|

市場調査レポート

商品コード

1852165

乳タンパク質:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Dairy Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 乳タンパク質:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年09月02日

発行: Mordor Intelligence

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

概要

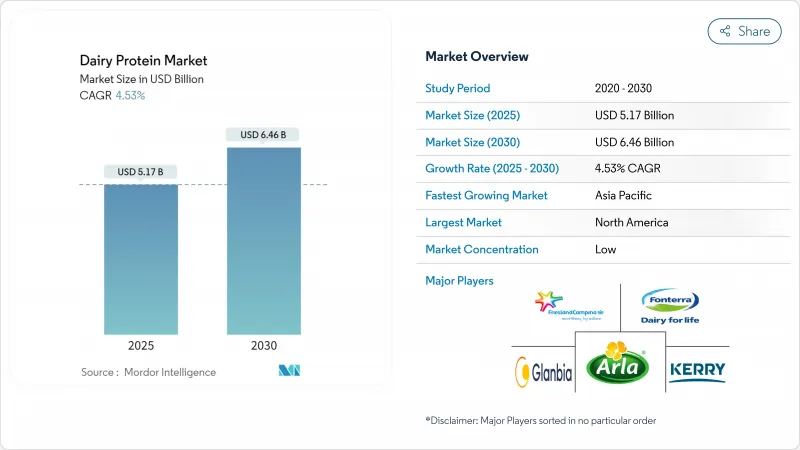

乳製品タンパク質の市場規模は、2025年に51億7,000万米ドルと評価され、2030年には64億6,000万米ドルに達し、CAGR 4.53%で成長すると予測されています。

市場成長の主因は、体重管理と筋肉開拓をサポートする高タンパク質食に対する消費者の嗜好の高まり、総合的な健康効果を目的とした機能性栄養食品の採用の高まり、様々な消費者層におけるRTD(Ready-to-Drink)飲料への用途の拡大です。膜ろ過と精密発酵技術の進歩により、生産収率が改善され、タンパク質の品質が向上し、飲食品処方における新たな用途が可能になりました。クリーンラベル製品に対する消費者の需要は、特に健康志向の消費者や食生活に嗜好性を持つ消費者の間で、オーガニックや最小限の加工を施した選択肢への関心を高めています。乳価の変動やサプライチェーンの課題にもかかわらず、メーカーは世界的な需要の増加に対応するため、生産能力の拡大を続けています。大手協同組合が規模の経済を達成するために合併によって統合する一方で、原料メーカーはプレミアム市場セグメントを獲得するためにラクトフェリンや加水分解ホエイ分離物のような特殊製品に注力するため、市場の競争は激化しています。こうした動きは、アスリートやフィットネス愛好家向けのスポーツ栄養、乳児用調製粉乳メーカー向けの早期栄養、医療食品メーカー向けの臨床栄養の各分野に新たな機会を生み出します。

世界の乳タンパク質市場の動向と洞察

高タンパク食への需要の高まり

IFIC Food and Health Survey 2024によると、消費者の71%がタンパク質の摂取量を積極的にモニターしており、2023年の69%から増加しています。若年成人、中年個人、高齢者を含むすべての人口統計グループにわたって、消費者の半数近くが夕方にタンパク質の消費量を増やしています。この動向は、特に健康志向の高い25~45歳の消費者の間で強いです。ミレニアル世代とジェネレーションZがプロテイン強化製品の発売増加を牽引し、従来のスポーツ栄養消費者だけでなく、日常の栄養補助食品にまで市場を拡大しています。需要は朝食用、飲料用、食事代替用など多岐にわたる。ロイシン、イソロイシン、バリンなどの必須アミノ酸を含む完全なアミノ酸プロファイルのため、植物由来の代替品に比べ、乳製品タンパク質はプレミアム価格を維持しています。タンパク質を強化したスナック、デザート、飲食品、コンビニエンス・フードの利用が増加していることは、複数の食品カテゴリーでタンパク質強化が広く市場に受け入れられていることを示しています。この多様化には、タンパク質強化ヨーグルト、チーズスナック、ミルクベースの飲料、代替アイスクリームなどが含まれ、2030年までの乳製品タンパク質市場の成長を支えています。

スポーツ栄養と機能性食品の成長

乳製品タンパク質は、主にホエイ(乳清)の迅速な吸収とカゼインの緩やかな放出特性により、スポーツ栄養において強い存在感を維持しています。消費者層は従来のアスリートだけでなく、認知機能強化の効果を求める女性や若年層にまで拡大しており、そのためプロテインサプリメントや機能性飲料にシチコリンが配合されるなどの技術革新が起きています。レクリエーション活動、競合スポーツ、フィットネストレーニングを含むスポーツ参加の増加が市場拡大に寄与しています。世界保健機関(WHO)の2024年報告書によると、世界人口の69%が定期的な運動や身体活動を通じて活動的なライフスタイルを維持している一方、31%は身体的に不活発なままです。このことは、アスリートやボディビルダーが筋肉の回復と維持のためにカゼイン・プロテインを好み続けているアクティブ・ライフスタイル・セグメントに大きな成長機会をもたらします。カリウム、カルシウム、マグネシウムのような必須ミネラルを含む乳製品プロテインの天然電解質含量は、パフォーマンス上の利点を提供するため、機能的水分補給分野は特に有望です。栄養の個別化の動向は、様々な食事のニーズや制限に対応しながら、持久力強化、筋肉増強、回復の最適化など、特定のパフォーマンス目標をターゲットとした特殊な乳タンパク質処方の機会を生み出します。

乳糖不耐症と乳製品アレルギー

乳糖不耐症は世界人口のかなりの部分が罹患しており、特定のアジア地域では有病率が90%を超えているため、従来の乳製品タンパク質の使用が制限されています。この症状は消化能力と栄養吸収を制限し、プロテイン飲料市場における消費者の選択肢を狭めています。しかし、無乳糖加工とタンパク質分離技術の進歩により、こうした課題は克服されつつあります。最新のろ過システムと酵素処理により、メーカーは栄養価を保持したまま乳糖フリーの乳製品を製造できるようになりました。植物由来の表示に関するFDAのガイドラインは、栄養価の明確な区別を定め、高い生物学的利用能を示す乳製品の選択肢を強調しています。Imagindairy社のような企業は、乳糖とアレルゲン性の両方の問題を解消する発酵ベースの乳製品タンパク質を開発しています。これらの精密発酵法は、乳糖を含まない乳製品と同じタンパク質を生産し、これまで市場拡大を制限してきた不耐症とアレルギー反応の懸念の両方に対処します。これらの加工技術の導入により、乳タンパク質の機能的・栄養的特性を維持しながら、製品の入手しやすさが向上しています。

セグメント分析

2024年の乳製品タンパク質市場では、ホエイタンパクが49.26%の圧倒的シェアを占めています。この地位は、スポーツ栄養パウダー、レディ・トゥ・ドリンク・プロテイン・シェイク、ベーカリー製品に幅広く使用されていることに起因しています。このタンパク質の完全なアミノ酸プロファイル、迅速な吸収率、機能的特性により、これらの用途で不可欠なものとなっています。カゼインとカゼイン酸塩は、徐放性栄養製品と医療用栄養製剤において安定した需要を維持しています。加水分解タンパク質は、消化性が改善されアレルゲン性が低いため、市場で受け入れられつつあります。

乳タンパク質分野は、加工技術革新、特に本来のミセル構造を維持する限外ろ過技術に支えられ、2030年までCAGR 5.52%で成長すると予想されます。これらの開発により、超高温(UHT)飲料や高タンパク質ヨーグルトの配合におけるタンパク質の機能性が向上します。精密発酵ホエイタンパク質の商業生産は、全体的な原料需要を強化すると同時に、潜在的な市場シフトを示唆しています。技術の進歩は、特殊化された原料による市場のプレミアム化を可能にし、メーカーは乳児用調製粉乳、臨床栄養製品、タンパク質強化アイスクリーム用の的を絞ったソリューションの創出を可能にします。原料メーカーはサプライチェーンのトレーサビリティと持続可能性認証を優先し、製品差別化の機会を創出し、市場価値の成長を支えています。

従来のタンパク質は、確立されたサプライチェーン、効率的な加工方法、規模の経済によって支えられており、2024年の乳製品タンパク質市場の92.5%を占める。人工添加物、抗生物質の使用、集約的農法に対する消費者の関心の高まりが、オーガニック乳タンパク質需要をCAGR 8%で牽引しています。クリーン・ラベル・チーズ・セグメントは、商品棚での存在感を高め、消費者に受け入れられることで、市場の商業的可能性を示しています。オーガニック生産には、より高い飼料コスト、厳格な認証プロセス、特殊な取り扱い要件が伴うが、メーカーはプレミアム価格戦略と製品品質に対する消費者の信頼強化を通じて、これらの経費を相殺します。

オーガニック・セグメントは、消費者が合成添加物や保存料を含まない製品を求める、厳しい品質基準と天然成分を優先する乳児用調製粉乳や、スポーツ栄養剤で大きな伸びを示しています。主要市場における明確な規制と、有機酪農インフラへの持続的な投資により、認証牛乳の供給力が高まっています。先進国以外では、認証の課題とインフラの格差により生産能力は依然限られているが、有機乳業メーカーは、的を絞ったブランド開拓、透明性の高い調達慣行、eコマース流通チャネルの拡大を通じて、市場での地位を確立しています。

地域分析

北米は、確立されたスポーツ栄養エコシステムとタンパク質の品質に関する包括的な小売教育プログラムに支えられて、2024年の世界の乳製品タンパク質市場で33%の圧倒的シェアを維持します。この地域の市場の強さは、消費者の幅広い認知、高度な流通網、継続的な製品革新に起因します。2024年8月、ケンビューはマイクロペプチド技術を搭載したニュートロジーナ(R)コラーゲンバンク(TM)を発売して製品ポートフォリオを拡大し、予防的スキンケアソリューションを求めるZ世代消費者をターゲットにプレエイジングカテゴリーに参入しました。ヨーグルトの摂取と2型糖尿病リスクの低減を結びつけるFDAの適格健康強調表示は、市場の地位をさらに強化し、高級乳製品の開発を促しています。

アジア太平洋は、都市化の進展、食生活の嗜好の変化、高タンパク食品とフレーバー・チーズの採用拡大により、2030年までのCAGRが8.5%と、著しい成長の可能性を示しています。中間層の拡大、可処分所得の増加、eコマース・プラットフォームの普及が、強力な市場機会を生み出しています。この地域の成長は、コールドチェーンインフラの改善とタンパク質豊富な食生活に対する意識の高まりによってさらに支えられています。

USDAのデータによると、2025年の生乳生産量は1億4,940万トンに達すると予測されており、厳しい環境規制や疾病関連の課題が続いています。2025年4月に行われた190億ユーロ規模のArlaとDMKの合併は、業界の統合を意味し、調達能力と研究施設を統合して経営効率を高める。欧州の消費者は持続可能性と製品の品質を強く重視しており、この地域の環境責任へのコミットメントを反映して、精密発酵と低炭素乳タンパク質への需要が高まっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 高タンパク食への需要の高まり

- スポーツ栄養と機能性食品の成長

- 乳幼児と高齢者栄養における用途の増加

- RTD(レディー・トゥ・ドリンク)飲料の高タンパク人気と用途の拡大

- 乳製品加工における技術革新

- クリーンラベルと天然蛋白源への需要の高まり

- 市場抑制要因

- 乳糖不耐症と乳製品アレルギー

- 植物性プロテインの需要の高まり

- 生乳の価格変動

- 環境と持続可能性への懸念

- サプライチェーン分析

- 規制とテクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額および数量)

- 成分別

- 牛乳

- 分離

- 濃縮

- 加水分解

- ホエー

- 濃縮

- 分離

- 加水分解

- カゼインとカゼイネート

- 牛乳

- 由来別

- 従来型

- オーガニック

- 原料別

- 牛

- バッファロー

- ヤギとヒツジ

- 用途別

- 食品および飲料

- ベーカリー・菓子

- 乳製品・デザート

- 飲料

- スポーツ・パフォーマンス栄養

- 乳児および幼児期の栄養

- 高齢者栄養と医療栄養

- その他の用途

- 食品および飲料

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリアおよびニュージーランド

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Fonterra Co-operative Group Ltd

- Royal FrieslandCampina N.V.

- Arla Foods amba

- Glanbia PLC

- Kerry Group PLC

- Groupe Lactalis S.A.

- Saputo Inc.

- Agropur Co-operative

- Hilmar Cheese Company, Inc.

- Leprino Foods Company

- DMK Group

- Carbery Group Limited

- Morinaga Milk Industry Co., Ltd

- Prolactal GmbH

- Actus Nutrition

- Ingredia SA

- Tatua Co-operative Dairy Co. Ltd.

- Theo Muller Group

- Hoogwegt International B.V.

- Savencia Fromage & Dairy