|

市場調査レポート

商品コード

1693780

南米のバイオ肥料:市場シェア分析、産業動向、成長予測(2025年~2030年)South America Biofertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米のバイオ肥料:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 155 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

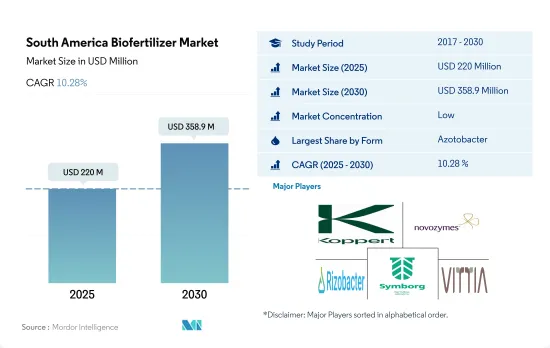

南米のバイオ肥料市場規模は、2025年には2億2,000万米ドルと推定され、2030年には3億5,890万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは10.28%で成長すると予測されます。

- バイオ肥料は、植物の成長と生産性を高める持続可能でエコフレンドリー方法です。バイオ肥料は生きた微生物から構成されており、土壌の栄養分を向上させ、植物にとって不可欠な要素をより利用しやすくします。最も一般的に使用されているバイオ肥料には、菌根菌、アゾスピリラム、アゾトバクタ、リゾビウム、リン酸可溶化細菌などがあります。

- これらの微生物は、土壌の健全性と肥沃度を向上させ、作物に必要な栄養素を供給する能力のために選択されます。これらの微生物は、有機物を分解して必須栄養素を放出するか、土壌中の特定の栄養素の利用可能性を直接高めることによって働いています。

- アゾトバクタは、この地域で消費されるバイオ肥料全体の28.6%を占めています。様々な農業気候条件下でのアゾトバクタの圃場検査により、このバイオ肥料はタマネギ、トマト、キャベツなどの作物の種子や苗に接種するのに適していることが明らかになりました。典型的な圃場環境では、アゾトバクタを接種することで、これらの作物における窒素肥料の必要性が10~20%減少します。したがって、農業におけるアゾトバクタの利用は、今後数年で拡大すると予想されます。

- ブラジルの調査では、Azospirillum brasilenseのAb-V5とAb-V6の2株を組み合わせることで、大豆、サトウキビ、コメ、小麦、牧草などの主要作物の収量が増加することが実証されています。これら2つの菌株の施用は、これらの作物で一般的に使用されている他の農薬との相性も良いです。

- 同地域のバイオ肥料市場は、有機栽培食品に対する需要の高まりと、土壌と環境をより安全に保つためのサステイナブル農法の重要性を政府が強調していることから、成長が見込まれています。

- ブラジルは南米有数の農業国であり、2022年には同地域のバイオ肥料市場全体の65.3%を占めています。同国の農業従事者は有機食品に対する世界の需要に対応しており、Global Organic Tradeによれば、2021年には前年比9.5%増の8,100万米ドルの有機食品売上を達成しました。

- この地域における有機作物の栽培面積は、2017年の49万5,700ヘクタールから2021年には71万7,200ヘクタールに増加しました。有機作物全体の増加傾向は、これらの国々におけるバイオ肥料市場を牽引すると予想され、2023~2029年の間にCAGR 10.0%を記録すると推定されます。

- 土壌汚染や環境汚染への懸念が高まる中、政府やその他の団体は、この地域全体で生物学的作物投入物の使用を強く推進しています。アルゼンチンでは、FAOの2022~2031年戦略的枠組みが、農業における化学肥料と農薬の使用削減に重点を置き、農業経済的な方法を用いて、より効率的でサステイナブル農業食品システムへの転換を優先しています。これは、よりサステイナブル代替手段としてバイオ肥料を採用する機会を開くものです。

- さらに、マメ科作物の収穫量も著しく増加しています。根粒菌の株はインドール酢酸のような成長ホルモンを生産し、根粒の形成と開発を迅速に刺激することで、植物の成長に好影響を与えます。バイオ肥料使用の利点は、南米での使用を促進すると予想されます。しかし、農業従事者の意識が低く、化学農法から有機農法への移行期間が長いことが、バイオ肥料の市場成長を若干妨げています。

南米のバイオ肥料市場動向

大豆、トウモロコシ、ヒマワリ、小麦の国際需要の高まりによる有機栽培面積の増加。

- The Research Institute of Organic Agriculture(FibL統計)が提供したデータによると、南米における作物の有機栽培面積は2021年に67万2,800ヘクタールと記録されました。アルゼンチンとウルグアイはこの地域の主要な有機生産国で、有機作物栽培面積が大きく、アルゼンチンは2021年にこの地域の有機栽培面積の11.5%のシェアを占めています。アルゼンチンで生産される主要有機作物には、サトウキビ、原毛、果物、野菜、豆類が含まれます。主要有機輸出品は大豆、トウモロコシ、ヒマワリ、小麦です。

- 2021年の有機作物栽培面積は38万4,300ヘクタールで、現金作物が53.9%と最大のシェアを占めています。この地域は、サトウキビ、ココア、コーヒー、綿花などの換金作物の主要生産地です。ブラジルはこの地域最大のサトウキビ生産国です。

- 一方、ウルグアイはこの地域で有機野菜や果物の栽培が盛んです。ウルグアイ有機農業者協会は、様々な有機小売店と提携することで、国内の有機栽培を推進しています。世界銀行が資金提供した「天然資源と気候変動のサステイナブル管理」プロジェクト(DACC)は、2022年に5,139の農業従事者が気候変動対応型農業(CSA)を導入するのを支援し、同地域の有機作物の栽培面積の増加に貢献しました。

- 南米では何百万もの農業従事者が外部からの投入物を使わない農業を続けており、国内生産が著しく低いにもかかわらず、この地域経済の将来を担う可能性は十分にあります。国民は健康志向を強めており、南米のますます環境に優しくサステイナブル農業システムに、より大きな市場を創出しています。

アルゼンチン、ブラジル、コロンビアの消費者の約49.0%が有機食品の購入に関心を持っています。

- 南米は、世界的に見ても有機食品の重要な生産・輸出国のひとつです。南米におけるオーガニック食品への一人当たりの支出は、世界の他の地域よりも比較的少ないです。2022年の1人当たり平均支出額は4.3米ドルでした。こうした輸出志向の国々は現在、見過ごされがちな国内需要を生み出しています。

- アルゼンチン、ブラジル、コロンビアといった南米諸国では、オーガニック食品のような自然栽培の製品に対する需要が高まっています。2021年にウィスコンシン州経済開発が実施した調査では、消費者は有機栽培の食品により高い価格を支払うことを望んでいることが証明されました。この調査では、消費者の43~49%が健康に気を配っていることが明らかになりました。ブラジルは、オーガニック包装食品と飲食品に対する一人当たりの支出額で世界第43位です。

- 2021年のGlobal Organic Tradeのデータによると、アルゼンチンの有機製品市場は2021年に1,590万米ドルに達し、世界市場規模の0.03%を占め、一人当たり消費額は0.35米ドルです。

- 現在、同地域のオーガニック食品市場は非常にセグメント化されており、入手可能なのは一部のスーパーマーケットや専門店に限られています。現在、コスタリカ、メキシコ、南米の都市部を中心に、この地域の多くのスーパーマーケット、専門店、地元のファーマーズ・マーケットが有機食品を販売し、潜在的な需要の高まりに応えています。消費者の意識の高まりとその購買動機は、この地域における有機食品の持続可能性の特性に対する理解を深めることにつながると予想されます。

南米バイオ肥料産業の概要

南米のバイオ肥料市場はセグメント化されており、上位5社で19.47%を占めています。この市場の主要企業は、Koppert Biological Systems Inc.、Novozymes、Rizobacter、Symborg Inc.、Vittia Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 有機栽培面積

- 一人当たりのオーガニック製品への支出

- 規制の枠組み

- アルゼンチン

- ブラジル

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 形態

- アゾスピリラム

- アゾトバクタ

- 菌根菌

- リン酸可溶菌

- 根粒菌

- その他のバイオ肥料

- 作物タイプ

- 換金作物

- 園芸作物

- 畑作物

- 国名

- アルゼンチン

- ブラジル

- その他の南米

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Atlantica Agricola

- IPL Biologicals Limited

- Koppert Biological Systems Inc.

- Novozymes

- Plant Response BIoTech Inc.

- Rizobacter

- Sustane Natural Fertilizer Inc.

- Symborg Inc.

- T.Stanes and Company Limited

- Vittia Group

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 500040

The South America Biofertilizer Market size is estimated at 220 million USD in 2025, and is expected to reach 358.9 million USD by 2030, growing at a CAGR of 10.28% during the forecast period (2025-2030).

- Biofertilizers are a sustainable and eco-friendly way of enhancing plant growth and productivity. They are composed of living microorganisms that can improve the soil's nutrient content, making essential elements more accessible to plants. Some of the most commonly used biofertilizers include mycorrhiza, Azospirillum, Azotobacter, Rhizobium, and phosphate-solubilizing bacteria.

- These microorganisms are selected for their ability to improve the soil's health and fertility, providing crops with the nutrients required. They work by either breaking down organic matter to release essential nutrients or directly increasing the availability of specific nutrients in the soil.

- Azotobacter accounted for 28.6% of the total biofertilizers consumed in the region. Field tests on Azotobacter under various agro-climatic conditions revealed that the biofertilizer is suitable for inoculating with seeds or seedlings of crops such as onion, tomato, and cabbage. Under typical field circumstances, Azotobacter inoculation reduces the need for nitrogenous fertilizers in these crops by 10-20%. Thus, the usage of Azotobacter in agriculture is expected to grow in the coming years.

- Research in Brazil has demonstrated that the combination of two strains of Azospirillum brasilense, Ab-V5 and Ab-V6, increased yields in key crops such as soybean, sugarcane, rice, wheat, and pasture. The application of these two strains is also compatible with other pesticides commonly used in these crops.

- The market for biofertilizers in the region is expected to grow due to the rising demand for organically-grown food and the government's emphasis on the importance of sustainable agricultural practices to keep the soil and environment safer.

- Brazil is a leading agriculture nation in South America and held 65.3% of the total biofertilizer market in the region in 2022. The country's farmers are keeping up with the worldwide demand for organic food and achieved organic food sales worth USD 81.0 million in 2021, which rose 9.5% compared to the previous year, as per the Global Organic Trade.

- The area under cultivation of organic crops in the region increased from 495.7 thousand hectares in 2017 to 717.2 thousand hectares in 2021. The increasing trend in the overall organic crop is expected to drive the market for biofertilizers in these countries and is estimated to register a CAGR of 10.0% between 2023 and 2029.

- With growing concern for soil and environmental pollution, the government and other organizations are highly promoting the usage of biological crop inputs across the region. In Argentina, the FAO's 2022-2031 Strategic Framework prioritizes transforming agri-food systems to be more efficient and sustainable, using agroeconomic methods, with a focus on reducing the use of chemical fertilizers and pesticides in agriculture. This opens up opportunities for adopting biofertilizers as a more sustainable alternative.

- Moreover, there has been a remarkable increase in the crop yield of leguminous crops. Strains of rhizobium produce growth hormones like indole acetic acid, which influences positive growth in plants by stimulating the formation and development of root nodules quickly. The advantages of biofertilizer usage are expected to drive their usage in South America. However, less awareness among the farmers and the long transition period from chemical farming to organic farming are slightly hindering the market growth of biofertilizers.

South America Biofertilizer Market Trends

Growing organic acreage owning to the rising international demand for soy, corn, sunflower, and wheat.

- The area under organic cultivation of crops in South America was recorded at 672.8 thousand hectares in 2021, according to the data provided by The Research Institute of Organic Agriculture (FibL statistics). Argentina and Uruguay are the major organic-producing countries in the region, with a large area under organic crop cultivation, with Argentina occupying a share of 11.5% of the organic area in the region in 2021. The primary organic crops produced in Argentina include sugarcane, raw wool, fruits, vegetables, and beans. The primary organic exports are soy, corn, sunflower, and wheat.

- Cash crops accounted for the maximum share of 53.9% under organic crop cultivation in 2021, with 384.3 thousand hectares of land. The region is a major grower of cash crops like sugarcane, cocoa, coffee, and cotton. Brazil is the largest sugarcane-growing country in the region.

- On the other hand, Uruguay is a large grower of organic fruits and vegetables in the region. The Organic Farmers' Association of Uruguay promotes organic cultivation in the country by partnering with various organic retail outlets. The World Bank-financed Sustainable Management of Natural Resources and Climate Change project (DACC) assisted 5,139 farmers in 2022 to adopt climate-smart agriculture (CSA), which helped increase the area under cultivation of organic crops in the region.

- Millions of farmers in South America continue to practice no-external input agriculture, which may very well represent the future of the region's economy despite the noticeably low domestic production. The population is becoming more health conscious, which creates a larger market for South America's increasingly eco-friendly and sustainable farming system.

Approximately 49.0% consumers in Argentina, Brazil and Colombia are interested in purchasing organic food.

- South America is one of the important producers and exporters of organic food products globally. The per capita spending on organic food products in South America is comparatively lesser than in other parts of the world. The average per capita spending was recorded as USD 4.3 in 2022. Nevertheless, these export-oriented countries are now generating an often-overlooked domestic demand.

- The demand for naturally grown products like organic food in South American countries like Argentina, Brazil, and Colombia has increased. A survey conducted by Wisconsin Economic Development in 2021 proved that consumers are willing to pay higher prices for organically grown food. The study revealed that 43-49% of consumers are conscious about their health. Brazil ranks 43rd globally for per capita spending on organic packaged food and beverages.

- The organic products market in Argentina reached a value of USD 15.9 million in 2021, representing 0.03% of the global market value, with a per capita consumption of USD 0.35, as per the data given by Global Organic Trade in 2021.

- Currently, the market for organic foods in the region is very fragmented, with its availability limited to a few supermarkets and specialty stores, as only people from higher-income families are potential customers. Many supermarkets, specialized stores, and local farmers' markets in the region are now selling organic food to satisfy the growing latent demand for such products, mainly in Costa Rica, Mexico, and urban centers of South America. Growing awareness among consumers and their buying motives are expected to lead to a better understanding of the sustainability attributes of organic food in the region.

South America Biofertilizer Industry Overview

The South America Biofertilizer Market is fragmented, with the top five companies occupying 19.47%. The major players in this market are Koppert Biological Systems Inc., Novozymes, Rizobacter, Symborg Inc. and Vittia Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Azospirillum

- 5.1.2 Azotobacter

- 5.1.3 Mycorrhiza

- 5.1.4 Phosphate Solubilizing Bacteria

- 5.1.5 Rhizobium

- 5.1.6 Other Biofertilizers

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Atlantica Agricola

- 6.4.2 IPL Biologicals Limited

- 6.4.3 Koppert Biological Systems Inc.

- 6.4.4 Novozymes

- 6.4.5 Plant Response Biotech Inc.

- 6.4.6 Rizobacter

- 6.4.7 Sustane Natural Fertilizer Inc.

- 6.4.8 Symborg Inc.

- 6.4.9 T.Stanes and Company Limited

- 6.4.10 Vittia Group

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms