北米のAUVとROV:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

North America AUV and ROV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1635463

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

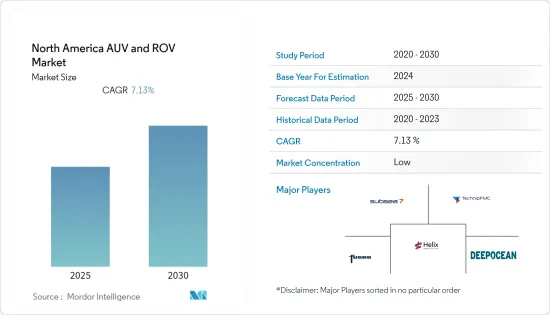

北米のAUVとROV市場は予測期間中に7.13%のCAGRで推移する見込み。

市場は2020年にCOVID-19の悪影響を受けました。現在、市場は流行前のレベルに達しています。

主要ハイライト

- 長期的には、海洋石油・ガス発見件数の増加、洋上風力発電設備の増加、石油・ガスの廃炉活動の活発化が市場を牽引する主要因です。

- その反面、化石燃料の使用増加による環境破壊が進み、北米地域では石油・ガスの海洋探査が禁止されているため、予測期間中は市場の鈍化が予想されます。

- AUVとROV市場の技術的進歩は、北米地域に巨大な機会をまもなく生み出すと期待されています。

- 米国は、防衛セグメントやAUVとROVの研究開発、石油・ガス、海運などの他の関連オフショアセグメントに多額の投資を行っているため、北米のAUVとROV市場を独占すると予想されます。

北米のAUVとROV市場動向

検査、修理、メンテナンス活動が大きな成長を遂げる

- 石油・ガス産業におけるROVの稼働率は、2014~2017年にかけて一貫して低下を記録し、その結果、稼働日数が減少しました。一般的に、点検・修理・保守(IRM)セグメントは、これらの作業が必要かつ避けられないと考えられているため、原油価格の変動から守られています。しかし、オフショア業務の大幅な減少と一部の業務の遅れが重なり、IRM AUVとROVサービス市場に強いマイナスの影響を与えました。

- 予測期間中、IRMセグメントは、特に米国やメキシコ湾を含む北米地域におけるオフショアインフラの老朽化が主要要因となり、大きな成長を記録すると予想されます。これらの老朽化したインフラは、頻繁な修理や保守活動とともに、より頻繁なモニタリングを必要とします。

- オフショア部門では、深海と超深海の事業が原油価格の下落により大きな打撃を受けました。低迷期には、産業は低価格のシナリオを採用し、プロジェクトのリエンジニアリング、効率化、経費管理の改善で対応し、その結果、総事業費は大幅に削減されました。こうした措置はすべて、産業の操業効率の改善につながっただけでなく、オフショア深海・超深海プロジェクトの損益分岐点価格の引き下げにもつながりました。

- また、オフショアプロジェクトの点検・修理・保守(IRM)サービスにROVを提供する企業も増えています。各社が提供している主要サービスには、無人点検、パイプライン保守、海底構造物モニタリング、海底エンジニアリングサービスなどがあります。例えば、Houston Mechatronics Inc.は2021年3月、自社開発のAUV/ROVトランスフォーマー「アクアノート」をアップグレードしたと発表しました。この多目的海中ロボットは、AUVをテザーレスROVに変身させることができ、大型船やアンビリカルを不要にします。このロボットの新しいバージョンであるアクアノートMk-IIは、最初のモデルよりも深い定格深度を持っています。これにより、データ収集だけでなく、保守・修理作業の遠隔操作が比較的低コストで可能になりました。

- したがって、上記の要因に基づき、検査、修理、保守活動は予測期間中に米国で大きな成長を示すと予想されます。

市場を独占する米国

- 米国は、防衛セグメントやAUVやROVの研究開発に多額の投資を行っており、石油・ガス、海運、再生可能エネルギーなど、他の関連オフショアセグメントも市場の技術進歩から多大な利益を得ています。このため、北米地域はAUVとROV技術の最前線にあり、同国のAUVとROVメーカーは製品を世界に輸出しています。

- 例えば、米国は2021年現在、世界で最も高い防衛予算、すなわち8,006億米ドルを費やしており、2015年の値(6,338億米ドル)と比較すると約26.3%増加しています。このため、AUVやROV船の研究開発が先駆けて進められてきました。ROVとAUVは米国海軍の海中能力の重要な部分を形成しています。2022年1月、アメリカのF-35CライトニングIIが南シナ海で墜落し、破片が海底に沈みました。F-35は最先端技術を搭載しており、敵対国が入手すると問題になるため、米国海軍は回収プログラムを開始しました。3月2日、残骸は海軍の主要な深海サルベージ車両であり、最大水深2万フィートまで活動できるCURV-21と呼ばれる船によって、水深1万2,400フィートで発見されました。

- 米国が石油・ガス生産能力の拡大に多額の投資を行っているため、メキシコ湾はAUVとROVの需要にとって世界のホットスポットとなっています。2021年現在、メキシコ湾地域は米国のオフショアと炭化水素総生産量のそれぞれ97%と15%を占めています。同国は、オフショア・リグの配備密度が世界で最も高い国の1つであり、生産・掘削プラットフォーム、海洋船舶、パイプライン・ネットワークなど、その他の石油・ガスインフラで構成されています。

- ROVやAUVの技術がますます手頃な価格になってきているため、米国の石油・ガス生産者は、海底資産や海面のデータ取得や定期的なメンテナンス作業のために、ROVやAUVサービスに投資する傾向にあります。ROVやAUVは、潜水作業員に比べて初期費用は高いもの、同じ量の作業を完了するのに必要な時間が短いため、プロジェクト全体のOPEXを削減することができます。

- このため、大手石油・ガス会社では、メキシコ湾でのROVとAUVサービスに対して複数の契約が日常的に結ばれています。2021年1月、Oceaneeringは、同社のサブシー部門が総額2億2,500万米ドルの複数の契約を獲得したと発表しました。これらの契約は、国際的な石油・ガス事業者や海洋建設会社から発行されたもので、契約サービスには、浮体式掘削リグやマルチサービス船、海底介入船、建設船から提供される遠隔操作車両(ROV)サービス、ROV工具、調査、測位、自律型海中ロボット(AUV)サービスなどが含まれます。

- したがって、上記の要因に基づいて、米国は予測期間中に北米地域のAUVとROV市場を独占すると予想されます。

北米のAUVとROV産業概要

北米のAUVとROV市場はセグメント化されています。同市場の主要企業(順不同)には、Subsea 7 SA、TechnipFMC PLC、DeepOcean AS、Helix Energy Solutions Group、Fugro NVなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2027年までの市場規模と需要予測(単位:100万米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 車種

- ROV

- AUV

- 車両クラス

- 作業クラス

- 観測クラス

- 用途

- 石油・ガス

- 防衛

- その他

- 活動

- 掘削と開発

- 建設

- 検査、修理、メンテナンス

- 廃止措置

- その他の活動

- 地域

- 米国

- カナダ

- その他の北米地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- DeepOcean AS

- DOF Subsea AS

- Helix Energy Solutions Group

- TechnipFMC PLC

- Fugro NV

- Oceaneering International Inc.

- Saipem SpA

- ROVOP

- Forum Energy Technologies Inc.

- Delta SubSea LLC

第7章 市場機会と今後の動向

目次

Product Code: 92205

The North America AUV and ROV Market is expected to register a CAGR of 7.13% during the forecast period.

The market was negatively impacted by COVID-19 in 2020. Presently, the market has now reached pre-pandemic levels.

Key Highlights

- Over the long term, the major driving factors of the market are increasing offshore oil and gas discoveries, growing offshore wind energy installations, and rising oil and gas decommissioning activities.

- On the flip side, increasing environmental damage due to increasing use of fossil fuels has let to ban of offshore exploration of oil and gas in North American region is expected to slow down the market during the forecast period.

- Nevertheless, technological advancements in the AUV and ROV market are expected to create huge opportunities for the North America region soon.

- United States is expected to dominate the AUV and ROV market in North America as the country heavily invested in defence sector and in the R&D of AUVs and ROVs, other related offshore sectors such oil and gas, shipping, etc.

North America AUV & ROV Market Trends

Inspection, Repair, and Maintenance Activity to Witness Significant Growth

- The utilization rates for ROV in the oil and gas industry registered a consistent decline during 2014-2017, resulting in declining day rates. Generally, the inspection, repair, and maintenance (IRM) segment is protected from the volatility in oil prices, as these operations are considered necessary and unavoidable. However, the combination of a substantial decline in offshore operations and delay in some of the activities had a strong negative impact on the IRM AUV and ROV services market.

- During the forecast period, the IRM segment is expected to register significant growth, mainly driven by ageing offshore infrastructure, particularly in the North American region which includes United States, and Gulf of Mexico. These ageing infrastructure require more frequent monitoring, along with frequent repair and maintenance activities.

- In the offshore sector, the deepwater and ultra-deepwater activities were hit harder by the decline in oil prices. During the period of downturn, the industry adopted a lower price scenario and responded with project re-engineering, efficiency gains, and better expense management, which resulted in a significant reduction of the total operating cost. All such steps have not only resulted in improving the operational efficiency in the industry but have also reduced the breakeven price of offshore deepwater and ultra-deepwater projects.

- Also, a growing number of companies are offering ROV for inspection, repair, and maintenance (IRM) services for offshore projects. Some of major services being offered by the companies include driverless inspection, pipeline maintenance, subsea structure monitoring, and subsea engineering services. For instance, in March 2021, Houston Mechatronics Inc. announced that it has upgraded its self-developed AUV/ROV transformer, Aquanaut, a multi-purpose subsea robot which can transform an AUV into a tetherless ROV, eliminating the need for large vessels and umbilicals. The new version of this robot, Aquanaut Mk-II, has a deeper depth rating than the first model. It enables collection of data as well as the remote operation of maintenance and repair tasks at a comparatively lower cost.

- Therefore, based on the above-mentioned factors, inspection, repair, and maintenance activity is expected to witness significant growth in the United States during the forecast period.

United States to Dominate the Market

- The United States has invested heavily in defence sector and in the R&D of AUVs and ROVs, other related offshore sectors such oil and gas, shipping and renewable energy have profited immensely from the technological advancements in the market. Due to this, the North American region is at forefront of the AUV and ROV technology, and AUV and ROV manufacturers in the country export their products globally.

- For instance, the United States, as of 2021 spent highest defence budget globally i.e., USD 800.6 billion, an increase of about 26.3% when compared to 2015 value (USD 633.8 billion). This has pioneered the R&D on AUV and ROV vessels. ROVs and AUVs form a critical part of the United States Navy's subsea capabilities. In January 2022, an American F-35C Lightning II crashed in the South China Sea, and the debris sunk to the ocean floor. As the F-35 jet model has cutting-edge technology which would be problematic if acquired by hostile nations, the US Navy started a recovery program. On March 2nd, the wreckage was discovered at a depth of 12,400 ft by an called a CURV-21, which is the Navy's primary deep sea salvage vehicle and can operate to a maximum depth of 20,000 feet.

- As the United States has invested heavily in expanding its oil and gas production capacity, the Gulf of Mexico has become a global hotspot for AUV and ROV demand. As of 2021, the Gulf of Mexico region is responsible for 97% and 15% of the United States' offshore and total hydrocarbon production, respectively. The country has one of the highest global density of offshore rig deployment, and consists of other oil and gas infrastructure such as production and drilling platforms, marine vessels and pipeline networks.

- As ROV and AUV technology has become increasingly affordable, oil and gas producers in the United States have been inclined towards investing in ROV and AUV services for obtaining data and carrying out routine maintenance work on subsea assets and surfaces. Despite the higher upfront cost when compared to diving crews, ROV and AUVs need lesser amount of time to complete the same amount of work, which reduces overall project OPEX.

- Due to this, multiple contracts are routinely dealt out by major oil and gas companies for ROVs and AUV services in the Gulf of Mexico. In January 2021, Oceaneering announced that its subsea segment had won multiple contracts totalling USD 225 million. The contracts were issued by iinternational oil and gas operators and marine construction companies, and the contracted services include remotely operated vehicle (ROV) services delivered from floating drilling rigs and multi-service, subsea intervention, and construction vessels, ROV tooling, survey, positioning, and autonomous underwater vehicle (AUV) services.

- Therefore, based on the above-mentioned factors, United States is expected to dominate the AUV and ROV market in North American region during the forecast period.

North America AUV & ROV Industry Overview

The North America AUV and ROV market is fragmented. Some of the major players in the market (in no particular order) include Subsea 7 SA, TechnipFMC PLC, DeepOcean AS, Helix Energy Solutions Group, and Fugro NV.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD million, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 ROV

- 5.1.2 AUV

- 5.2 Vehicle Class

- 5.2.1 Work-class Vehicle

- 5.2.2 Observatory-class Vehicle

- 5.3 Application

- 5.3.1 Oil and Gas

- 5.3.2 Defense

- 5.3.3 Other Applications

- 5.4 Activity

- 5.4.1 Drilling and Development

- 5.4.2 Construction

- 5.4.3 Inspection, Repair, and Maintenance

- 5.4.4 Decommissioning

- 5.4.5 Other Activities

- 5.5 Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 DeepOcean AS

- 6.3.2 DOF Subsea AS

- 6.3.3 Helix Energy Solutions Group

- 6.3.4 TechnipFMC PLC

- 6.3.5 Fugro NV

- 6.3.6 Oceaneering International Inc.

- 6.3.7 Saipem SpA

- 6.3.8 ROVOP

- 6.3.9 Forum Energy Technologies Inc.

- 6.3.10 Delta SubSea LLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

北米のAUVとROV:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日