米国の非乳製品ミルク:市場シェア分析、産業動向、成長予測(2025年~2030年)

United States Non-Dairy Milk - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683835

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

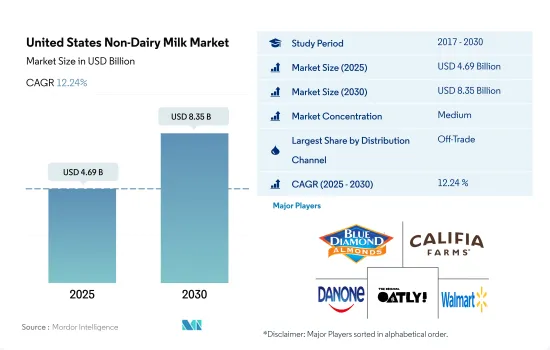

米国の非乳製品ミルク市場規模は2025年に46億9,000万米ドルと推定され、2030年には83億5,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは12.24%で成長する見込みです。

幅広い小売部門を通じて植物性ミルクを簡単に入手できることが成長を後押ししています。

- 米国では、小売チャネルにおける植物性ミルクの販売が大きな役割を果たしています。植物性ミルクは現在、牛乳の感覚と栄養価の両方を再現しようとする成分の多様化と製品開発における主な進歩に支えられ、牛乳カテゴリーのイノベーションリーダーとしての役割を果たしています。2022年、流通チャネル全体における植物性乳の販売額は2021年から8.1%増加しました。

- 2021年、小売チャネルにおける植物性乳の販売額は牛乳の3倍に増加し、牛乳の成長率が9%である2020年から27%の伸びを示しました。同年、42%の世帯が植物性ミルクを購入し、植物性ミルク購入者の76%が小売チャネルで複数回購入しています。この成長は、抗生物質やホルモン剤などの動物性食品に関連するリスクのため、動物性食品の摂取を控えたいと考える米国の買い物客に支えられています。

- 米国における植物性製品全体の中で、植物性牛乳の売上は増加しています。米国の植物性ミルク市場の流通チャネルは、非売品セグメントが支配的です。オフ・トレード部門では、スーパーマーケットとハイパーマーケットが大きなシェアを占めています。2022年には、スーパーマーケットとハイパーマーケットが金額ベースで80.9%のシェアを占めました。

- オン・トレード・チャネルは米国の植物性ミルク市場で最も急成長しているセグメントであり、2021年から2024年には21.2%の成長率で増加すると予測されています。米国の多くの大手レストランが、特にカクテル、スムージー、コーヒー、エスプレッソベースの飲料の原料オプションとして植物性ミルクを使用しています。2022年、米国には60万以上のレストランがありました。

米国の非乳製品ミルク市場の動向

乳糖不耐症の増加、ヘルシー志向の高まり、持続可能な原料調達が植物性ミルク市場を後押し

- 米国では、企業による投資とイノベーションに支えられ、一人当たりの植物性乳消費量が大幅に増加しています。米国の消費者の52%以上が植物性食品を好んでいます。多くのアメリカ人は、一般的に乳製品やその他の動物性食品の摂取量が少なく、ビーガンやベジタリアンに比べ、よりフレキシタリアンである傾向があります。2022年現在、米国の消費者の7%がフレキシタリアンであるのに対し、植物性食品を好む消費者は12%を超えています。あらゆる年代のアメリカ人が植物性食品に関心を持っているが、20代と30代が最も関心を持っています。

- アメリカ人の半数近く(47%)が植物性ミルクを定期的に摂取しており、ミレニアル世代とジェネレーションXの年齢層では56%に増加しています。乳糖不耐症の増加、健康的な食品への嗜好の高まり、持続可能な原料調達といった要因が、植物性ミルク市場の大きな成長をもたらしました。米国では、ジェネレーションZの40%、ミレニアル世代の38%、ジェネレーションXの34%、ベビーブーマーとシニアの21%が、持続可能な原料調達のために植物性ミルクを消費しています。

- 政府による支援も、米国における植物性乳製品の生産と消費を後押しする要因のひとつです。米国政府は植物性食品を重要な成長産業と位置づけています。米国の植物性食品企業は2021年に50億米ドルの資金を獲得し、2020年から60%増加しました。代替産業で最も成熟した部分である植物ベースの代替品部門は、2021年に19億米ドルの投資を確保し、2019年に調達した6億9,300万米ドルのほぼ3倍となりました。

米国の非乳製品ミルク産業の概要

米国の非乳製品ミルク市場は適度に統合されており、上位5社で48.59%を占めています。この市場の主要企業は以下の通り。 Blue Diamond Growers, Califia Farms LLC, Danone SA, Oatly Group AB and Walmart Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原材料/商品生産

- 代替乳製品-原材料生産

- 規制の枠組み

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 製品タイプ

- アーモンドミルク

- カシューミルク

- ココナッツミルク

- ヘンプミルク

- オートミルク

- 豆乳

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- 専門小売店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オン・トレード

- オフトレード

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)。

- Blue Diamond Growers

- Califia Farms LLC

- Campbell Soup Company

- Danone SA

- Oatly Group AB

- Otsuka Holdings Co. Ltd

- Ripple Foods PBC

- SunOpta Inc.

- Walmart Inc.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50000720

The United States Non-Dairy Milk Market size is estimated at 4.69 billion USD in 2025, and is expected to reach 8.35 billion USD by 2030, growing at a CAGR of 12.24% during the forecast period (2025-2030).

Availability of plant-based milk easily through wide retail sector is boosting the growth

- The sales of plant-based milk in retail channels play a major in the United States. Plant-based milk now serves as the innovation leader in the milk category, supported by key advancements in ingredient diversification and product development that seeks to replicate both the sensory experience and nutritional value of cow's milk. In 2022, the sales value of plant-based milk in the overall distribution channel increased by 8.1% from 2021.

- In 2021, plant-based milk sales in retail channels increased by three times compared to cows' milk, which represents a 27% growth from 2020, where cows' milk growth stands at 9%. In the same year, 42% of households purchased plant-based milk, and 76% of plant-based milk buyers purchased it multiple times in retail channels. The growth is aided by shoppers in the United States who want to eat less animal-based foods due to the risks associated with animal-based foods, such as the presence of antibiotics, hormones, and others.

- Among overall plant-based products in the United States, plant-based milk sales have been increasing. The off-trade segment dominates the distribution channels of the United States plant-based milk market. In the off-trade segment, supermarkets and hypermarkets accounted for a major share. In 2022, supermarkets and hypermarkets accounted for an 80.9% share in terms of value.

- The on-trade channel is the fastest-growing segment in the United States plant-based milk market, which is anticipated to increase at a growth rate of 21.2% in 2024 from 2021. Many leading restaurants in the United States use plant-based milk, particularly as an ingredient option in cocktails, smoothies, coffees, and espresso-based drinks. In 2022, there were more than 600,000 restaurants in the United States.

United States Non-Dairy Milk Market Trends

Increasing lactose intolerance, growing preference for healthy food, and sustainable ingredient sourcing boosted the plant-based milk market

- Plant-based milk consumption per person is rising significantly in the United States, supported by investments and innovations by companies. More than 52% of US consumers prefer plant-based food. Most Americans generally consume less dairy and other animal products, and compared to vegans or vegetarians, they also tend to be more flexitarian. As of 2022, 7% of consumers in the United States adopted a flexitarian diet, compared to over 12% who prefer a plant-based diet. Although Americans of all ages are interested in plant-based foods, people in their 20s and 30s are the most interested.

- Nearly half of Americans (47%) consume plant-based milk regularly, which increased to 56% in the millennial and Generation X age groups. Factors such as increasing lactose intolerance, growing preference for healthy food, and sustainable ingredient sourcing resulted in major growth of the plant-based milk market. In the United States, 40% of Generation Z, 38% of millennials, 34% of Generation X, and 21% of Baby Boomers and seniors consume plant-based milk due to sustainably sourced ingredients.

- Governmental support is another factor boosting the production and consumption of plant-based dairy products in the country. The US government identified plant-based foods as an important and growing industry. Plant-based food companies in the United States received USD 5 billion in funding in 2021, up by 60% from 2020. The most mature portion of the alternative industry, the plant-based alternatives sector, secured USD 1.9 billion in investments in 2021, almost three times the USD 693 million raised in 2019.

United States Non-Dairy Milk Industry Overview

The United States Non-Dairy Milk Market is moderately consolidated, with the top five companies occupying 48.59%. The major players in this market are Blue Diamond Growers, Califia Farms LLC, Danone SA, Oatly Group AB and Walmart Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Dairy Alternative - Raw Material Production

- 4.3 Regulatory Framework

- 4.3.1 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product Type

- 5.1.1 Almond Milk

- 5.1.2 Cashew Milk

- 5.1.3 Coconut Milk

- 5.1.4 Hemp Milk

- 5.1.5 Oat Milk

- 5.1.6 Soy Milk

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 Convenience Stores

- 5.2.1.2 Online Retail

- 5.2.1.3 Specialist Retailers

- 5.2.1.4 Supermarkets and Hypermarkets

- 5.2.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Blue Diamond Growers

- 6.4.2 Califia Farms LLC

- 6.4.3 Campbell Soup Company

- 6.4.4 Danone SA

- 6.4.5 Oatly Group AB

- 6.4.6 Otsuka Holdings Co. Ltd

- 6.4.7 Ripple Foods PBC

- 6.4.8 SunOpta Inc.

- 6.4.9 Walmart Inc.

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

米国の非乳製品ミルク:市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日