北米の非乳製品牛乳:市場シェア分析、産業動向、成長予測(2025~2030年)

North America Non-Dairy Milk - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 182 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693870

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

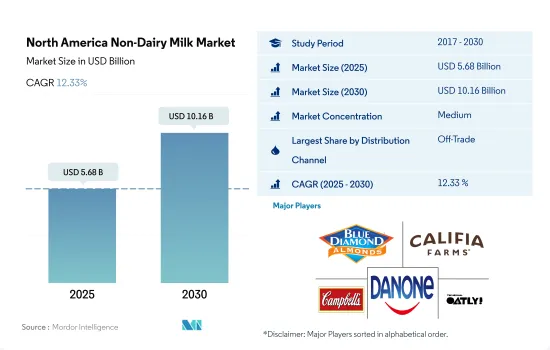

北米の非乳製品牛乳市場規模は2025年に56億8,000万米ドルと推定・予測され、2030年には101億6,000万米ドルに達し、予測期間(2025~2030年)のCAGRは12.33%で成長すると予測されます。

ハイパーマーケットやオンラインストアを含む近代的な食料品小売の台頭が、商取引外のチャネルを通じた販売を促進

- 主にハイパーマーケットとスーパーマーケットが、商取引外チャネルの高い市場シェアを牽引しています。スーパーマーケットとハイパーマーケットは、植物性乳の販売において常に市場をリードしてきました。これらのチャネルは、特に大都市や市場において、消費者が市場で入手可能な多種多様な製品の中から購入を決定する際に影響を与えるという付加的な利点を提供しています。米国では、スーパーマーケットとハイパーマーケットが2022年の植物性乳販売の73.97%(金額ベース)を占めています。

- コンビニエンスストアは、植物性ミルクを購入するためにスーパーマーケットとハイパーマーケットに次いで広く好まれている商業外流通チャネルです。このセグメントは2022年に数量ベースで12.19%の市場シェアを獲得します。プライベートブランドへの幅広いリーチと容易なアクセスが、消費者が他の小売チャネルよりも伝統的食料品店を好む原動力となっています。

- 北米のオンラインチャネルは、植物性ミルクの流通チャネルとして最も急速に成長すると予測されています。このセグメントは2017~2022年に金額で81.93%の成長を記録しました。カナダでは、植物性ミルクのオンライン販売は予測期間中に15.09%のCAGRを記録し、2029年末には市場規模2,378万米ドルに達すると予測されています。

- オンラインセグメントにおける市場の成長は、カナダの消費者の購買行動の変化に対応して、最新の食料品店がオンラインデリバリーインフラへの投資を増やしていることに起因しています。2021年には、カナダ人の約22%が食料品を定期的にオンラインで購入しています。調査対象市場における著名なオンライン小売業者には、Instacart、Amazon Fresh、Walmart、Kroger、Shipt、Thrive Market、Whole Foods、FreshDirectが含まれます。

米国消費者のヴィーガンライフスタイルの採用が植物性ミルクの消費を促進

- 健康的なライフスタイルの一部としてベジタリアン食の重要性が高まっているため、米国では植物性ミルクが広く受け入れられています。米国の成人の約68%が代替乳製品や植物性食肉を試したことがあります。また、調査によると、回答者の約34%が環境への影響を減らすために菜食主義者のライフスタイルを採用することに関心を持っています。そのため、米国はこの地域の主要市場として認識されており、2017~2022年にかけての消費量は32.57%の成長を記録しています。

- カナダの植物性ミルク市場は、2023~2029年にかけてCAGR 9.76%を記録し、2023年末には292,898.79トンの市場規模に達すると予測されています。市場の成長は主に菜食主義者の増加に起因します。2021年、カナダにおける植物由来のレディミールの小売売上は、フリーフロムレディミール全体の17%のシェアを占めました。ヴィーガン食品の流通を専門とする小売パートナーの増加もカナダ市場の成長を促進する重要な要因です。小売業者には、Compass Foods、Instacart、Well.ca、Avron、Walmart、Amazonなどがあります。Well.caは、Califia、Chobani、Blue Diamond、Earth's Ownといった様々なブランドの代替乳製品を提供しています。

- 消費者が無糖または減糖を特徴とするヘルシーな代替品にシフトしているため、無糖植物性ミルクの需要は予測期間中に増加すると予想されます。例えば、米国の成人の10人中8人は意図的に食事中の砂糖を避けたり減らしたりしており、16%は砂糖を減らすことが最も重要であると回答しています。無糖植物性ミルクを専門とする主要ブランドは、Silk、Califia、Planet Oat、Orgain、Elmhurstです。

北米の非乳製品ミルク市場動向

植物性乳製品の有益な要素は、環境意識の高い消費者からの影響が大きく、北米での消費を牽引しています。

- 植物性ミルクは北米市場で高い関心を集めており、その利点に関する認識と実証が高まっています。利用可能なすべての植物性ミルクの中で、アーモンドミルクは2021年に主要な代替ミルクのタイプでした。その年のアーモンドミルクは約3億4,400万米ドルと評価されました。消費者の好意的な割合は、身体、環境、動物福祉にとってより良い製品へのシフトを望んでおり、食生活の必要性から植物由来のソースに移行しています。非乳製品牛乳は現在、米国の主要食料品店やコーヒーチェーンの棚に、適切な代用品として並んでいます。

- 米国では、成人の67%が非乳製品牛乳を試したことがあり、約3人に1人が少なくとも週に1回は摂取しています。また、代替ミルクを摂取する人の82%は風味が好きだからであり、56%は環境に配慮しています。豆乳やオートミールのような製品は、北米市場で非乳製品飲料がゆっくりと着実に急増し始めてからほぼ10年経った現在、アメリカの家庭で従来の牛乳の一部品種とほぼ同じくらい普及しています。

- 植物性乳や従来型乳のメーカーを含む市場の参入企業が、さまざまな選択肢を強調し始めたため、冷蔵庫のスペースをめぐる競争は激化しています。こうしたソリューションには、環境意識の高い顧客にサービスを提供する食品技術産業の企業も含まれます。2020年、世界の植物性ミルクの小売販売額は32億米ドル近くに達します。栄養密度、腸の健康、(農薬による)毒性の低減、動物福祉、消化性などの要素により、市場は今後数年間で好影響を確認すると予測されます。

北米の非乳製品牛乳産業概要

北米の非乳製品牛乳市場は適度に統合されており、上位5社で47.97%を占めています。この市場の主要企業は、Blue Diamond Growers、Califia Farms LLC、Campbell Soup Company、Danone SA、Oatly Group ABなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原料/商品生産

- 代替乳製品-原料生産

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 製品タイプ

- アーモンドミルク

- カシューミルク

- ココナッツミルク

- ヘンプミルク

- オートミルク

- 豆乳

- 流通チャネル

- オフトレード

- サブ流通チャネル別

- コンビニエンスストア

- オンライン小売

- 専門店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Blue Diamond Growers

- Califia Farms LLC

- Campbell Soup Company

- Danone SA

- Elmhurst Milked LLC

- Laird Superfood LLC

- Oatly Group AB

- The Hain Celestial Group Inc.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50000730

The North America Non-Dairy Milk Market size is estimated at 5.68 billion USD in 2025, and is expected to reach 10.16 billion USD by 2030, growing at a CAGR of 12.33% during the forecast period (2025-2030).

Rise in modern grocery retailing including hypermarkets and online stores fuels the sales through off-trade channels

- Hypermarkets and supermarkets primarily drive the high market share of off-trade channels. Supermarkets and hypermarkets have always maintained a strong lead in plant-based milk sales in the market. The proximity factor of these channels, especially in large and developed cities, provides an added advantage of influencing the consumer's decision to purchase among the large variety of products available in the market. In the United States, supermarkets and hypermarkets covered 73.97% of plant-based milk sales, in terms of value, in 2022.

- Convenience stores are the second most widely preferred off-trade distribution channel after supermarkets and hypermarkets to purchase plant-based milk. The segment acquired a 12.19% market share, in terms of volume, in 2022. The broader reach and easy access to private label brands drive the consumer preference for traditional grocery stores over other retail channels.

- The online channel in North America is projected to be the fastest-growing distribution channel for plant-based milk. The segment registered a growth of 81.93% in value from 2017-2022. In Canada, the online sales of plant-based milk are anticipated to register a CAGR of 15.09% during the forecast period to reach a market value of USD 23.78 million by the end of 2029.

- The market's growth in the online segment is attributed to the increasing investments by modern grocery stores in the online delivery infrastructure in response to the changing purchasing behavior of Canadian consumers. Almost 22% of Canadians regularly purchased groceries online in 2021. Prominent online retailers in the market studied include Instacart, Amazon Fresh, Walmart, Kroger, Shipt, Thrive Market, Whole Foods, and FreshDirect.

Adoption of vegan lifestyles among U.S. consumers propels the consumption of plant-based milk

- Plant-based milk is gaining significant acceptance among the US population due to the rising importance of vegetarian diets as a part of healthy lifestyles. Around 68% of US adults have tried a dairy alternative or plant-based meat. Surveys also report that around 34% of respondents are interested in adopting vegan lifestyles to reduce environmental impacts. Therefore, the United States is identified as the major market in the region, with a volume consumption registered growth of 32.57% from 2017-2022.

- The Canadian plant-based milk market is anticipated to register a CAGR of 9.76% during 2023-2029 to reach a market volume of 292,898.79 tonnes by the end of 2023. The market's growth is primarily attributed to the rise in the vegan population. In 2021, retail sales of plant-based ready meals in Canada represented a share of 17% of total free-from-ready meal sales. The growing number of retail partners specializing in vegan food distribution is another key factor driving the growth in the Canadian market. Some retailers include Compass Foods, Instacart, Well.ca, Avron, Walmart, and Amazon. Well.ca offers dairy alternatives of different brands such as Califia, Chobani, Blue Diamond, and Earth's Own.

- As consumers are shifting toward healthy variants featuring no or reduced sugar, the demand for unsweetened plant milk is expected to increase during the forecast period. For instance, eight out of every 10 US adults intentionally avoid or reduce sugar in their diets, with 16% stating that it is the most important thing they are trying to reduce. Key brands specializing in unsweetened plant milk are Silk, Califia, Planet Oat, Orgain, and Elmhurst.

North America Non-Dairy Milk Market Trends

The beneficial factors of plant-based milk products, with a larger impact from environment-conscious consumers, drive consumption in North America.

- Plant-based milk is highly gaining interest in the North American market, as the awareness and proof regarding their benefits are rising in the region. Among all the available plant-based milk, almond milk was the leading type of milk alternative in the United States in 2021. For that year, almond milk was valued at approximately USD 344 million. A favorable proportion of consumers are willing to shift to better products for their bodies, the environment, and animal welfare and move to plant-based sources for their dietary needs. Non-dairy milk is now available as a suitable substitute on the shelves of major grocery and coffee chains in the United States.

- In the United States, 67% of adults have tried non-dairy milk, and about 1 in 3 consume it at least once a week. In addition, 82% of those who consume alternative milk do so because they like the flavor, while 56% are environmentally conscious. Products like soy milk and oat milk are now almost as widespread in American households as some varieties of conventional cow's milk, almost a decade after non-dairy beverages began their slow and steady surge in the North American market.

- The competition for refrigerator space has intensified as players in the market, including manufacturers of plant-based and conventional milk, have begun to highlight various options on the horizon. These solutions include companies in the food technology industry that serve environmentally conscious customers. In 2020, the region's retail sales value of plant-based milk in the world amounted to nearly USD 3.20 billion. With factors like nutritional density, gut health, reduced toxicity (from pesticides), animal welfare, and digestibility, the market is projected to witness a positive impact in the upcoming years.

North America Non-Dairy Milk Industry Overview

The North America Non-Dairy Milk Market is moderately consolidated, with the top five companies occupying 47.97%. The major players in this market are Blue Diamond Growers, Califia Farms LLC, Campbell Soup Company, Danone SA and Oatly Group AB (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Dairy Alternative - Raw Material Production

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product Type

- 5.1.1 Almond Milk

- 5.1.2 Cashew Milk

- 5.1.3 Coconut Milk

- 5.1.4 Hemp Milk

- 5.1.5 Oat Milk

- 5.1.6 Soy Milk

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 By Sub Distribution Channels

- 5.2.1.1.1 Convenience Stores

- 5.2.1.1.2 Online Retail

- 5.2.1.1.3 Specialist Retailers

- 5.2.1.1.4 Supermarkets and Hypermarkets

- 5.2.1.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Blue Diamond Growers

- 6.4.2 Califia Farms LLC

- 6.4.3 Campbell Soup Company

- 6.4.4 Danone SA

- 6.4.5 Elmhurst Milked LLC

- 6.4.6 Laird Superfood LLC

- 6.4.7 Oatly Group AB

- 6.4.8 The Hain Celestial Group Inc.

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

北米の非乳製品牛乳:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 182 Pages

- 納期

- 2~3営業日