医薬品プラスチック包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Pharmaceutical Plastic Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665363

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

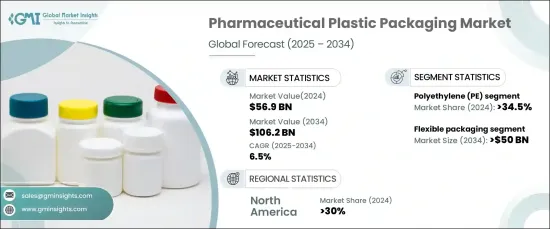

世界の医薬品プラスチック包装市場は、2024年に569億米ドルと評価され、2025~2034年にかけてCAGR 6.5%で成長すると予測されています。

この産業は、安全性、使いやすさ、規制要件の遵守における技術革新によって大きな変化を遂げつつあります。この成長に寄与している主要動向の1つは、改ざん防止包装や小児用包装に対する需要の高まりです。消費者の安全が最優先事項となるにつれ、メーカーは保護機能を強化し、製品への不正アクセスを防止するために、破損可能なキャップ、タンパーシール、視覚インジケータなどの先進的機能を組み込むようになってきています。

同市場は、ポリエチレン(PE)、ポリプロピレン(PP)、ポリエチレンテレフタレート(PET)、ポリ塩化ビニル(PVC)、その他など、材料タイプによって分類されます。ポリエチレン(PE)セグメントは、2024年に34.5%と圧倒的な市場シェアを占めています。ポリエチレンは汎用性、耐久性、手頃な価格で広く支持されており、ボトル、容器、軟包装など様々な医薬品包装ソリューションの製造に最適です。ポリエチレンは湿気や化学品に強いため、保管や輸送中にデリケートな医薬品を保護するのに特に効果的です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 569億米ドル |

| 予測金額 | 1,062億米ドル |

| CAGR | 6.5% |

包装タイプ別に見ると、市場は軟包装と硬包装に分けられます。軟包装はCAGR 7.5%で成長し、2034年には500億米ドルに達すると予測されます。このセグメントは、利便性、費用対効果、持続可能性などの主要な利点を提供し、医薬品包装産業で急速に普及しています。軟包装には、パウチ・小袋、ブリスターパック、ストリップパックなどの製品があり、錠剤、カプセル剤、粉末、液体などの医薬品包装に一般的に使用されています。これらの包装ソリューションは湿気、酸素、光に対して優れた保護を提供し、医薬品の完全性を保ち、保存期間を延ばすのに役立っています。

北米の医薬品プラスチック包装市場は2024年に30%を占めました。米国では、持続可能性の重視とスマート技術の統合によって市場が急成長しています。製造業者は環境目標を達成するため、再生プラスチックや生分解性オプションなど、エコフレンドリー材料の採用を増やしています。さらに、QRコードやRFIDタグのような技術は、製品のトレーサビリティ、真正性、患者エンゲージメントを強化するために取り入れられ、市場をさらに前進させています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次データ

- 二次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 変革

- 将来の展望

- メーカー

- 流通業者

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 慢性疾患の増加と高齢化

- 小児用耐性包装と開封防止包装の採用拡大

- 遠隔医療の成長による安全な宅配包装へのニーズの高まり

- 単位用量と複数用量の包装形態の使用の増加

- 特殊な包装を必要とする生物製剤の急速な拡大

- 産業の潜在的リスク・課題

- コスト効率と高性能包装ソリューションのバランス

- 多層と特殊プラスチック包装のリサイクルにおける課題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:材料別、2021~2034年

- 主要動向

- ポリエチレン(PE)

- ポリプロピレン(PP)

- ポリエチレンテレフタレート(PET)

- ポリ塩化ビニル(PVC)

- その他

第6章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- ボトル

- ブリスターパック

- シリンジとバイアル

- フィルムとラップ

- チューブ

- パウチ・小袋

- その他

第7章 市場推定・予測:包装タイプ別、2021~2034年

- 主要動向

- 軟包装

- 硬包装

第8章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 経口医薬品

- 注射剤

- 外用薬

- その他

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Amcor

- APG Pharma

- Aptar

- Berry Global

- Bormioli

- CL Smith

- Comar

- Constantia

- Drug Plastics

- DWK

- Frapak

- Gerresheimer

- Klockner

- Medicopack

- Nelipak

- Origin Pharma

- Plascene

- Silgan

目次

The Global Pharmaceutical Plastic Packaging Market, valued at USD 56.9 billion in 2024, is projected to grow at a CAGR of 6.5% between 2025-2034. The industry is undergoing significant changes, driven by innovations in safety, user-friendliness, and adherence to regulatory requirements. One of the key trends contributing to this growth is the rising demand for tamper-evident and child-resistant packaging. As consumer safety becomes a top priority, manufacturers are increasingly incorporating advanced features like breakable caps, tamper seals, and visual indicators to enhance protection and prevent unauthorized access to products.

The market is categorized by material types, including polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), polyvinyl chloride (PVC), and others. The polyethylene (PE) segment holds a dominant market share of 34.5% in 2024. Polyethylene is widely favored for its versatility, durability, and affordability, making it ideal for manufacturing various pharmaceutical packaging solutions such as bottles, containers, and flexible packaging. Its resistance to moisture and chemicals makes it particularly effective at protecting sensitive medications during storage and transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $56.9 Billion |

| Forecast Value | $106.2 Billion |

| CAGR | 6.5% |

In terms of packaging types, the market is divided into flexible and rigid packaging. Flexible packaging is expected to grow at a CAGR of 7.5%, reaching USD 50 billion by 2034. This segment is rapidly gaining traction in the pharmaceutical packaging industry, offering key advantages like convenience, cost-effectiveness, and sustainability. Flexible packaging includes products like pouches, sachets, blister packs, and strip packs, which are commonly used for packaging pharmaceuticals such as tablets, capsules, powders, and liquids. These packaging solutions provide excellent protection against moisture, oxygen, and light, helping to preserve the integrity and extend the shelf life of pharmaceutical products.

North America pharmaceutical plastic packaging market held 30% in 2024. In the United States, the market is seeing rapid growth, driven by a focus on sustainability and the integration of smart technologies. Manufacturers are increasingly adopting eco-friendly materials, such as recycled plastics and biodegradable options, to meet environmental goals. Additionally, technologies like QR codes and RFID tags are being incorporated to enhance product traceability, authenticity, and patient engagement, further propelling the market forward.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Disruptions

- 3.1.3 Future outlook

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.2 Profit margin analysis

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Rising prevalence of chronic diseases and aging population

- 3.5.1.2 Growing adoption of child-resistant and tamper-evident packaging

- 3.5.1.3 Growth of telemedicine fueling need for secure home-delivery packaging

- 3.5.1.4 Rising use of unit dose and multi-dose packaging formats

- 3.5.1.5 Rapid expansion of biologics necessitating specialized packaging

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Balancing cost-efficiency with high-performance packaging solutions

- 3.5.2.2 Challenges in recycling multi-layer and specialized plastic packaging

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene (PE)

- 5.3 Polypropylene (PP)

- 5.4 Polyethylene Terephthalate (PET)

- 5.5 Polyvinyl Chloride (PVC)

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Bottles

- 6.3 Blister packs

- 6.4 Syringes and vials

- 6.5 Films and wraps

- 6.6 Tubes

- 6.7 Pouches and sachets

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Flexible packaging

- 7.3 Rigid packaging

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Oral drugs

- 8.3 Injectable drugs

- 8.4 Topical drugs

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amcor

- 10.2 APG Pharma

- 10.3 Aptar

- 10.4 Berry Global

- 10.5 Bormioli

- 10.6 CL Smith

- 10.7 Comar

- 10.8 Constantia

- 10.9 Drug Plastics

- 10.10 DWK

- 10.11 Frapak

- 10.12 Gerresheimer

- 10.13 Klockner

- 10.14 Medicopack

- 10.15 Nelipak

- 10.16 Origin Pharma

- 10.17 Plascene

- 10.18 Silgan

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日