北米の衛星バス:市場シェア分析、産業動向、成長予測(2025年~2030年)

North America Satellite Bus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 167 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693950

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

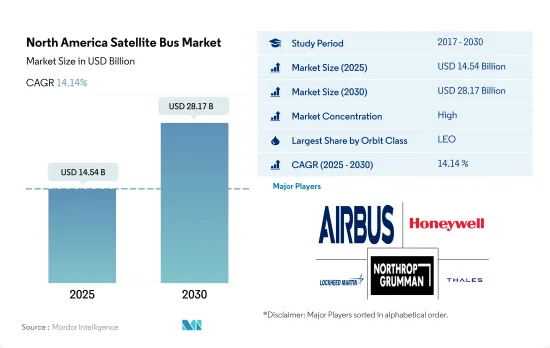

北米の衛星バス市場規模は2025年に145億4,000万米ドルと推定・予測され、2030年には281億7,000万米ドルに達し、予測期間中(2025~2030年)にCAGR 14.14%で成長すると予測されています。

様々な衛星用途でLEO軌道への衛星打ち上げが増加し、市場需要を牽引

- 北米の衛星バス市場は、通信やナビゲーションからリモートセンシングや科学研究まで幅広い用途で、衛星ベースのサービスに対する需要の増加が市場を牽引しています。

- LEO衛星は、地球観測、リモートセンシング、科学研究などの用途で需要があります。LEO衛星には、Boeing502フェニックス、Lockheed MartinLM400、ノースロップ・グラマンGeoStar-3など、さまざまな企業がさまざまなバスソリューションを提供しています。これらのバスは、さまざまなLEO用途をサポートするように設計されています。2017~2022年の間に、約3,021機の衛星がLEOに打ち上げられました。

- 大容量データ伝送、世界カバレッジ、高画質放送機能のニーズが、GEO衛星の需要を牽引しています。GEO軌道では、Boeing702、Lockheed MartinA2100、マキサー・ Technologies1300クラスなど、さまざまな企業が通信・放送ミッションのための革新的なソリューションを提供しています。これらのバスは、衛星を利用したサービスに長期間安定したサービスを提供するよう設計されています。2017~2022年の間に、約33機の衛星がGEOに打ち上げられました。

- MEO衛星は通信やナビゲーションなどの用途に使用されます。MEO衛星の需要は、大容量データ伝送、ナビゲーション能力の向上、先進的画像技術の必要性によって牽引されています。Airbus社、Boeing社、Lockheed Martin社などの企業は、Airbus社のユーロスター・ネオ、Boeing社の702MP、Lockheed Martin社のLM2100など、通信やナビゲーションのミッションに先進的ソリューションを提供しています。2017~2022年にかけて、約7機の衛星がMEOに打ち上げられました。このような開発により、市場全体は2023~2029年にかけて17%の成長が見込まれています。

北米の衛星バス市場動向

燃料効率と運用効率向上の動向が見られる

- 衛星バス(または宇宙船バス)は、衛星や宇宙船の本体であり構造部品であり、その中にペイロードやすべての科学機器が搭載されます。さらに、軍事と民生の二重目的での商業衛星プラットフォームの利用拡大が、衛星バス市場を押し上げています。衛星通信は5Gインフラにとって不可欠な要素になると考えられています。地上と衛星間のシームレスな接続性を提供するため、衛星輸送コンジットは全体的な通信マップに統合されつつあります。これにより、都市部や農村部で衛星サービスを拡大する新たな機会が生まれます。

- 中国は、宇宙ベースの能力増強に向けて多大な資源を投入しています。同国はアジア太平洋で最多の超小型衛星を打ち上げています。2022年4月、中国の新興企業SpaceWishの超小型衛星がCZ-2C(3)ロケットに搭乗してLEOに打ち上げられました。XINGYUAN-2は6Uのリモートセンシング用キューブサットで、重量は約7.5kgです。

- 加えて、超小型衛星や超小型衛星の自主開発は、インドの産業が力を入れているセグメントのひとつです。多くの新興企業や大学が、国内の様々なレベルでこれらの衛星を開発しています。例えば、2018年12月、Exseed SpaceはExseedSAT 1と名付けられた超小型衛星を打ち上げ、無線アマチュアに重要な通信を提供しました。これはインド初の民間所有の衛星の宇宙進出でした。オーストラリア、マレーシア、韓国、シンガポールなどの国も超小型衛星の開発に投資しています。

各宇宙機関の宇宙開発費の増加は、衛星産業にプラスの影響を与えると予想されます。

- 北米の宇宙プログラムへの政府支出は、2021年には約200億米ドルに達します。この地域は、世界最大の宇宙機関であるNASAが存在する、宇宙イノベーションと研究の震源地です。以来、このセグメントへの大規模な投資は、他の様々なサブシステム部品メーカーを引き付け、彼らに機会を創出しています。

- この地域では、2022年に米国政府が宇宙プログラムに240億米ドル近くを投じ、世界で最も宇宙開発費を投じた国となっています。カナダ政府によると、米国とは別に、カナダの宇宙部門はカナダのGDPに23億米ドルを上乗せし、1万人を雇用しています。カナダ政府の報告によると、カナダの宇宙関連企業の90%は中小企業です。カナダ宇宙庁(CSA)の予算は控えめで、2022~23年の予算支出見込み額は3億2,900万米ドルです。

- 調査と投資助成に関しては、この地域の政府と民間セクタは、宇宙セグメントの研究とイノベーションのために専用の資金を用意しています。各機関は、義務と呼ばれる金銭的約束をすることで、利用可能な予算資源を費やしています。例えば、2023年2月まで、米国航空宇宙局(NASA)は研究助成金として3億3,300万米ドルを分配しました。

北米の衛星バス産業概要

北米の衛星バス市場はかなり統合されており、上位5社で71%を占めています。この市場の主要企業は、Airbus SE、Honeywell International Inc.、Lockheed Martin Corporation、Northrop Grumman Corporation、Thalesです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 衛星の小型化

- 衛星質量

- 宇宙開発への支出

- 規制の枠組み

- カナダ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 用途

- 通信

- 地球観測

- ナビゲーション

- 宇宙観測

- その他

- 衛星質量

- 10~100kg

- 100~500kg

- 500~1,000kg

- 10kg以下

- 1,000kg以上

- 軌道クラス

- GEO

- LEO

- MEO

- エンドユーザー

- 商業

- 軍事・政府

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- Ball Corporation

- Honeywell International Inc.

- Lockheed Martin Corporation

- Nano Avionics

- NEC

- Northrop Grumman Corporation

- Sierra Nevada Corporation

- Thales

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50001264

The North America Satellite Bus Market size is estimated at 14.54 billion USD in 2025, and is expected to reach 28.17 billion USD by 2030, growing at a CAGR of 14.14% during the forecast period (2025-2030).

Increasing launches of satellites into LEO orbit for various satellite applications is driving the market demand

- The North American satellite bus market is driven by the increasing demand for satellite-based services, with applications ranging from communication and navigation to remote sensing and scientific research.

- LEO satellites are in demand for applications such as Earth observation, remote sensing, and scientific research. For LEO satellites, various companies offer a range of bus solutions, including the Boeing 502 Phoenix, the Lockheed Martin LM 400, and the Northrop Grumman GeoStar-3. These buses are designed to support a range of LEO applications. Between 2017 and 2022, approximately 3,021 satellites were launched into LEO.

- The need for high-capacity data transmission, global coverage, and high-quality broadcasting capabilities drives the demand for GEO satellites. For GEO orbit, various companies offer innovative solutions for communication and broadcasting missions, including the Boeing 702, the Lockheed Martin A2100, and the Maxar Technologies 1300-class. These buses are designed to provide long-term, stable service for satellite-based services. Between 2017 and 2022, approximately 33 satellites were launched into GEO.

- MEO satellites are used for applications such as communication and navigation. The demand for MEO satellites is driven by the need for high-capacity data transmission, improved navigation capabilities, and advanced imaging technologies. Companies like Airbus, The Boeing Company, and Lockheed Martin offer advanced solutions for communication and navigation missions, including the Airbus Eurostar Neo, the Boeing 702MP, and the Lockheed Martin LM 2100. Between 2017 and 2022, approximately seven satellites were launched into MEO. With such developments, the overall market is expected to grow by 17% during 2023-2029.

North America Satellite Bus Market Trends

The trend for better fuel and operational efficiency has been witnessed

- A satellite bus (or spacecraft bus) is the main body and structural component of a satellite or spacecraft, in which the payload and all scientific instruments are held. Moreover, the growing utilization of commercial satellite platforms for dual (military and civil) purposes has boosted the satellite bus market. Satellite communications are envisioned to be an essential part of the 5G infrastructure. In order to provide seamless connectivity between terrestrial and satellite, the satellite transport conduit is being integrated into the overall communication map. This will result in new opportunities for extending satellite services in urban and rural areas.

- China is investing significant resources toward augmenting its space-based capabilities. The country has launched the largest number of nano and microsatellites in Asia-Pacific. In April 2022, Chinese startup SpaceWish's nanosatellite was launched into LEO boarding CZ-2C (3) rocket. XINGYUAN-2 is a 6U remote sensing CubeSat that weighs approximately 7.5 kg.

- In addition, the indigenous development of nano and microsatellites has been one of the areas of emphasis for the industry in India. Many startups and universities are developing these satellites at various levels in the country. For instance, in December 2018, Exseed Space launched a nanosatellite named ExseedSAT 1 to provide vital communication for radio amateurs. This was India's first privately owned satellite into space. Countries like Australia, Malaysia, South Korea, and Singapore are also investing in the development of nano and microsatellites.

The increasing space expenditures of different space agencies are expected to impact the satellite industry positively

- Government's spending on space programs in North America hit approximately around 20 billion in 2021. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. Since, the major investments in this field attracts various other sub system and component manufacturers and creates opportunities for them.

- In the region, in 2022, the US government spent nearly USD 24 billion on its space programs, making it the highest spender on space in the world. Apart from the United States, the Canadian space sector adds USD 2.3 billion to the Canadian GDP and employs 10,000 people, according to the Canadian government. The government reports that 90% of Canadian space firms are small- and medium-sized businesses. The Canadian Space Agency (CSA) budget is modest, and the estimated budgetary spending for 2022-23 was USD 329 million.

- In terms of research and investment grant, the region's governments and the private sector have dedicated funds for research and innovation in the space sector. Agencies spend available budgetary resources by making financial promises called obligations. For instance, till February 2023, the National Aeronautics and Space Administration (NASA) distributed USD 333 million as research grants.

North America Satellite Bus Industry Overview

The North America Satellite Bus Market is fairly consolidated, with the top five companies occupying 71%. The major players in this market are Airbus SE, Honeywell International Inc., Lockheed Martin Corporation, Northrop Grumman Corporation and Thales (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Satellite Mass

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 Canada

- 4.4.2 United States

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Satellite Mass

- 5.2.1 10-100kg

- 5.2.2 100-500kg

- 5.2.3 500-1000kg

- 5.2.4 Below 10 Kg

- 5.2.5 above 1000kg

- 5.3 Orbit Class

- 5.3.1 GEO

- 5.3.2 LEO

- 5.3.3 MEO

- 5.4 End User

- 5.4.1 Commercial

- 5.4.2 Military & Government

- 5.4.3 Other

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Airbus SE

- 6.4.2 Ball Corporation

- 6.4.3 Honeywell International Inc.

- 6.4.4 Lockheed Martin Corporation

- 6.4.5 Nano Avionics

- 6.4.6 NEC

- 6.4.7 Northrop Grumman Corporation

- 6.4.8 Sierra Nevada Corporation

- 6.4.9 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

北米の衛星バス:市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 167 Pages

- 納期

- 2~3営業日