|

市場調査レポート

商品コード

1911830

欧州の医薬品プラスチック包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Europe Pharmaceutical Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の医薬品プラスチック包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 133 Pages

納期: 2~3営業日

|

概要

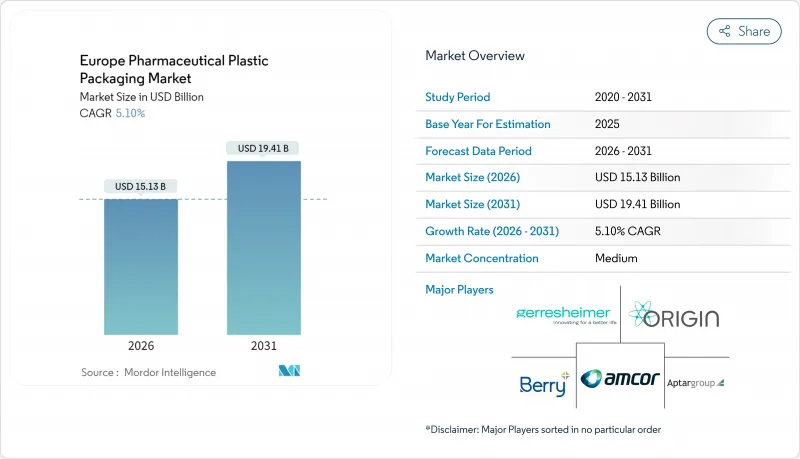

欧州の医薬品プラスチック包装市場は、2025年に144億米ドルと評価され、2026年の151億3,000万米ドルから2031年までに194億1,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは5.10%と見込まれます。

成長の鍵は、持続可能性への要請、バイオ医薬品の普及、在宅治療の拡大にあり、これらはそれぞれバリア特性、リサイクル性、ユーザー中心設計に対する性能要件を厳格化しています。主要サプライヤーは循環型経済目標と病院自動化プログラムを満たすため、再生材使用ラインとRFID対応フォーマットの拡充を進めています。一方、樹脂コストの変動や抽出物規制の強化により利益率が圧迫されており、規模の優位性を維持するため、原材料のヘッジング、サプライヤーの多様化、選択的な合併が進められています。既存企業が垂直統合を拡大する一方、専門企業がスマートソリューションやバイオベースソリューションのニッチ市場を獲得しているため、競争の激しさは中程度に留まっています。これにより、欧州の医薬品プラスチック包装市場全体で価格設定や協業モデルが再構築されています。

欧州の医薬品プラスチック包装市場の動向と洞察

子供用安全キャップおよび高齢者向けパッケージの需要増加

高齢化と小児安全規制の強化により、包装投資は触覚的な操作性と認証済みチャイルドレジスタンスを兼ね備えたキャップへ移行しています。欧州のコンバーター各社は新たな人間工学的キャッププラットフォームごとに200万~400万ユーロを投資しており、この取り組みにより2024年には患者中心システムの導入が18%増加しました。ネメラ社のトルク低減式キャップは、ISO 8317規格を上回る性能を維持しつつ開封力を30%低減し、使いやすさと安全性の両立を実証しています。欧州の医薬品庁(EMA)が2024年に発表した慢性疾患治療薬向けユーザーフレンドリー包装を推奨するガイドラインにより、規制面での後押しも得られました。早期導入企業からは、特に複雑なロック機構を支える金型精度が求められるポリプロピレン製キャップにおいて、初期コストが15~20%上昇するもの、プレミアム価格設定とブランドロイヤルティの向上により相殺されているとの報告が寄せられています。

高度な非経口プラスチックを必要とする生物学的製剤の急増

欧州における生物学的製剤の生産量は2024年に23%増加し、ドイツとスイスの工場ではモノクローナル抗体の生産が拡大しています。これらの高価値分子は、超低抽出物性とガラス不使用の耐破損性を要求するため、ポリプロピレンの3~4倍のコストながら化学的不活性性と透明性を提供する環状オレフィン共重合体および環状オレフィンポリマーの需要が加速しています。ショット・ファーマ社の1億5,000万ユーロ規模のバイアル増産計画は、特殊ポリマー製造能力へのサプライヤーの取り組みを裏付けています。バイオ医薬品対応包装材の成長率は欧州の医薬品プラスチック包装市場全体のほぼ2倍に達し、材料構成、認証スケジュール、サプライヤー統合のパターンを再構築しています。

変動するPPおよびPET樹脂価格

石油化学原料の供給障害とエネルギー価格の変動により、2024年にポリプロピレンとPETは15~20%上昇しました。BASFなどの生産者は四半期ごとの価格提示に移行し、変動リスクをコンバーター側に転嫁しています。コンバーターは製薬企業と複数年の供給契約を結ぶことが多いためです。ヘッジ能力に乏しい中小企業は圧迫に直面し、統合の波を引き起こしています。一方、大手グループは供給源の多様化や自社リサイクルへの投資により価格変動の影響を緩和しています。多くの中堅コンバーターでは、原材料費の30~40%が四半期ごとの調整条項の対象となっており、欧州の医薬品プラスチック包装市場全体の予測可能性が損なわれています。

セグメント分析

ポリプロピレンは、コスト効率性、耐薬品性、規制面での広範な認知度を背景に、2025年においても欧州の医薬品プラスチック包装市場で35.20%のシェアを維持しました。医薬品用PPの年間消費量は18万トンを超え、キャップ、ブリスター包装、注射器などをカバーしています。しかしながら、欧州の医薬品プラスチック包装市場規模は高密度ポリエチレン(HDPE)へ移行しつつあり、5.74%のCAGRで成長しています。HDPEは優れた防湿・防酸素バリア性により生物学的製剤の安定性要件を満たすと同時に、PPWR(プラスチックリサイクル規制)下でより高いリサイクル可能性を提示しているためです。

持続可能性への転換は医療用グレードの再生PET(rPET)の需要を高め、バイオベースグレードの試験導入を促進しています。ゲレスハイマー社は医薬品純度基準を満たす再生PET製点滴ボトルの商業生産を開始しました。ニッチなポリマー(COC、COP、PLAブレンド)は300~400%のプレミアム価格ながら、超低抽出物が必須の非経口製剤分野で採用が進んでいます。ショット・ファーマ社のCOC生産拡大は、こうした特殊樹脂の需要増を裏付けています。ポリプロピレン供給業者は、使用済みプラスチック原料の流れを試験的に導入することで対応していますが、欧州の医薬品プラスチック包装市場における主導的地位を維持するためには、臭気、色調、トレーサビリティに関する技術的課題を克服する必要があります。

欧州の医薬品プラスチック包装市場は、原材料別(ポリプロピレン、ポリエチレンテレフタレート、低密度ポリエチレン、高密度ポリエチレン、その他)、製品タイプ別(固形容器、液体・点滴用ボトル、点鼻薬ボトル、口腔ケアパック、パウチ/サシェ、バイアル・アンプル、その他)、および国別で区分されています。市場予測は金額ベース(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 子供用安全包装および高齢者向け包装の需要増加

- 高度な非経口プラスチックを必要とする生物学的製剤の急増

- EU循環型経済規則がリサイクル可能プラスチックを加速

- 電子商取引による医薬品流通の拡大が二次包装の保護機能強化を促進

- 在宅注射療法が小型PPプレフィルドシリンジを牽引

- 病院自動化向けロボティクス対応RFIDブリスター包装

- 市場抑制要因

- PPおよびPET樹脂価格の変動性

- 抽出物・溶出物に関するより厳格な規制基準

- 注射剤におけるガラス・アルミニウム代替

- 医療用再生樹脂の供給不足

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 業界バリューチェーン分析

- マクロ経済動向の影響

第5章 市場規模と成長予測

- 原材料別

- ポリプロピレン(PP)

- ポリエチレンテレフタレート(PET)

- 低密度ポリエチレン(LDPE)

- 高密度ポリエチレン(HDPE)

- その他(COP、COC、PVCフリーブレンド、バイオポリマー)

- 製品タイプ別

- 固形容器

- 液体・スポイトボトル

- 鼻腔スプレーボトル

- 口腔ケアパック

- パウチ/サシェ

- バイアルおよびアンプル(ポリマー)

- カートリッジ

- プレフィルドシリンジ

- キャップおよびクロージャー

- その他(単回投与用ストリップ、吸入器用キャニスター)

- 国別

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ベルギー

- スウェーデン

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Gerresheimer AG

- Amcor PLC

- Berry Global Group Inc.

- AptarGroup Inc.

- Origin Pharma Packaging

- Pretium Packaging

- Klckner Pentaplast

- Comar

- Gil Plastic Products Ltd

- Drug Plastics Group

- West Pharmaceutical Services Inc.

- Nemera

- Bormioli Pharma

- Alpla Group

- Sanner GmbH

- Tekni-Plex

- Weener Plastics

- Jabil Healthcare(Nypro)

- Stevanato Group(EZ-fill polymer vials)

- Raumedic AG