欧州の非乳製品ミルク:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Europe Non-Dairy Milk - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 213 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693873

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

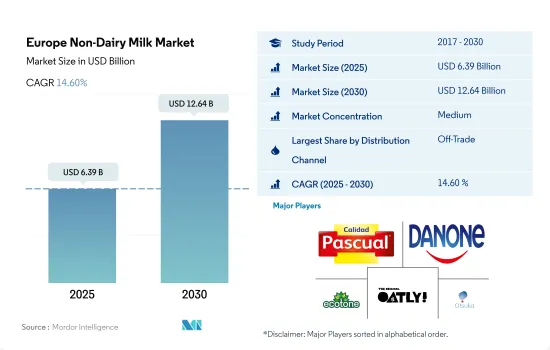

欧州の非乳製品ミルク市場規模は2025年に63億9,000万米ドルと推定・予測され、2030年には126億4,000万米ドルに達し、予測期間(2025~2030年)のCAGRは14.60%で成長すると予測されます。

幅広い小売部門を通じて植物性ミルクを容易に入手できることが成長を後押ししています。

- 植物性ミルクは、牛乳の感覚と栄養価を再現しようとする成分の多様化と製品開発の主要進展に支えられ、牛乳カテゴリーのイノベーションリーダーとなっています。流通チャネル全体を通じた植物性乳の販売額は、2026年には2022年から70.3%成長すると予測されます。

- 流通チャネル全体の中で、オフトレードセグメントが欧州の植物性ミルク市場の流通チャネルを支配しています。主にハイパーマーケットとスーパーマーケットが、オフチャネルの高い市場シェアを牽引しています。スーパーマーケットとハイパーマーケットにおける植物性ミルクの販売額は、2018~2022年にかけて72.57%の成長を記録しました。これらの小売チャネルは、提供されるブランドの幅広い品揃え、かなりの棚スペース、頻繁な価格プロモーションにより、強い地位を占めています。

- その他の植物性ミルクと比較すると、豆乳は非売品チャネルで最も消費されており、2022年の市場シェアは38.17%です。

- この地域ではオンチャネルの市場はそれほど大きくなく、まだ発展途上の段階にあります。消費者は自宅では植物性ミルクを好み、レストランや外食店で飲むことは少ないです。オンチャネルの2022年の金額シェアは、オフチャネルに比べて3%以下です。

- 欧州では、チーズや肉などの他の植物性製品に比べ、植物性代替ミルクの人気が高まっており、多くの消費者が豆乳、オートミール、アーモンド、ココナッツミルクなどの代替ミルクをすでに使いこなしています。ドイツでは、消費者の93%がすでに植物性代替ミルクを購入しており、これは他のどの植物性製品カテゴリーよりも高いです。

ドイツはこの地域の植物性ミルク消費において主要な役割を果たしています。

- 欧州の植物性ミルクは、2022年には前年の2021年と比較して14.1%の成長を記録しました。この成長は、多くの消費者が植物性製品の健康と持続可能性の利点に惹かれていることに起因しています。植物性飲料はまた、乳製品ベースの牛乳よりも保存期間が長いという利点も主張しています。牛乳の賞味期限は通常4~7日だが、植物性ミルクは常温で最長10日です。

- 国別では、ドイツがこの地域の植物性ミルク市場をリードしており、2024年には2021年比で77.6%の成長が見込まれています。他の植物性製品に比べ、同国では多くの消費者が代替ミルクに慣れ親しんでいます。牛乳は同国で最も好まれる植物性製品であり、93%の消費者がすでに購入しています。2021年には、ドイツの消費者の75%が従来の牛乳の代替品としてオートミルクを、69.4%がアーモンドミルクを、ほぼ51%が豆乳を消費しています。同国では牛乳が最も好まれる植物性製品で、消費率は93%です。

- スペインは、この地域で植物性ミルクが2番目に多い市場です。スペインでは、菜食主義者の数が増加しており、人口の半数以上がフレキシタリアンと考えて肉の消費を減らしたいと考えています。2022年現在、スペインの消費者の30%がフレキシタリアンであり、6%が植物性食生活を実践しています。スペインにおける植物性乳の総販売額は、2021年の6億5,070万米ドルから2022年には7億640万米ドルへと約8.6%増加しました。他の植物性ミルクと比較して、豆乳はスペインで主に消費されています。2022年には豆乳が金額シェアで31.5%を占めました。

欧州の非乳製品乳市場の動向

植物性乳製品がもたらす健康上の利点により消費量が増加

- 欧州における植物性乳の消費は増加傾向にあります。特に毎日の食事に従来の牛乳の代わりにオートミールを取り入れることが増えており、欧州全域で消費パターンが強化されています。チーズや肉などの他の植物性製品と比較して、植物性ミルクは同地域の植物性食品市場をリードしています。欧州の植物性ミルク市場は、2023年には66.8%のシェアを占めると予想されています。多くの消費者が豆乳やココナッツミルクのような代替ミルクに親しんでいます。ドイツでは、消費者の93%が植物性ミルクを消費しており、これは他のどの植物性製品カテゴリーよりも高いです。

- 植物性ミルクの人気は過去10年間で高まっています。このような飲み物は、さまざまな文化圏で何世紀にもわたって飲まれてきました。スペインでは、ホルチャータ・デ・チュファとして知られるタイガーナッツ・ミルクが国民的な飲み物として人気があります。植物性ミルクは家庭の主食となり、もはやヴィーガンやベジタリアンだけが飲むものではないです。欧州の消費者の54%近くが植物性ミルクを好み、43%が乳製品や乳製品代替品を購入しています。

- 植物性乳の国内需要は予測期間中一定と予想されます。これは主食としての植物性ミルクの消費が伸びているためです。植物性ミルクの一人当たり消費量は、2024~2027年の間に44%増加すると予測されます。欧州諸国の大都市は植物性消費者の基盤が強いが、植物性タンパク質消費への緩やかなシフトは予測期間中に他の地域にも広がると予想されます。2022年には英国の消費者の約60%が植物性タンパク質に関心を持っていました。

欧州の非乳製品ミルク産業概要

欧州の非乳製品ミルク市場は適度に統合されており、上位5社で43.66%を占めています。この市場の主要企業は、Calidad Pascual SAU、Danone SA、Ecotone、Oatly Group AB、Otsuka Holdingsなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原料/商品生産

- 代替乳製品-原料生産

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 製品タイプ

- アーモンドミルク

- カシューミルク

- ココナッツミルク

- ヘーゼルナッツミルク

- ヘンプミルク

- オートミルク

- 豆乳

- 流通チャネル

- オフトレード

- サブ流通チャネル別

- コンビニエンスストア

- オンライン小売

- 専門店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

- 国名

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Calidad Pascual SAU

- Califia Farms LLC

- Danone SA

- Ecotone

- International Food SRL

- Minor Figures Limited

- Oatly Group AB

- Otsuka Holdings Co. Ltd

- The Hain Celestial Group Inc.

- Valsoia SpA

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50000739

The Europe Non-Dairy Milk Market size is estimated at 6.39 billion USD in 2025, and is expected to reach 12.64 billion USD by 2030, growing at a CAGR of 14.60% during the forecast period (2025-2030).

Easy availability of plant-based milk through wide retail sector is boosting the growth

- Plant-based milk is the innovation leader in the milk category, supported by key advancements in ingredient diversification and product development that seek to replicate the sensory experience and nutritional value of cow's milk. The sales value of plant-based milk through the overall distribution channel is anticipated to grow by 70.3% in 2026 from 2022.

- Among overall distribution channels, the off-trade segment dominates the distribution channels of the Europe plant-based milk market. Hypermarkets and supermarkets primarily drive the high market share of off-trade channels. The sales value of plant-based milk in supermarkets and hypermarkets registered a growth of 72.57% from 2018 to 2022. These retail channels have a strong position due to the wide selection of brands offered, considerable shelf space, and frequent price promotions.

- Compared to other plant-based milk, soy milk is the most consumed through off-trade channels, with a market share of 38.17% in 2022.

- The region does not have a considerable market for the on-trade channels and is at a nascent stage. Consumers prefer plant-based milk at home and are less likely to drink from a restaurant or food service outlet. On-trade channels acquired less than 3% of the value share in 2022 compared to off-trade channels.

- In Europe, plant-based milk alternatives have been gaining popularity compared to other plant-based products, such as cheese and meat, and many consumers are already familiar with milk alternatives like soy, oat, almond, and coconut milk. In Germany, 93% of consumers already buy plant-based milk alternatives, which is higher than in any other plant-based product category.

Germany plays a major role in the consumption of plant-based milk in the region

- The plant-based milk in the Europe region witnessed a growth of 14.1% in 2022 compared to the previous year, 2021. The growth is attributed to many consumers drawn toward the health and sustainability benefits of plant-based products. Plant-based beverages also claim other advantages, as they have a longer shelf life than dairy-based milk. Cow's milk usually lasts four to seven days, but plant-based milk lasts up to 10 days at room temperature.

- By country, Germany is the leading market for plant-based milk in the region, and it is anticipated to grow by 77.6% in 2024 compared to the year 2021. Compared to other plant-based products, many consumers in the country are familiar with milk alternatives. Milk is the most preferred plant-based product in the country, with 93% of consumers buying it already. In 2021, 75% of consumers in Germany consumed oat milk as their go-to alternative to conventional milk, 69.4% consumed almond milk, and almost 51% consumed soy milk. Milk is the most preferred plant-based product in the country, with a consumption rate of 93%.

- Spain is the second-leading market for plant-based milk in the region. In Spain, the number of vegans is growing, and more than half of the population wants to reduce meat consumption, considering themselves flexitarian. As of 2022, 30% of Spanish consumers identify as flexitarian, while 6% follow a plant-based diet. The total sales value of plant-based milk in Spain reported an increase from USD 650.7 million in 2021 to USD 706.4 million in 2022, which represented an increase of approximately 8.6%. Compared to other plant-based milk, soy milk is majorly consumed in Spain. In 2022, soy milk accounted for 31.5% of the value share.

Europe Non-Dairy Milk Market Trends

The consumption of plant-based milk products increased due to the health benefits they offer

- The consumption of plant milk in Europe is on the rise. The increasing inclusion of oat milk instead of conventional milk, especially in the daily diet, is strengthening consumption patterns across Europe. Compared to other plant-based products such as cheese and meat, plant-based milk leads the plant-based food market in the region. The European plant-based milk market is expected to hold a share of 66.8% in 2023. Many consumers are familiar with milk alternatives like soy and coconut milk. In Germany, 93% of consumers consume plant-based milk, which is higher than in any of the other plant-based product categories.

- The popularity of plant milk has increased over the past decade. Drinks like these have been consumed for centuries in various cultures. In Spain, tiger nut milk, known as horchata de chufa, is a popular national drink. Plant milk has become a household staple and is no longer consumed exclusively by vegans and vegetarians. Nearly 54% of European consumers prefer plant-based milk, and 43% purchase dairy and dairy alternatives.

- The domestic demand for plant-based milk is expected to be constant during the forecast period. This is due to the growing consumption of plant milk as a staple product. The per capita consumption of plant milk is anticipated to rise by 44% during 2024-2027. Bigger cities in European countries have strong plant-based consumer bases, but a gradual shift toward plant-based protein consumption is expected to spread to other parts of countries during the forecast period. Around 60% of UK consumers were interested in plant-based proteins in 2022.

Europe Non-Dairy Milk Industry Overview

The Europe Non-Dairy Milk Market is moderately consolidated, with the top five companies occupying 43.66%. The major players in this market are Calidad Pascual SAU, Danone SA, Ecotone, Oatly Group AB and Otsuka Holdings Co. Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Dairy Alternative - Raw Material Production

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product Type

- 5.1.1 Almond Milk

- 5.1.2 Cashew Milk

- 5.1.3 Coconut Milk

- 5.1.4 Hazelnut Milk

- 5.1.5 Hemp Milk

- 5.1.6 Oat Milk

- 5.1.7 Soy Milk

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 By Sub Distribution Channels

- 5.2.1.1.1 Convenience Stores

- 5.2.1.1.2 Online Retail

- 5.2.1.1.3 Specialist Retailers

- 5.2.1.1.4 Supermarkets and Hypermarkets

- 5.2.1.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

- 5.3 Country

- 5.3.1 Belgium

- 5.3.2 France

- 5.3.3 Germany

- 5.3.4 Italy

- 5.3.5 Netherlands

- 5.3.6 Russia

- 5.3.7 Spain

- 5.3.8 Turkey

- 5.3.9 United Kingdom

- 5.3.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Calidad Pascual SAU

- 6.4.2 Califia Farms LLC

- 6.4.3 Danone SA

- 6.4.4 Ecotone

- 6.4.5 International Food SRL

- 6.4.6 Minor Figures Limited

- 6.4.7 Oatly Group AB

- 6.4.8 Otsuka Holdings Co. Ltd

- 6.4.9 The Hain Celestial Group Inc.

- 6.4.10 Valsoia SpA

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

欧州の非乳製品ミルク:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 213 Pages

- 納期

- 2~3営業日