感染症のための研究支出は2021年に46億6,600万米ドルでした。このように、様々な疾病の研究に高い支出が行われているため、in-situハイブリダイゼーション、シークエンシング、PCRなどの分子診断が利用されており、予測期間中に同国の市場成長が拡大すると期待されています。

また、市場参入企業の戦略的な取り組みも同市場の成長を後押ししています。例えば、2022年6月、医療診断企業の1つであるVisby Medical社は1億3,500万米ドルの資金調達を行いました。この資金調達を通じて、Visby Medicalは生産能力を拡大し、提供する製品数を増やし、PCR診断を消費者の家庭に届けることを計画しました。

また2022年12月、米国の新興企業Alercell社が2023年1月にLENA Q51(R)を発売すると報告しました。これはDNAの塩基配列決定に基づく白血病診断検査で、白血病患者の最大51の遺伝子変異を検出します。同国における分子診断製品の技術革新と分子診断への資金提供による拡大は、予測期間中の同国市場の成長を促進すると予想されます。

そのため、HIV、肝炎、ヒトパピローマウイルス、複数の種類のがんなどの様々な感染症の診断におけるPCRの有用性の高さと、米国におけるこれらの疾患の有病率の高さが、予測期間中に米国における分子診断市場の成長を促進すると予想されます。

北米の分子診断産業の概要

北米の分子診断市場は、地域レベルおよび世界レベルの企業が多数存在するため、競争は中程度です。調査対象となった国際的な企業には、Abbott Laboratories、Agilent Technologies、Becton, Dickinson and Company、Danaher Corporation(Cepheid Inc.)、EXACT Sciences Corporation、F. Hoffmann-la Roche Ltd、Hologic Corporation、Illumina Inc.、Myriad Genetics Inc.、Qiagenが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ポイントオブケア診断薬に対する需要の増加

- ファーマコゲノミクスにおける最近の進歩

- 細菌性およびウイルス性の大規模流行

- 市場抑制要因

- 厳しい規制の枠組み

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 技術別

- インサイチュハイブリダイゼーション

- チップとマイクロアレイ

- 質量分析(MS)

- シーケンシング

- PCR

- その他の技術

- 用途別

- 感染症

- 腫瘍学

- ファーマコゲノミクス

- 微生物学

- 遺伝子疾患スクリーニング

- ヒト白血球抗原タイピング

- 血液スクリーニング

- 製品別

- 機器

- 試薬

- その他の製品

- エンドユーザー別

- 病院

- 検査機関

- その他のエンドユーザー

- 地域別

- 米国

- カナダ

- メキシコ

第6章 競合情勢

- 企業プロファイル

- Abbott Laboratories

- Agilent Technologies

- Becton, Dickinson and Company

- Danaher Corporation(Cepheid Inc.)

- EXACT Sciences Corporation

- F. Hoffmann-la Roche Ltd

- Hologic Corporation

- Illumina Inc.

- Myriad Genetics Inc.

- Qiagen

第7章 市場機会と今後の動向

The North America Molecular Diagnostics Market size is estimated at USD 11.52 billion in 2025, and is expected to reach USD 15.87 billion by 2030, at a CAGR of 6.63% during the forecast period (2025-2030).

COVID-19 had a profound impact on the studied market. Molecular diagnostics has been widely used in the past few years to detect COVID-19. Various market players were launching innovative point-of-care molecular diagnostics to meet the rising demand for rapid diagnostics of infectious diseases. For instance, in July 2022, BioGX, a global provider of easy molecular diagnostic solutions, launched a point-of-care (POC) CE-marked, three-gene multiplex COVID-19 test on its pixl platform. Also, in April 2021, Thermo Fisher Scientific Inc. was granted emergency use authorization (EUA) from the FDA for its amplitude solution with the TaqPath COVID-19 high-throughput combo kit, a tool for rapidly scaling high-sensitivity PCR testing. The growth of the molecular diagnostics market is slightly subsidized currently due to the decrease in the number of COVID -19 cases. However, the studied market is expected to report stable growth over the forecast period owing to the high demand for molecular diagnostics in multiple applications and technological advancements in molecular diagnostic products in the region.

The market is mainly driven by increasing demand for point-of-care diagnostics, recent advancements in pharmacogenomics, and large outbreaks of bacterial and viral epidemics.

The molecular diagnostics test must be precise, rapid, and also be able to measure the infectious burden. The increase in infectious diseases and cancer cases in the United States has led to trends shifting from traditional diagnostic methods to molecular diagnostics. For instance, according to data published by the American Academy of Pediatrics, in March 2022, more than 1 million people in the United States have long-term hepatitis B infections, and people who are infected with hepatitis B as a baby have a 90% chance of developing severe, chronic conditions like liver cancer in their lifetime. The identification of these diseases at an early stage has become easy using molecular tests, coupled with pharmacogenomics, which is expected to fuel market growth.

In situ hybridization is a growing technology in the molecular diagnostics branch that is used to locate and detect specific mRNA sequences in preserved tissue sections or cell preparations. The launches by several market players are expected to boost the availability of products for molecular diagnostics. For instance, in April 2021, BIO-TECHNE launched NOVEL DNASCOPE In Situ Hybridization assays for chromogenic detection of DNA copy numbers and structural variations. The RNAscope technology is an advanced in situ hybridization (ISH) assay that enables visualization of single-molecule gene expression with single-cell resolution directly in intact cells and tissues. The advancements in technology and product launches are expected to propel the usage of in situ hybridization for various applications such as genetic disease screening and cancer detection.

The strategic initiatives taken by the market players are also propelling the growth of the market. For instance, in February 2021, Bio-Rad Laboratories Inc. received EUA approval from the FDA for multi-target Reliance SARS-CoV-2, FluA, FluB, RT-PCR, and Reliance SARS-CoV-2 RT-PCR assay kits. The multi-target assay kit simultaneously detects and differentiates SARS-CoV-2, influenza A, and influenza B in a single multiplex reaction. Such launches are also expected to contribute to the growth of the market during the forecast period.

Therefore, owing to the aforementioned factors such as the high burden of infectious diseases, and the rising demand for molecular diagnostics leading to increasing product launches, the studied market is anticipated to witness growth over the analysis period. However, the stringent regulatory framework is likely to impede the market growth.

North American Molecular Diagnostics Market Trends

Oncology Segment Expected to Hold a Significant Market Share Over The Forecast Year

Oncology deals with the diagnosis and treatment of tumors and cancers. The segment's high growth is attributed to the rising burden of various types of cancer worldwide. Cancer is one of the leading causes of morbidity and mortality.

According to the American Cancer Society, cancer statistics 2022, 1,918,030 new cancer cases are predicted to occur in the United States in 2022. Breast cancer is estimated to be 290,560 new cases, leukemia with 60,650 new cases, and lymphoma with 89,010 new cases in the United States in 2022. Also, according to the Canadian Cancer Statistics November 2021 report, an estimated 2 in 5 Canadians were likely to be diagnosed with cancer in their lifetime. It stated that an estimated 229,200 Canadians was predicted to be diagnosed with cancer in 2021. Thus, the increasing burden of cancer and rising awareness among people for early cancer detection is estimated to increase the usage of molecular diagnostics over the forecast period.

The strategic initiatives adopted by market players in the region to expand molecular diagnostics products for oncology purposes are expected to fuel market growth. For instance, in November 2022, Roche received FDA approval for VENTANA FOLR1 (FOLR1-2.1) RxDx assay as the first IHC-based companion diagnostic to identify ovarian cancer patients eligible for ELAHERE. Such advancements and approvals are expected to boost segment growth during the forecast period.

Therefore, owing to the factors such as the high prevalence of cancer, the benefits of molecular diagnostics in cancer detection, and strategic initiatives adopted by market players are expected to augment the segment during the forecast period.

United States is Expected to Hold a Significant Market Share Over The Forecast Period

The United States is expected to hold a significant market share owing to factors such as the rising incidence of cancer and infectious diseases, better healthcare infrastructure, awareness among people and healthcare industry stakeholders about available technologies, and the strong presence of industry players in the region.

The spending on research studies in the country on various diseases involves the use of molecular diagnostics which is expected to propel market growth. For instance, according to the National Institutes of Health (NIH) 2022 update, research expenditure in the United States for genetic testing was USD 212 million in 2021 and USD 4,666 million for emerging infectious diseases in 2021. Thus, the high spending on the research of various diseases uses molecular diagnostics such as in-situ hybridization, sequencing, and PCR which is expected to augment the market growth in the country during the forecast period.

The strategic initiatives the market players take also propel the market segment's growth. For instance, in June 2022, one of the medical diagnostic companies Visby Medical raised funding of USD 135 million. Through this funding, Visby Medical planned to scale production capacity, increase the number of products it offers and bring PCR diagnostics to consumers' homes.

Also, in December 2022, Alercell, a United States-based start-up reported launching LENA Q51(R) in January 2023. It is a leukemia diagnostic test based on sequencing DNA that will detect up to 51 gene mutations in leukemia patients. The innovation in molecular diagnostics products and expansions through initiating funding for molecular diagnostics in the country is expected to propel the market growth in the country during the forecast period.

Therefore, the high utility of PCR in recent times for the diagnosis of various infectious diseases such as HIV, hepatitis, human papillomavirus, and multiple types of cancer along with the high prevalence of such diseases in the country is expected to propel the molecular diagnostics market growth in the United States during the forecast period.

North American Molecular Diagnostics Industry Overview

The North American molecular diagnostics market is moderately competitive due to the region's many local and global level companies. The international players in the market studied include Abbott Laboratories, Agilent Technologies, Becton, Dickinson and Company, Danaher Corporation (Cepheid Inc.), EXACT Sciences Corporation, F. Hoffmann-la Roche Ltd, Hologic Corporation, Illumina Inc., Myriad Genetics Inc., and Qiagen.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Point-of-care Diagnostics

- 4.2.2 Recent Advancements in Pharmacogenomics

- 4.2.3 Large Outbreaks of Bacterial and Viral Epidemics

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Framework

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Technology

- 5.1.1 In-situ Hybridization

- 5.1.2 Chips and Microarrays

- 5.1.3 Mass Spectrometry (MS)

- 5.1.4 Sequencing

- 5.1.5 PCR

- 5.1.6 Other Technologies

- 5.2 By Application

- 5.2.1 Infectious Disease

- 5.2.2 Oncology

- 5.2.3 Pharmacogenomics

- 5.2.4 Microbiology

- 5.2.5 Genetic Disease Screening

- 5.2.6 Human Leukocyte Antigen Typing

- 5.2.7 Blood Screening

- 5.3 By Product

- 5.3.1 Instrument

- 5.3.2 Reagent

- 5.3.3 Other Products

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Laboratories

- 5.4.3 Other End Users

- 5.5 Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Agilent Technologies

- 6.1.3 Becton, Dickinson and Company

- 6.1.4 Danaher Corporation (Cepheid Inc.)

- 6.1.5 EXACT Sciences Corporation

- 6.1.6 F. Hoffmann-la Roche Ltd

- 6.1.7 Hologic Corporation

- 6.1.8 Illumina Inc.

- 6.1.9 Myriad Genetics Inc.

- 6.1.10 Qiagen