欧州の衛星バス市場:シェア分析、産業動向、成長予測(2025年~2030年)

Europe Satellite Bus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 171 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693939

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

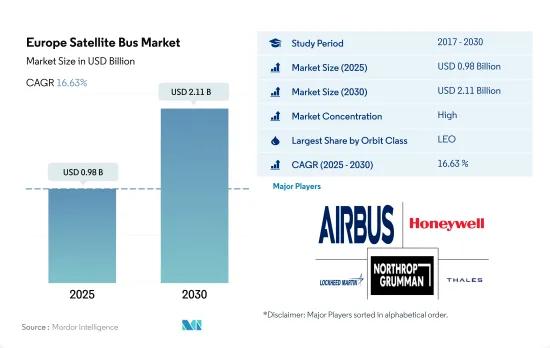

欧州の衛星バス市場規模は2025年に9億8,000万米ドルと予測され、2030年には21億1,000万米ドルに達し、予測期間中(2025~2030年)にCAGR 16.63%で成長すると予測されています。

様々な衛星用途でLEO軌道への衛星打ち上げが増加し、市場需要を牽引

- LEO衛星は気象観測、地球観測、リモートセンシングなど様々な用途に利用されています。欧州では、Surrey Satellite Technology Limited(SSTL)が開発したSSTL-150バスなどの衛星バスがLEO衛星に使用されています。SSTL-150バスは、カメラ、AIS(自動認識システム)受信機、小型衛星など、さまざまなペイロードをサポートできる汎用性の高いプラットフォームです。2017~2022年の間に、約531機の衛星がLEOに打ち上げられました。

- GEO衛星は、衛星ベースのテレビ放送、天気予報、軍事通信システムなどの用途に使用されます。欧州の衛星メーカーは、タレスアレニア・スペース社が開発したスペースバスNEOなどのバス設計をGEO衛星に使用しています。スペースバスNEOは、大型テレビ放送用アンテナやハイパワーアンプなど、幅広いペイロードに対応できる高性能プラットフォームです。2017~2022年にかけて、約16基の衛星がGEOに打ち上げられました。

- MEO衛星は、GPSやガリレオなどの世界のナビゲーションシステム(GNSS)や衛星ベースのブロードバンドサービスに使用されます。欧州の衛星メーカーは、Airbus Defense and Spaceが開発したEurostar E3000バスをはじめ、MEO用途にさまざまなバス設計を採用しています。Eurostar E3000バスは、数多くのMEOアプリケーションに使用されてきた信頼性の高いプラットフォームです。このバスの標準化されたプラットフォームにより、衛星メーカーはさまざまな用途のMEO衛星を高い信頼性とコスト効率で製造することができます。2017~2022年の間に、約16機の衛星がMEOに打ち上げられました。、市場全体は2023~2029年の間に19.43%の成長が見込まれています。

欧州の衛星バス市場動向

欧州の衛星産業は、特定の用途のニーズに合わせて設計された衛星設計・製造のための強力なアーキテクチャの恩恵を受けています。

- 宇宙船を質量で分類することは、ロケットのサイズと衛星を軌道に打ち上げるコストを決定する主要指標の1つです。衛星ミッションの成功は、飛行前の質量測定の精度と、制限内で質量を発生させるための衛星の適切なバランスに大きく依存します。

- 衛星は質量によって分類され、主要質量分類は1,000kgを超える大型衛星です。2017~2022年の間に、欧州の組織が所有する35以上の大型衛星が打ち上げられました。中型衛星は質量が500kgから1,000kgの衛星です。欧州の組織は、過去の期間に打ち上げられた15以上の衛星を運用していました。500kg以下の衛星は小型衛星と呼ばれ、欧州では460機以上が打ち上げられています。

- 開発期間が短く、ミッション全体のコストを削減できることから、この地域では小型衛星への移行傾向が強まっています。これらの衛星によって、科学的技術的成果を得るために必要な時間を大幅に短縮することが可能になりました。小型衛星のミッションは柔軟性が高く、新たな技術的機会やニーズによりよく対応できる傾向があります。欧州の小型衛星産業は、特定の用途に合わせた小型衛星を設計・製造するための強固な枠組みの存在によって支えられています。欧州での運用数は、商業と軍事宇宙セグメントでの需要増に牽引され、2023~2029年の間に増加すると予想されます。

さまざまな宇宙機関の宇宙開発費の増加は、欧州の衛星産業にプラスの影響を与えると予想されます。

- 民間/政府、商業、軍事セグメントからの衛星需要の増加は近年確認されています。現在、フランスやドイツなど一部の欧州諸国は、衛星バス製造セグメントで十分な能力を有しています。しかし、小型衛星の製造へのシフトが進んでいるため、衛星バスの製造拠点は欧州全域で拡大すると予想されます。

- 欧州諸国は宇宙領域における様々な投資の重要性を認識しており、世界の宇宙産業において競合と革新性を維持するために、地球観測、衛星航法、接続性、宇宙研究、技術革新などのセグメントへの支出を増やしています。

- この点に関して、2022年11月、ESAは、地球観測における欧州のリードを維持し、航法サービスを拡大し、米国との探査におけるパートナーであり続けることを目的として、今後3年間で宇宙資金を25%増額することを提案したと発表しました。欧州宇宙機関(ESA)は、2023~2025年の185億ユーロの予算を支持するよう22カ国に要請しました。2022年9月、フランスは、ESAが自らの大幅な予算増額に向けたコミットメントの確保に努める中、国家と欧州の宇宙プログラムへの支出を増加させる計画を発表しました。政府は、過去3年間で約25%増となる90億米ドル以上を宇宙活動に充てる計画を発表しました。

欧州の衛星バス産業概要

欧州の衛星バス市場はかなり統合されており、上位5社で71%を占めています。この市場の主要企業は、Airbus SE、Honeywell International Inc.、Lockheed Martin Corporation、Northrop Grumman Corporation、Thalesです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 衛星の小型化

- 衛星質量

- 宇宙開発への支出

- 規制の枠組み

- フランス

- ドイツ

- ロシア

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 用途

- 通信

- 地球観測

- ナビゲーション

- 宇宙観測

- その他

- 衛星質量

- 10~100kg

- 100~500kg

- 500~1,000kg

- 10kg以下

- 1,000kg以上

- 軌道クラス

- GEO

- LEO

- MEO

- エンドユーザー

- 商業

- 軍事・政府

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- Ball Corporation

- Honeywell International Inc.

- Lockheed Martin Corporation

- Nano Avionics

- NEC

- Northrop Grumman Corporation

- OHB SE

- Sierra Nevada Corporation

- Thales

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50001251

The Europe Satellite Bus Market size is estimated at 0.98 billion USD in 2025, and is expected to reach 2.11 billion USD by 2030, growing at a CAGR of 16.63% during the forecast period (2025-2030).

Increasing launches of satellites into LEO orbit for various satellite applications is driving the market demand

- LEO satellites are used for various applications, including weather monitoring, Earth observation, and remote sensing. In Europe, satellite buses such as the SSTL-150 bus developed by Surrey Satellite Technology Limited (SSTL) are used for LEO satellites. The SSTL-150 bus is a versatile platform that can support a range of payloads, including cameras, AIS (Automatic Identification System) receivers, and small satellites. Between 2017 and 2022, approximately 531 satellites were launched into LEO.

- GEO satellites are used for applications such as satellite-based television broadcasting, weather forecasting, and military communication systems. European satellite manufacturers use bus designs such as the Spacebus NEO developed by Thales Alenia Space for GEO satellites. The Spacebus NEO is a highly capable platform that can support a wide range of payloads, including large television broadcasting antennas and high-power amplifiers. Between 2017 and 2022, approximately 16 satellites were launched into GEO.

- MEO satellites are used for global navigation systems (GNSS) such as GPS and Galileo and satellite-based broadband services. European satellite manufacturers use a variety of bus designs for MEO applications, including the Eurostar E3000 bus developed by Airbus Defense and Space. The Eurostar E3000 bus is a reliable platform that has been used for numerous MEO applications. The standardized platform of the bus enables satellite manufacturers to build a range of MEO satellites for different applications with a high degree of reliability and cost-effectiveness. Between 2017 and 2022, approximately 16 satellites were launched into MEO. And the overall market is expected to grow by 19.43% during 2023-2029.

Europe Satellite Bus Market Trends

Europe's satellite industry benefits from a strong architecture for satellite design and manufacture, designed to meet specific application needs

- Classifying spacecraft by mass is one of the main metrics for determining launch vehicle size and the cost of launching satellites into orbit. The success of a satellite mission depends heavily on the accuracy of its pre-flight mass measurement and the proper balance of the satellite to generate mass within limits.

- Satellites are classified according to their mass, and the main mass classifications are large satellites over 1,000 kg. Between 2017 and 2022, more than 35+ large satellites owned by European organizations were launched. A medium-sized satellite has a mass between 500 kg and 1,000 kg. European organizations operated more than 15+ satellites that were launched during the historical period. Satellites with a mass of less than 500 kg are considered small satellites, and about 460+ small satellites were launched in the region.

- There is a growing trend toward smaller satellites in the region due to their shorter development times, which can reduce overall mission costs. These satellites have made it possible to significantly reduce the time required to obtain scientific and technological results. Small spacecraft missions tend to be flexible and can better respond to new technological opportunities or needs. The small satellite industry in Europe is supported by the presence of a robust framework for designing and manufacturing small satellites tailored to serve specific application profiles. The number of operations in the European region is expected to increase during 2023-2029, driven by the growing demand in the commercial and military space sectors.

Increasing space expenditures of different space agencies are expected to positively impact the European satellite industry

- Increased demand for satellites from the civil/government, commercial, and military sectors has been witnessed over recent years. Currently, some European countries, such as France and Germany, have adequate capabilities in the field of satellite bus manufacturing. However, due to the growing shift toward manufacturing smaller satellites, the manufacturing base of satellite buses is expected to expand across Europe.

- European countries are recognizing the importance of various investments in the space domain and increasing their spending in areas such as Earth observation, satellite navigation, connectivity, space research, and innovation to stay competitive and innovative in the global space industry.

- On this note, in November 2022, ESA announced that it had proposed a 25% boost in space funding over the next three years designed to maintain Europe's lead in Earth observation, expand navigation services, and remain a partner in exploration with the United States. The European Space Agency (ESA) has asked its 22 nations to back a budget of EUR 18.5 billion for 2023-2025. In September 2022, France announced its plans to increase spending on national and European space programs as the ESA works to secure commitments for its own significant budget increase. The government announced its plans to allocate more than USD 9 billion to space activities, an increase of about 25% over the past three years.

Europe Satellite Bus Industry Overview

The Europe Satellite Bus Market is fairly consolidated, with the top five companies occupying 71%. The major players in this market are Airbus SE, Honeywell International Inc., Lockheed Martin Corporation, Northrop Grumman Corporation and Thales (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Satellite Mass

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 France

- 4.4.2 Germany

- 4.4.3 Russia

- 4.4.4 United Kingdom

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Satellite Mass

- 5.2.1 10-100kg

- 5.2.2 100-500kg

- 5.2.3 500-1000kg

- 5.2.4 Below 10 Kg

- 5.2.5 above 1000kg

- 5.3 Orbit Class

- 5.3.1 GEO

- 5.3.2 LEO

- 5.3.3 MEO

- 5.4 End User

- 5.4.1 Commercial

- 5.4.2 Military & Government

- 5.4.3 Other

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Airbus SE

- 6.4.2 Ball Corporation

- 6.4.3 Honeywell International Inc.

- 6.4.4 Lockheed Martin Corporation

- 6.4.5 Nano Avionics

- 6.4.6 NEC

- 6.4.7 Northrop Grumman Corporation

- 6.4.8 OHB SE

- 6.4.9 Sierra Nevada Corporation

- 6.4.10 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

欧州の衛星バス市場:シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 171 Pages

- 納期

- 2~3営業日