|

市場調査レポート

商品コード

1686529

オフショアAUV・ROV-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Offshore AUV And ROV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| オフショアAUV・ROV-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

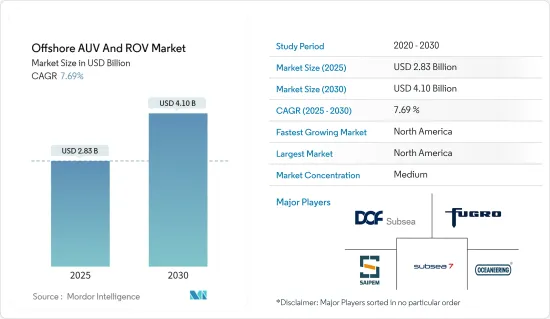

オフショアAUV・ROV市場規模は2025年に28億3,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは7.69%で、2030年には41億米ドルに達すると予測されます。

主なハイライト

- 中期的には、オフショア石油・ガス生産活動の増加、オフショア風力発電産業の成長、石油・ガス廃止活動の増加などの要因が、予測期間中のオフショアAUV・ROV市場を牽引すると予想されます。

- 一方で、気候変動への注力を強めることを計画している国や、将来的に海洋探査活動を禁止することを計画している国は、市場の成長を抑制すると予想されます。

- とはいえ、技術革新と技術進歩により、石油・ガス、洋上風力、調査などの産業におけるオフショア活動でのAUV・ROVの利用が増加すると予想されます。AUV・ROVの技術的進歩は、長期的には企業にかなりの機会を提供すると予想されます。

- 北米は大きな成長が見込まれ、需要の大部分は米国やメキシコなどの国々からもたらされます。

オフショアAUV・ROVの市場動向

石油・ガスセグメントが市場を独占

- AUV・ROVは、海底インフラ建設、モニタリング、調査ミッションのための位置決めとガイダンスに使用されます。オフショア石油・ガスエンジニアリングにおける水中探査機の用途には、ガイド掘削作業、海底観測、定点サンプリング、ジャケット設置に関わる補助作業、石油・ガスパイプラインの敷設、オフショア施設のメンテナンスなどが含まれます。

- 世界の主要経済国が依然として石油ベースの製品に大きく依存しているため、石油・ガスへの依存度は高まっています。石油・ガス産業は、国際政治・経済において絶大な影響力を持っています。

- 2022年、世界の石油生産量は前年比4.18%増の9,384万8,000バレル/日を記録しました。世界人口の増加は、一次エネルギー消費の増加に反映され、2011年の520.90エクサジュールから、2022年には604.04エクサジュールとなりました。

- 世界の炭化水素の潜在埋蔵量の多くは、海底に眠っています。炭化水素産業は、石油・ガスの発見とその生産を成功させるために、海上の条件に適した技術を開発しました。

- 石油・ガス掘削リグは、水深2マイルで操業することもあります。こうした深海の油井やパイプライン・システムの多くは、設置、検査、修理、メンテナンスを無人水中ビークルに頼っています。

- 最近、いくつかの国が石油・ガスの海洋部門に積極的に取り組んでおり、海底油田からの増産に向けた投資を目の当たりにしているため、AUVやROVの活躍の場が生まれています。

- 2022年5月、ShellとPetrobrasはSaipemと契約し、2つのエネルギー会社が運営するブラジル沖合の2つの超深海油田の点検キャンペーンを含む2つのパイロットプロジェクトにFlatFish海底ドローンを使用しました。

- さらに2022年8月、インドの石油・天然ガス公社は、エクソンモービル社との間で、同国の東海岸と西海岸における深海探査に関する基本合意書(HoA)を締結しました。両社は、東部沖合ではクリシュナ・ゴダヴァリ海盆とカウヴェリー海盆を、西部沖合ではクッチ・ムンバイ海域を重点的に探査する予定です。

- したがって、上記の点から、オフショアAUV・ROVの需要は、予測期間中に石油・ガス分野で大きく成長すると予想されます。

北米が大きな成長を遂げる見込み

- 北米地域は、世界的に最も発達したオフショア石油・ガス産業の1つであり、主な重点地域はメキシコ湾とアラスカ沖地域の膨大な埋蔵量です。掘削深度が年々深まるにつれ、技術的に回収可能な埋蔵量も大幅に増加し、投資が活発化しています。

- 工業化の進展と研究開発への投資により、北米は予測期間中、オフショアAUV・ROVの最大市場の1つになると予想されます。

- 米国は防衛分野とAUV・ROVの研究開発に多額の投資を行っているため、石油・ガス、海運、再生可能エネルギーのような他の関連オフショア分野は、調査された市場の技術進歩から多大な利益を得ています。このため、この地域はAUV・ROV技術の最前線にあります。同地域のAUV・ROVメーカーは、その製品を世界中に輸出しています。

- この地域は、世界的に最も発達した海洋石油・ガス産業の1つであり、主な重点地域はメキシコ湾とアラスカ沖地域の膨大な埋蔵量です。掘削深度が年々深まるにつれて、技術的に回収可能な埋蔵量が大幅に増加し、それが投資の拡大を引き寄せています。

- 米国が石油・ガス生産能力の拡大に多額の投資を行ったため、メキシコ湾はAUV・ROVの需要にとって世界のホットスポットとなりました。2022年現在、メキシコ湾地域は米国のオフショアと炭化水素総生産量のそれぞれ97%と15%を占めています。同地域は、オフショア・リグの展開密度が世界で最も高い地域の1つであり、生産・掘削プラットフォーム、海洋船舶、パイプライン・ネットワークなど、その他の石油・ガス・インフラで構成されています。

- ROVとAUVの技術がますます手頃な価格になってきているため、米国の石油・ガス生産者は、海底資産や海面のデータを取得し、定期的な保守作業を実施するために、ROVとAUVサービスに投資しています。ROVやAUVは、潜水作業員に比べて初期費用は高いもの、同じ量の作業を完了するのに必要な時間が短いため、プロジェクト全体のOPEXを削減することができます。

- このため、大手石油・ガス会社はメキシコ湾でROVとAUVサービスの複数契約を日常的に結んでいます。2022年9月、DOF Subsea USAは、主要地域の石油・ガス事業者からメキシコ湾で複数の契約を受注したと発表しました。DOF Subseaが運航するジョーンズ法に準拠した船舶は、1年間の期間中に約180日間利用され、複数の現場で点検、保守、修理、軽作業、試運転支援など、さまざまな活動を行う。

- メキシコは伝統的に炭化水素産業が盛んでした。しかし、メキシコのオフショア部門における平均掘削深度は、米国に比べて相対的に低いです。このため、メキシコの石油・ガス事業者は、ダイバー・アシストからROVやAUVなどのダイバーレス・サービスに切り替える金銭的インセンティブが少ないです。

- しかし、メキシコ政府が炭化水素部門を活性化し、国内の炭化水素生産を促進しようとしているため、同国の石油・ガス業界は、特に国営石油・ガス公社PEMEXから大規模な投資を受けると予想されます。2022年3月、PEMEXのE&P部門であるPEPは、ベースライン・シナリオとインクリメンタル・シナリオに基づく1億700万~4億7,800万米ドルの投資で、浅海のウチュキル鉱区の探査承認を得たと発表しました。

- 同様にメキシコは、今後数年間に2つの新しい海洋鉱区の開発に12億米ドルを投資することを約束しました。オフショア分野へのこのような大規模な投資は、予測期間中、メキシコのオフショアAUV・ROV市場を牽引すると予想されます。

- したがって、上記の点から、北米地域は予測期間中にAUV・ROV市場で大きな成長を示すことが期待されています。

オフショアAUV・ROV産業の概要

オフショアAUV・ROV市場は半分断されています。この市場の主要企業(順不同)には、DOF Subsea AS、Fugro NV、Subsea 7 SA、Saipem SpA、Oceaneering International Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- アメリカ、アジア太平洋、中東・アフリカ地域における石油・ガス海洋探査活動の増加

- オフショア再生可能技術の成長

- 抑制要因

- 複数地域におけるオフショア探査・生産活動の禁止

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 車両タイプ

- ROV

- AUV

- 車両クラス

- 作業車両クラス

- 軽作業車

- 中型作業車

- 重作業車

- 観測車クラス

- 作業車両クラス

- エンドユーザー用途

- 石油・ガス

- 防衛

- 研究

- その他の用途

- 活動

- 掘削と開発

- 建設

- 検査、修理、メンテナンス

- 廃止措置

- その他の活動

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- デンマーク

- ノルウェー

- ロシア

- フランス

- その他の欧州

- アジア太平洋

- 中国

- インド

- ASEAN諸国

- その他のアジア太平洋

- 南米

- ブラジル

- ベネズエラ

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- ナイジェリア

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- DeepOcean AS

- DOF Subsea AS

- Helix Energy Solutions Group Inc.

- TechnipFMC PLC

- Bourbon

- Fugro NV

- Subsea 7 SA

- Saipem SpA

- Oceaneering International Inc.

- Teledyne Technologies Incorporated

第7章 市場機会と今後の動向

- AUV・ROV市場における技術の進歩

目次

Product Code: 52273

The Offshore AUV And ROV Market size is estimated at USD 2.83 billion in 2025, and is expected to reach USD 4.10 billion by 2030, at a CAGR of 7.69% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising offshore oil and gas production activities, growing offshore wind power industry, and increasing oil and gas decommissioning activities are expected to drive the offshore AUV and ROV market during the forecast period.

- On the other hand, countries planning to increase their focus on climate change and banning offshore exploration activities in the future are expected to restrain market growth.

- Nevertheless, innovation and technological advancement are expected to increase the utilization of AUVs and ROVs in offshore activities in industries such as oil and gas, offshore wind, research, etc. The technological advancements in AUVs and ROVs are expected to offer a considerable opportunity for companies in the long term.

- North America is expected to witness significant growth, with the majority of the demand coming from countries such as the United States and Mexico.

Offshore AUV And ROV Market Trends

Oil and Gas Segment to Dominate the Market

- AUVs and ROVs are used for positioning and guidance for sub-sea infrastructure construction, monitoring, and survey missions. The applications of underwater vehicles in offshore oil and gas engineering include guide drilling work, undersea observation, fixed-point sampling, auxiliary work involved in jacket installation, laying of oil and gas pipelines, and maintenance of offshore facilities.

- The dependence on oil and gas increases as major economies globally still rely heavily on petroleum-based products. The oil and gas industry displays immense influence in international politics and economics.

- In 2022, global oil production recorded 93,848 thousand barrels per day, with an increase of 4.18% over the previous year. The increase in the global population was reflected in an increase in primary energy consumption, which stood at 604.04 exajoules in 2022, up from 520.90 exajoules in 2011.

- Many of the potential global reserves of hydrocarbons lie beneath the sea. The hydrocarbon industry developed techniques suited to conditions found in offshore sites, both to find oil and gas and produce it successfully.

- Oil and gas drilling rigs may operate in water depths of two miles. Many of these deepwater wells and pipeline systems rely on unmanned underwater vehicles to help perform installations, inspections, repairs, and maintenance.

- Several countries have recently been active in the oil and gas offshore sector and have been witnessing investments in increasing production from offshore fields, hence creating an opportunity for AUVs and ROVs.

- In May 2022, Shell and Petrobras contracted Saipem to use its FlatFish subsea drone for two pilot projects involving the inspection campaigns of two ultra-deepwater fields offshore Brazil operated by the two energy companies.

- Furthermore, in August 2022, Oil and Natural Gas Corp., an Indian oil explorer and producer, entered into a Heads of Agreement (HoA) with ExxonMobil Corp. for deepwater exploration on both the east and west coasts of the country. In the eastern offshore, both oil explorers plan to focus on the Krishna Godavari and Cauvery basins, and in the western offshore, they will focus on the Kutch-Mumbai region.

- Therefore, owing to the above points, the demand for offshore AUVs and ROVs is expected to grow significantly in the oil and gas sector during the forecast period.

North America is Expected to Witness Significant Growth

- The North American region has one of the most well-developed offshore oil and gas industries globally, with the primary areas of focus being the vast reserves in the Gulf of Mexico and offshore Alaska regions. As drilling depths have increased over the years, the volume of technically recoverable reserves has increased significantly, which attracted growing investments.

- Due to the high level of industrialization and investments in research and development, North America is expected to be one of the largest markets for offshore AUVs and ROVs during the forecast period.

- As the United States has invested heavily in the defense sector and the R&D of AUVs and ROVs, other related offshore sectors, like oil and gas, shipping, and renewable energy, have profited immensely from the technological advancements in the market studied. Due to this, the region is at the forefront of AUV and ROV technology. AUV and ROV manufacturers in the region export their products globally.

- The region has one of the most well-developed offshore oil and gas industries globally, with the primary areas of focus being the vast reserves in the Gulf of Mexico and the offshore Alaska region. As drilling depths have increased over the years, the volume of technically recoverable reserves has increased significantly, which attracted growing investments.

- As the United States invested heavily in expanding its oil and gas production capacity, the Gulf of Mexico has become a global hotspot for AUV and ROV demand. As of 2022, the Gulf of Mexico region was responsible for 97% and 15% of the US offshore and total hydrocarbon production, respectively. The region has one of the highest global densities of offshore rig deployment and consists of other oil and gas infrastructure, like production and drilling platforms, marine vessels, and pipeline networks.

- As ROV and AUV technology has become increasingly affordable, oil and gas producers in the United States have been investing in ROV and AUV services to obtain data and carry out routine maintenance work on subsea assets and surfaces. Despite the higher upfront cost compared to diving crews, ROVs and AUVs need less time to complete the same amount of work, which reduces overall project OPEX.

- Due to this, major oil and gas companies routinely deal out multiple contracts for ROVs and AUV services in the Gulf of Mexico. In September 2022, DOF Subsea USA announced that the company had been awarded multiple contracts in the Gulf of Mexico by leading regional oil and gas operators. The Jones Act Compliant vessel(s) operated by DOF Subsea will be utilized for around 180 days over a one-year term, performing a range of activities, including inspection, maintenance, repair, light construction, and commissioning support at multiple field locations.

- Traditionally, Mexico had a strong hydrocarbon industry. However, the average drilling depths in Mexico's offshore sector have been relatively lower than that of the United States. Due to this, Mexican oil and gas operators have fewer financial incentives to switch from diver-assisted to diverless services, such as ROVs and AUVs.

- However, as the Mexican government looks to revitalize the hydrocarbon sector and boost domestic hydrocarbon production, the country's oil and gas industry is expected to see large investments, especially from state oil and gas utility PEMEX. In March 2022, PEP, the E&P wing of the PEMEX, announced that it received approval for the exploration of the Uchukil block in shallow waters with an investment of USD 107-478 million based on the baseline and incremental scenarios.

- Similarly, Mexico also committed to investing USD 1.2 billion in the development of two new offshore fields in forthcoming years. Such large investments in the offshore sector are expected to drive the offshore AUV and ROV market in Mexico during the forecast period.

- Therefore, owing to the above points, the North American region is expected to witness significant growth in the AUV and ROV markets during the forecast period.

Offshore AUV And ROV Industry Overview

The offshore AUV and ROV market is semi-fragmented. Some of the key players in this market (in no particular order) include DOF Subsea AS, Fugro NV, Subsea 7 SA, Saipem SpA, and Oceaneering International Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Offshore Oil and Gas Exploration Activities in the American, Asia-Pacific, and Middle-East and African Regions

- 4.5.1.2 Growing Offshore Renewable Technologies

- 4.5.2 Restraints

- 4.5.2.1 Ban on Offshore Exploration and Production Activities in Multiple Regions

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 ROV

- 5.1.2 AUV

- 5.2 Vehicle Class

- 5.2.1 Work-class Vehicle

- 5.2.1.1 Light Work-class Vehicle

- 5.2.1.2 Medium Work-class Vehicle

- 5.2.1.3 Heavy Work-class Vehicle

- 5.2.2 Observatory-class Vehicles

- 5.2.1 Work-class Vehicle

- 5.3 End-user Application

- 5.3.1 Oil and Gas

- 5.3.2 Defense

- 5.3.3 Research

- 5.3.4 Other End-user Applications

- 5.4 Activity

- 5.4.1 Drilling and Development

- 5.4.2 Construction

- 5.4.3 Inspection, Repair, and Maintenance

- 5.4.4 Decommissioning

- 5.4.5 Other Activities

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Denmark

- 5.5.2.4 Norway

- 5.5.2.5 Russia

- 5.5.2.6 France

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 ASEAN Countries

- 5.5.3.4 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Venezuela

- 5.5.4.3 Argentina

- 5.5.4.4 Colombia

- 5.5.4.5 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 DeepOcean AS

- 6.3.2 DOF Subsea AS

- 6.3.3 Helix Energy Solutions Group Inc.

- 6.3.4 TechnipFMC PLC

- 6.3.5 Bourbon

- 6.3.6 Fugro NV

- 6.3.7 Subsea 7 SA

- 6.3.8 Saipem SpA

- 6.3.9 Oceaneering International Inc.

- 6.3.10 Teledyne Technologies Incorporated

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in the AUV and ROV Market