グリーンデータセンター:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Green Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 2066466

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

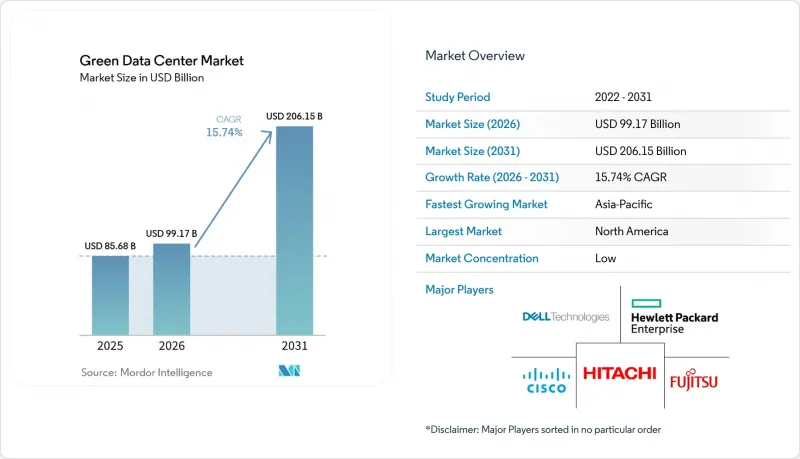

Mordor Intelligenceによると、グリーンデータセンターの市場規模は2025年に856億8,000万米ドルと評価され、2026年の991億7,000万米ドルから2031年までに2,061億5,000万米ドルに達すると予測されており、予測期間(2026年~2031年)におけるCAGRは15.74%となる見込みです。

本レポートは、構成要素(サービス、ソリューション)、データセンターの種類(コロケーションプロバイダー、ハイパースケーラー/クラウドサービスプロバイダー、エンタープライズ、エッジ)、ティアの種類(Tier 1および2、Tier 3、Tier 4)、業種(医療、BFSI、政府機関など)、および地域ごとに分類されています。市場予測は金額(米ドル)ベースで提示されています。

世界のグリーンデータセンター市場の動向と洞察

ハイパースケールクラウドの拡張が100%再生可能エネルギーへ移行

グリーンデータセンター市場は、現在、自社の直接消費量をはるかに上回る規模の風力、太陽光、およびバッテリーハイブリッドプロジェクトを契約しているハイパースケール事業者から恩恵を受けています。アマゾンは2024年に全社で100%再生可能エネルギーを達成し、マイクロソフトは2030年までにカーボンネガティブな事業運営を公約しており、グーグルは余剰の再生可能電力を、廃熱をさらに収益化する都市の地域暖房プロジェクトに活用しています。これらの戦略により、事業者は価格の安定した電力を確保し、再生可能エネルギークレジットの販売を通じてヘッジ収益を生み出し、コロケーション施設の所有者がその後従う調達テンプレートを確立することが可能になります。

OECD諸国におけるPUE 1.3以下への規制推進

EUの新たな指令や改訂された米国のエネルギー基準により、グリーンデータセンター市場において、PUE、水使用効率、および炭素強度の透明性のある報告が義務付けられています。ドイツのエネルギー効率法では冷却効率の開示が義務付けられている一方、AWSは2024年に世界のPUE 1.15を報告しており、AIベースのワークロードスケジューリングと液体冷却を組み合わせることで、規制遵守が可能であることを実証しています。早期に改修を行う事業者は、ファンの消費電力の低減や機械的冗長性の削減によるコスト削減効果を享受でき、コロケーション契約の更新時に競合力を高めることができます。規制違反に対する罰則は会計年度ごとに強化されており、エネルギー効率の高い機器の導入に向けた短期的な動きが加速しています。

ブラウンフィールド改修と比較した初期設備投資(CAPEX)の割増率(30~40%)

高性能断熱材、液浸冷却ラックに対応した構造化ケーブル、およびオンサイト太陽光発電・蓄電システムは、従来のシェルと比較して建設コストを最大40%押し上げます。低炭素コンクリートや相変化断熱壁などの建設資材は、2025年においても供給制約が続いており、グリーンデータセンター市場の展開にスケジュール上のリスクをもたらしています。小規模な事業者は、完全なグリーンビルドではなく、段階的な効率化改修に切り替えることが多く、部品価格が正常化するまで、全体的な容量の増加が鈍化しています。

セグメント分析

ソリューション部門は2025年の売上高の62.54%を占め、資本集約度においてグリーンデータセンター市場の規模を牽引しています。事業者は、効率化要件を満たすために、電源調整装置、熱回収型チラー、AIを活用したDCIMソフトウェアを優先的に導入しており、一方、液体からチップへの冷却製品ラインでは、出荷台数が2桁の伸びを記録しました。サービス部門は、絶対値では小さいもの、施設所有者がライフサイクルにわたるサステナビリティ監査、AIを活用したワークロードオーケストレーション、ESG報告のために専門家を起用するにつれ、CAGR15.38%が見込まれています。

効率98%のUPSモジュールやスマートグリッドインターフェースを含む電源システムのアップグレードにより、耐障害性が強化され、運用コストが削減されました。冷却ソリューションは、高床式エアハンドラーから、温水ループと組み合わせたリアドア式熱交換器へと移行しました。サービス面では、統合パートナー各社が、炭素排出量算定ダッシュボードや再生可能エネルギー証書(REC)取引プラットフォームをパッケージ化しています。こうしたサステナビリティ管理の専門化は、グリーンデータセンター業界における構造的な向上を示しています。

企業のアウトソーシング戦略が継続する中、コロケーション企業は2025年の支出の36.62%を占めましたが、ハイパースケーラーはCAGR16.21%で他を凌駕し、自社所有容量におけるグリーンデータセンター市場全体の規模を拡大させました。彼らが締結した10億米ドル規模の再生可能エネルギーPPAや、カスタム設計の液浸冷却システムは、技術導入の動向を牽引し、その影響は小売向けコロケーションスイートにも波及しています。

エンタープライズ事業者は堅調な推移を維持し、取締役会レベルで設定された排出量目標を達成するため、封じ込めポッドやモジュール式バッテリーストレージを用いて既存施設(ブラウンフィールド)を刷新しました。エッジマイクロ施設は、まだ発展途上ではありますが、5G基地局の処理をサポートするために、パッシブ冷却や太陽光発電によるUPSを採用しました。クラウド大手企業の調達力により、部品サプライヤーのコスト曲線は低下し続けており、間接的に第2層のプロバイダーにとっての参入障壁が低くなっています。

地域別分析

北米は2025年に売上高の26.14%を占め、信頼性の高い再生可能エネルギー発電、手厚い税制優遇措置、およびバージニア州、オレゴン州、テキサス州周辺に集中するハイパースケール事業に支えられています。州の規制当局が詳細なESG情報開示を義務付けていることから、AIベースのエネルギー管理が早期に導入され、この地域のグリーンデータセンター市場は技術的成熟度において先行しています。

アジア太平洋地域は、日本のカーボンニュートラル・データセンター構想、インドのデータ主権政策、オーストラリアの再生可能エネルギーゾーンが新規建設を後押しし、2031年までの年間平均成長率(CAGR)が22.86%に達すると予測されています。東南アジアにおける送電網のボトルネックは、専用線による太陽光発電と蓄電池の組み合わせ案件を促進しており、送電網のアップグレードが実現すれば、同地域は飛躍的な効率向上を実現する態勢が整っています。

欧州は、「気候中立データセンター事業者協定(Climate Neutral Data Centre Operator Pact)」などの統一された政策を通じて、中心的な役割を維持しています。北欧のデータセンターキャンパスでは、自然冷却と豊富な水力発電を活用し、熱を都市熱供給網に供給することで、実効PUEを1.1まで低減しています。南欧では太陽光発電と他の電源を組み合わせたハイブリッドプロジェクトが加速しており、ドイツの企業向け電力購入契約(PPA)がフランクフルトにおけるマルチクラウドの導入を後押ししています。全体として、地域的な政策の一貫性が、グリーンデータセンター市場における投資の勢いを支えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ハイパースケール・クラウドの拡張が100%再生可能エネルギーへ移行

- OECD諸国におけるPUE 1.3以下を目指す規制の推進

- 10 MWを超えるキャンパスにおけるオンサイト水素燃料電池の実証事業(2025年~2028年)

- 地域熱供給ネットワークにおけるAIワークロードの廃熱再利用

- 地域ベースの再生可能エネルギークレジットの収益化

- サーバーOEM各社による提携から生まれる液体冷却ターンキー・エコシステム

- 市場抑制要因

- ブラウンフィールド改修と比較した初期設備投資(CAPEX)の割増分(30~40%)

- 新興国における再生可能エネルギー送電網の容量の制限

- 都市中心部周辺における再生水利用権の不足

- 低GWP冷媒(R-718、R-1234yf)のサプライチェーンの変動性

- サプライチェーン分析

- 規制情勢

- 技術展望

- ポーターのファイブフォース分析

- 市場に対するマクロ経済的要因の評価

第5章 市場規模と成長予測

- コンポーネント別

- サービス別

- システムインテグレーション

- モニタリングサービス

- プロフェッショナルサービス

- その他のサービス

- ソリューション別

- Power

- 冷却

- サーバー

- ネットワーク機器

- 管理ソフトウェア

- その他のソリューション

- サービス別

- データセンタータイプ別

- コロケーションプロバイダー

- ハイパースケーラー/クラウドサービスプロバイダー

- エンタープライズおよびエッジ

- ティア別

- Tier 1および2

- ティア3

- ティア4

- 産業分野別

- ヘルスケア

- BFSI

- 政府

- 通信・IT

- 製造業

- メディア・エンターテイメント

- その他の業種

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他の南米諸国

- 欧州

- ドイツ

- 英国

- フランス

- オランダ

- その他の欧州諸国

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア・ニュージーランド

- その他のアジア太平洋諸国

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他の中東諸国

- アフリカ

- 南アフリカ

- ナイジェリア

- その他のアフリカ諸国

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Fujitsu Ltd

- Cisco Systems Inc.

- Hewlett Packard Enterprise Co.

- Dell Technologies Inc.

- Hitachi Ltd

- Schneider Electric SE

- IBM Corporation

- Eaton Corporation

- Vertiv Holdings Co

- Equinix Inc.

- Digital Realty Trust Inc.

- NTT Communications Corp.

- Amazon Web Services Inc.

- Microsoft Corp.

- Google LLC

- Huawei Technologies Co. Ltd

- Rittal GmbH and Co. KG

- Siemens AG

- Vapor IO Inc.

- Iron Mountain Inc.

- QTS Realty Trust Inc.

- Keppel Data Centres

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日