アジア太平洋の非乳製品牛乳:市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia-Pacific Non-Dairy Milk - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 215 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693858

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

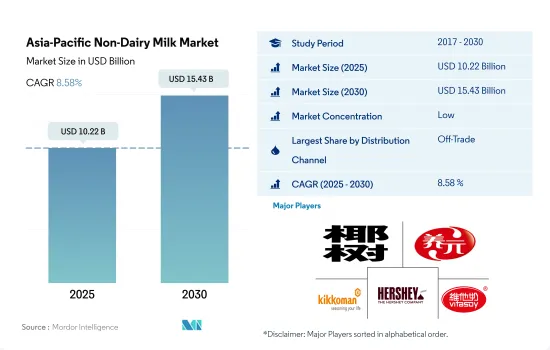

アジア太平洋の非乳製品牛乳市場規模は、2025年に102億2,000万米ドルと推定され、2030年には154億3,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは8.58%で成長すると予測されます。

組織小売チャネルの強力な浸透が市場成長を促進

- 2017~2022年にかけて、アジア太平洋の小売市場は、非商業的小売が支配的でした。2022年には、商業外小売が93.64%のシェアを占めています。この地域の消費者は、植物性ミルクを購入する際の利便性の高さから、取引外小売に強く惹かれています。

- 2022年のアジア太平洋におけるオントレード小売のシェアは6.36%でした。クイックサービスレストランのようなオンチャネルでは、植物性ミルクの価格は固定されているが、消費者はオフチャネルでいくつかの選択肢を持っています。アジア太平洋では、オフチャネルは植物性ミルクを低価格から中価格、高価格まで様々な価格で提供しています。例えば、これらの小売業者が販売するオートミルクは255インドルピーから764インドルピーまです。さまざまな価格帯の植物性ミルクが入手可能であることは、消費者の購買力を促進します。

- アジア太平洋では、小売業者は無糖、チョコレート、バニラなど、さまざまな風味の植物性ミルクを提供することに注力しています。しかし、これらの小売業者は、使用されている原料や使用されている種子のタイプなど、製品仕様に関する完全な情報を提供していない場合があります。その結果、消費者は植物由来のミルク飲料を商取引外の方法で購入することを好みます。

- 過去3年間(2020~2023年)において、専門店は消費者により高い商品認知度を提供するため、取引外モードにおいて大きな需要を経験しています。植物性ミルクに対する需要の高まりを考慮すると、この地域の流通セグメント全体は2022年と比較して2025年には9.78%の成長が見込まれます。

政府の支援、ヴィーガニュアリーキャンペーン、植物性ミルクをメニューに導入する外食産業やカフェなど数多くの要因が市場拡大に拍車をかけています。

- アジア太平洋市場は、2019~2023年にかけて植物性ミルクの販売額が全体として9%の成長率を記録しました。植物性ミルクは、同地域の乳製品代替市場の大部分を占めています。中国、日本、韓国は植物性ミルクの主要消費国です。2023年には、これら3カ国の合計がこの地域の植物性ミルク消費全体の74%のシェアを占めています。韓国では、消費者の約74%が植物性ミルクを選択し、27%が他の代替乳製品を消費しています。

- 2022年、インドはVeganuaryキャンペーンへの参加者数が世界で3番目に多く、約6万人が参加しました。これは、同国における植物性代替食品への関心の高まりを浮き彫りにしています。オーストラリアでは、2022年に1人当たり1週間に約半量の代用乳が消費されました。

- アジア太平洋のベジタリアンやヴィーガンは、天然の乳製品を使ったミルクと比較して、植物由来の代替ミルクが人間の栄養と健康にもたらす利点を積極的に宣伝しています。さらに、この地域の政府は乳製品代替企業に投資しています。例えば、2022年にニュージーランド政府は、サウスランドを拠点とするオートミールミルク製造会社、ニュージーランド・ファンクショナル・フーズを支援するために600万米ドルを拠出しました。

- 飲食店やコーヒーショップは、消費者の需要を満たすため、植物由来の商品を仕入れています。900以上の店舗を持つインド最大のコーヒーチェーン、カフェ・コーヒー・デイは、2022年に様々な植物性飲料の提供を開始し、同地域のオントレード販売を牽引しています。韓国では、スターバックスでオートミルクをメニューに導入した結果、最初の1ヵ月だけで20万本以上のオートミルク飲料が販売されました。同地域では2024~2027年の間に、オンチャネルを通じた植物性ミルクの売上が11%成長すると予想されています。

アジア太平洋の非乳製品ミルク市場動向

この地域におけるヴィーガン人口の増加と牛乳アレルギーの増加が、この地域における植物性ミルク消費を支えています。

- アジア太平洋では、ヴィーガン人口の増加により、ここ数年、さまざまな種類の植物性ミルクの消費が増加しています。各国でヴィーガンの展示会/見本市や音楽祭が開催されるほどです。例えば、オーストラリアは国民一人当たりの菜食主義者の割合が世界で3番目に高いです。2022年現在、同国には250万人のヴィーガンとベジタリアンがいます。この地域にはヴィーガンの有名人、特に有名シェフが何人もおり、植物由来のライフスタイルを食卓や食文化の主流にする上で重要な役割を果たしています。そのため、従来の牛乳に代わって豆乳を毎日の食事に取り入れる人が増え、地域全体の消費パターンが強化されています。

- 代替乳製品の中では、豆乳やアーモンドミルクのような植物性ミルクが、2022年には地域全体で大半のシェアを占めています。乳製品代替ミルクの消費量では、中国がこの地域の主要国です。植物性ミルクの中でも、大豆飲料は、大豆消費の長年の伝統と広く入手可能なことから、中国では伝統的に最も人気があります。

- 消費者、特に牛乳アレルギーのある消費者は、植物性乳製品の摂取に熱心です。牛乳アレルギーは、幼児によく見られる食物アレルギーのひとつです。日本の消費者の多くは乳糖不耐症で、牛乳や乳製品を摂取しないです。2022年現在、オーストラリアでは、乳幼児の約50人に1人が牛乳アレルギーの兆候を示しています。また、消費者の45%が動物性食品の摂取を積極的に減らそうとしています。したがって、オーストラリアにおける植物性ミルクの一人当たり消費量は、2022~2023年にかけて4.74%増加すると推定されます。

アジア太平洋の非乳製品牛乳産業概要

アジア太平洋の非乳製品牛乳市場はセグメント化されており、上位5社で38.79%を占めています。この市場の主要企業は、Coconut Palm Group、Hebei Yangyuan Zhihui Beverage、Kikkoman Corporation、The Hershey Company、Vitasoy International Holdings Ltdなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たりの消費量

- 原料/商品生産

- 代替乳製品-原料生産

- 規制の枠組み

- オーストラリア

- 中国

- インド

- 日本

- 韓国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 製品タイプ

- アーモンドミルク

- カシューミルク

- ココナッツミルク

- ヘーゼルナッツミルク

- ヘンプミルク

- オートミルク

- 豆乳

- 流通チャネル

- オフトレード

- サブ流通チャネル別

- コンビニエンスストア

- オンライン小売

- 専門店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- ニュージーランド

- パキスタン

- 韓国

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Blue Diamond Growers

- Bonsoy Beverage Co.

- Coconut Palm Group Co. Ltd

- Hebei Yangyuan Zhihui Beverage Co. Ltd

- Kikkoman Corporation

- Marusan-AI Co. Ltd

- Noumi Ltd

- Oatly Group AB

- The Hershey Company

- Vitasoy International Holdings Ltd

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The Asia-Pacific Non-Dairy Milk Market size is estimated at 10.22 billion USD in 2025, and is expected to reach 15.43 billion USD by 2030, growing at a CAGR of 8.58% during the forecast period (2025-2030).

Strong penetration of organized retail channels fueling the market growth

- From 2017 to 2022, off-trade retailing dominated the retail space in the Asia-Pacific region. In 2022, off-trade retailing held a share of 93.64%. Consumers in this region are highly fascinated by off-trade retailing due to the greater convenience it offers when purchasing plant-based milk.

- On-trade retailing accounted for a share of 6.36% in Asia-Pacific in 2022. In on-trade channels, such as quick-service restaurants, the prices for plant-based milk are fixed, while consumers have several options in off-trade channels. In the Asia-Pacific region, off-trade channels offer plant-based milk at varied prices, ranging from low to medium and high. For example, oat milk sold by these retailing units is available from INR 255 to as high as INR 764. The availability of plant-based milk at different price points also promotes consumer buying power, as they can choose products that suit their affordability parameters.

- In the Asia-Pacific region, on-trade retailers focus on providing a variety of plant-based milk, including different flavors such as unsweetened, chocolate, vanilla, etc. However, these retailers may not provide complete information about product specifics, such as ingredients used or the type of seeds used. As a result, consumers prefer purchasing their plant-based milk beverages through off-trade modes.

- Over the past three years (2020-2023), specialty stores have experienced significant demand under the off-trade mode, as they offer higher visibility of the products to consumers. Considering the growing demand for plant-based milk, the overall distribution segment in the region is expected to grow by 9.78% in 2025 compared to 2022.

Numerous factors like government support, veganuary campaign, and food service, caffes introducing plant-based milk in their menu is fueling the market expansion

- The Asia-Pacific market witnessed an overall growth rate of 9% in the sales value of plant-based milk from 2019 to 2023. Plant-based milk holds a significant portion of the dairy alternative market in the region. China, Japan, and South Korea are the leading consumers of plant-based milk. In 2023, these three countries collectively accounted for a 74% share of the overall plant-based milk consumption in the region. In South Korea, approximately 74% of consumers opt for plant-based milk, while 27% consume other dairy alternatives.

- In 2022, India had the third-highest number of participants globally in the Veganuary campaign, with approximately 60,000 people joining. This highlights the growing interest in plant-based alternatives in the country. In Australia, each individual consumed around half a metric cup of milk substitutes per week in 2022.

- Vegetarians and vegans in the Asia-Pacific region actively promote the advantages of plant-based alternative milk for human nutrition and health compared to natural dairy milk. Additionally, governments in the region are investing in dairy alternative companies. For instance, in 2022, the New Zealand Government contributed USD 6 million to support New Zealand Functional Foods, a Southland-based oat milk producer.

- Eateries and coffee shops are stocking plant-based goods to meet consumer demand. Cafe Coffee Day, India's largest coffee chain with over 900 outlets, started offering a variety of plant-based beverages in 2022, driving on-trade sales in the region. In South Korea, the introduction of oat milk to the menu at Starbucks resulted in the sale of over 200,000 oat milk beverages in the first month alone. The sales of plant-based milk through on-trade channels are expected to grow by 11% during the period 2024-2027 in the region.

Asia-Pacific Non-Dairy Milk Market Trends

The increasing vegan population in the region, coupled with increasing milk allergies, is supporting the plant-based milk consumption in the region

- The consumption of different types of plant milk in Asia-Pacific has been on the rise for the past few years due to the growing vegan population. There are even vegan exhibitions/trade shows and music festivals conducted in different countries. For example, Australia has the third-highest percentage of vegans per capita globally. As of 2022, there are 2.5 million vegans and vegetarians' population in the country. Several vegan celebrities across the region, particularly celebrity chefs, have played a significant role in bringing plant-based lifestyles into the mainstream of dining and food culture. Thus, increasing the inclusion of soy milk in the daily diet, as it replaces conventional milk, strengthening the consumption patterns across the region.

- Among the dairy alternatives, plant-based milk like soy milk and almond milk had the majority share across the region in 2022. China is the leading country across the region in terms of consumption of dairy alternatives milk. Within plant-based milk, soy drinks have traditionally been the most popular in China due to the long-standing tradition of soy consumption and its wide availability.

- Consumers, especially those allergic to milk, are keen to consume plant-based milk products. Cow milk allergy is one of the common food allergies in young children. Many Japanese consumers are lactose intolerant and do not consume milk or milk products. As of 2022, in Australia, around 1 in 50 babies and young children showed signs of an allergy to cow's milk. Also, 45% of consumers are actively trying to reduce the number of animal products they consume. Thus, the per capita consumption of plant-based milk in Australia is estimated to increase by 4.74% in 2022-2023.

Asia-Pacific Non-Dairy Milk Industry Overview

The Asia-Pacific Non-Dairy Milk Market is fragmented, with the top five companies occupying 38.79%. The major players in this market are Coconut Palm Group Co. Ltd, Hebei Yangyuan Zhihui Beverage Co. Ltd, Kikkoman Corporation, The Hershey Company and Vitasoy International Holdings Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Dairy Alternative - Raw Material Production

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Japan

- 4.3.5 South Korea

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product Type

- 5.1.1 Almond Milk

- 5.1.2 Cashew Milk

- 5.1.3 Coconut Milk

- 5.1.4 Hazelnut Milk

- 5.1.5 Hemp Milk

- 5.1.6 Oat Milk

- 5.1.7 Soy Milk

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 By Sub Distribution Channels

- 5.2.1.1.1 Convenience Stores

- 5.2.1.1.2 Online Retail

- 5.2.1.1.3 Specialist Retailers

- 5.2.1.1.4 Supermarkets and Hypermarkets

- 5.2.1.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 New Zealand

- 5.3.8 Pakistan

- 5.3.9 South Korea

- 5.3.10 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Blue Diamond Growers

- 6.4.2 Bonsoy Beverage Co.

- 6.4.3 Coconut Palm Group Co. Ltd

- 6.4.4 Hebei Yangyuan Zhihui Beverage Co. Ltd

- 6.4.5 Kikkoman Corporation

- 6.4.6 Marusan-AI Co. Ltd

- 6.4.7 Noumi Ltd

- 6.4.8 Oatly Group AB

- 6.4.9 The Hershey Company

- 6.4.10 Vitasoy International Holdings Ltd

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 215 Pages

- 納期

- 2~3営業日