|

市場調査レポート

商品コード

1693759

欧州の有機肥料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Organic Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の有機肥料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 169 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

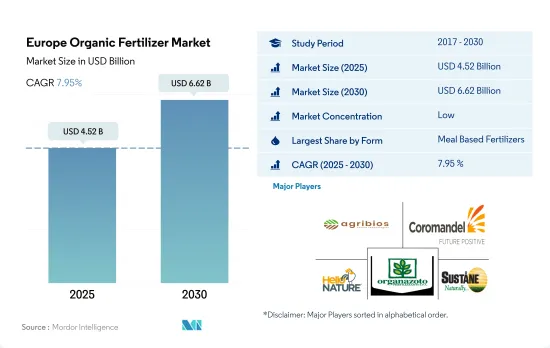

欧州の有機肥料市場規模は2025年に45億2,000万米ドルと推定・予測され、2030年には66億2,000万米ドルに達し、予測期間(2025~2030年)のCAGRは7.95%で成長すると予測されています。

- 2022年の欧州有機肥料市場は、主にミール系肥料が市場の62.0%を占めています。これらの肥料は窒素、リン、カリウム、カルシウムを豊富に含むため、農作物にとって非常に有益です。肉骨粉をベースにした有機肥料は、鉱物肥料の需要を減らし、大量の食肉加工廃棄物を処理するためのエコフレンドリー解決策を記載しています。肥料も欧州の有機肥料市場に大きく貢献しており、2022年には38.3%のシェアを記録しました。このセグメントの市場規模は2017~2022年の間に58.2%の増加を記録しました。

- 欧州における2022年の有機肥料消費量では、耕作作物が77.7%のシェアを占め、園芸作物がそれに続きました。これは、同地域の連作作物の栽培面積が大きく、2022年の有機作物栽培面積全体の82.3%に達したことに起因しています。

- 低炭素経済諸国の開発はEUの成長戦略の主要目標であり、有機肥料はこの取り組みに大きく貢献する可能性を秘めています。有機肥料は大気中の二酸化炭素を土壌に移行させる働きがあり、有機物を多く含むため、二酸化炭素が大気中に放出されるのを防ぐことができます。このアプローチは、2023~2029年にかけてCAGR 7.8%を記録すると推定される欧州有機肥料市場を牽引すると期待されています。

- 2022年の欧州有機肥料市場は、ミールベースの肥料と肥料が大半を占め、連作作物が主要消費者でした。欧州連合(EU)が低炭素経済を推進し続ける中、有機肥料の需要は増加し、市場の成長を促進すると予想されます。

- 欧州は有機作物の主要生産者の1つとして台頭しており、2020年時点で42万人の有機生産者がいます。2022年には、欧州は世界の有機肥料市場の41.7%を占め、このセグメントにおける同地域の優位性を物語っています。この地域の主要作物には小麦、トウモロコシ、ライ麦、大麦、テンサイ、ジャガイモなどがあり、連作作物が有機肥料消費の大半を占めています。

- 欧州の有機農地面積は着実に増加しており、2017年の490万ヘクタールから2022年には690万ヘクタールへと7.1%の成長率を示しています。これは、2030年までにEUの農地に占める有機農業の割合を最低25.0%にするという欧州委員会の目標によるところが大きいです。

- 欧州連合(EU)は現在、新しい肥料製品、特にバイオ廃棄物やその他の二次原料からリサイクルされた栄養素や有機物を含む肥料製品の市場参入を容易にすることを目的として、2003年以来初めてとなる肥料規則の改正を行っています。この新規制はまた、EUのすべての国で販売される肥料製品の安全基準と品質基準を定めるものです。有機肥料は、循環的で資源効率に優れており、まさに新規制の対象となる肥料製品です。

- 世界の有機肥料市場における欧州の存在感の大きさと、有機農業のシェア拡大に対する欧州のコミットメントが相まって、欧州の有機肥料市場は将来有望です。肥料規則の改正が予定されていることから、この産業では技術革新と成長の急増が予想され、さまざまな利害関係者に事業拡大の機会が提供されます。

欧州有機肥料市場の動向

欧州のグリーンディールは有機栽培の拡大に大きく貢献しています。

- 欧州諸国は有機農業をますます推進しており、有機栽培に分類される土地の量は過去10年間で大幅に増加しています。2021年3月、欧州委員会は、2030年までに農地の25%を有機栽培にするという欧州グリーンディール目標を達成するため、有機アクションプランを立ち上げました。オーストリア、イタリア、スペイン、ドイツは、欧州における有機農業の主要国のひとつです。イタリアでは、農地面積の15.0%が有機農法で栽培されており、EU平均の7.5%を上回っています。

- 2021年には、欧州連合(EU)の有機農地は1,470万ヘクタールとなりました。農業生産面積は、耕地作物(主に穀物、根菜類、生鮮野菜)、永続的草地、永続的作物(果樹・ベリー類、オリーブ畑、ブドウ畑)の3つの利用タイプに大別されます。2021年の有機耕地面積は650万ヘクタールで、EU全体の有機農地面積の46%に相当します。

- EUにおける穀物、油糧種子、タンパク質作物、豆類の有機栽培面積は、2017~2021年の間に32.6%増加し、160万ヘクタール以上に達しました。栽培面積は130万ヘクタールで、オリーブ、ブドウ、アーモンド、柑橘類などの多年生作物は、2020年にはこの地域の有機栽培地の15%を占めます。スペイン、イタリア、ギリシャは有機オリーブの主要栽培国で、2021年の栽培面積はそれぞれ256,507ヘクタール、208,212ヘクタール、56,507ヘクタールです。オリーブもブドウも、国内外に需要を生み出す特産品に生まれ変わることができるため、欧州経済にとって極めて重要です。この地域における有機栽培面積の拡大は、欧州の有機栽培産業をさらに強化すると予想されます。

有機食品への需要の高まり、一人当たりの支出の増加は、有機肥料市場にプラスの効果をもたらすと考えられます。

- 欧州の消費者は、天然材料と製法で作られた商品をより多く購入しています。有機食品はEUの農業生産全体のごく一部にすぎないが、もはやニッチ産業ではないです。欧州連合(EU)は、オーガニック商品の単一市場としては国際的に2番目に大きく、1人当たりの平均支出額は年間74.8米ドルです。欧州におけるオーガニック食品への1人当たりの支出は、過去10年間で倍増しています。2020年には、スイスとデンマークの消費者が有機食品に最も多く支出した(それぞれ1人当たり494.09米ドルと453.90米ドル)。

- 世界のオーガニックトレードのデータによれば、ドイツは欧州で最大のオーガニック食品市場であり、米国に次いで世界第2位で、2021年の市場規模は63億米ドル、1人当たり消費額は75.6米ドルです。同国は世界の有機食品需要の10.0%を占め、そのシェアは2021~2026年にかけて2.7%のCAGRで推移すると推定されます。

- フランスの有機食品市場は力強い成長を示し、2021年の小売売上高は12.6%増加しました。世界のオーガニックトレードのデータによると、同国の1人当たりの有機食品への支出は2021年に88.8米ドルを記録しました。2018年、Agence BIO/Spirit Insight Barometerが記録したように、フランス人の88%がオーガニック製品を消費したことがあると宣言しました。健康、環境、動物福祉の保護は、フランスでオーガニック食品を消費する主要理由です。オーガニック食品産業は、スペイン、オランダ、スウェーデンを含む他のいくつかの国でも、オーガニックストアの開店とともに成長し始めています。有機食品の売上が伸びたのは、COVID-19の大流行の最中とその後に端を発しており、消費者が健康問題に関心を向け始め、従来の方法で栽培された食品の悪影響を認識するようになったためです。

欧州の有機肥料産業概要

欧州の有機肥料市場はセグメント化されており、上位5社で1.36%を占めています。この市場の主要企業は、Agribios Italiana s.r.l.、Coromandel International Ltd.、HELLO NATURE ITALIA srl、ORGANAZOTO FERTILIZZANTI SPA、Sustane Natural Fertilizer Inc.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 有機栽培面積

- 一人当たりのオーガニック製品への支出

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 形態

- 肥料

- ミールベース肥料

- オイルケーキ

- その他の有機肥料

- 作物タイプ

- 換金作物

- 園芸作物

- 畑作物

- 国名

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Agribios Italiana s.r.l.

- Angibaud

- APC AGRO

- Coromandel International Ltd.

- Fertikal NV

- HELLO NATURE ITALIA srl

- Indogulf BioAg LLC(Indogulf Companyのバイオテク部門)

- ORGANAZOTO FERTILIZZANTI SPA

- Plantin

- Sustane Natural Fertilizer Inc.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Europe Organic Fertilizer Market size is estimated at 4.52 billion USD in 2025, and is expected to reach 6.62 billion USD by 2030, growing at a CAGR of 7.95% during the forecast period (2025-2030).

- The European organic fertilizers market in 2022 was primarily dominated by meal-based fertilizers, which accounted for 62.0% of the market. These fertilizers are highly beneficial to agricultural crops as they are rich in nitrogen, phosphorus, potassium, and calcium. Organic fertilizers based on meat and bone meal help reduce the demand for mineral fertilizers and provide an eco-friendly solution for disposing of large amounts of meat processing waste. Manures also contributed significantly to the European organic fertilizers market, registering a share of 38.3% in 2022. The segment's market value recorded an increase of 58.2% between 2017 and 2022.

- Row crops accounted for a significant portion of the organic fertilizer consumption in 2022 in Europe, with a share of 77.7%, followed by horticultural crops. This can be attributed to the large cultivation area of row crops in the region, which amounted to 82.3% of the total organic crop cultivation area in 2022.

- The development of a low-carbon economy is a primary goal of the EU's growth strategy, and organic fertilizers have the potential to make a significant contribution to this effort. Organic fertilizers help transfer atmospheric carbon dioxide into the soil, which prevents it from being released back into the atmosphere due to their high organic matter content. This approach is expected to drive the European organic fertilizers market, which is estimated to register a CAGR of 7.8% between 2023 and 2029.

- The European organic fertilizer market in 2022 was dominated by meal-based fertilizers and manures, with row crops being the primary consumers. As the European Union continues to push for a low-carbon economy, the demand for organic fertilizers is expected to increase, driving growth in the market.

- Europe has emerged as one of the major producers of organic crops, with 420,000 organic producers as of 2020. In 2022, Europe accounted for 41.7% of the global organic fertilizer market, a testament to the region's dominance in this field. The region's primary crops include wheat, maize, rye, barley, sugar beet, and potatoes, with row crops accounting for the majority of organic fertilizer consumption.

- Europe's organic agricultural acreage has been increasing steadily, with a growth rate of 7.1% from 4.9 million hectares in 2017 to 6.9 million hectares in 2022. This is largely due to the European Commission's objective of increasing the share of organic agriculture to a minimum of 25.0% of the EU's agricultural land by 2030.

- The European Union (EU) is currently revising its fertilizer Regulation for the first time since 2003, aiming to make it easier for new fertilizing products, particularly those containing nutrients or organic matter recycled from biowaste or other secondary raw materials, to enter the market. The new regulation will also establish safety and quality standards for fertilizing products sold in all EU countries. Organic-based fertilizers, with their circular and resource-efficient nature, are precisely the type of fertilizing products targeted by the new regulation.

- Europe's significant presence in the global organic fertilizers market, combined with the region's commitment to increasing the share of organic agriculture, presents a promising future for the organic fertilizers market in Europe. With the upcoming revision of the Fertilizer Regulation, the industry is expected to witness a surge in innovation and growth, providing opportunities for various stakeholders to expand their businesses.

Europe Organic Fertilizer Market Trends

European Green Deal is majorly contributing for increasing organic cultivation.

- European countries are increasingly promoting organic farming, and the amount of land categorized as organic has increased significantly over the last decade. In March 2021, the European Commission launched an organic action plan to achieve the European Green Deal target of ensuring that 25% of agricultural land is under organic farming by 2030. Austria, Italy, Spain, and Germany are among the leading countries for organic agriculture in the European region. In Italy, 15.0% of the agriculture area is under organic farming, which is higher than the EU average of 7.5%.

- In 2021, there were 14.7 million hectares of organic land in the European Union (EU). The agricultural production area is divided into three main types of use: arable land crops (mainly cereals, root crops, and fresh vegetables), permanent grassland, and permanent crops (fruit trees and berries, olive groves, and vineyards). The area of organic arable land was 6.5 million hectares in 2021, the equivalent of 46% of the EU's total organic agricultural area.

- The organic areas of cereals, oilseeds, protein crops, and pulses in the European Union increased by 32.6% between 2017 and 2021, reaching more than 1.6 million hectares. With 1.3 million hectares under cultivation, perennial crops like Olives, grapes, almonds, and citrus fruits accounted for 15% of the organic land in the region in 2020. Spain, Italy, and Greece are major growers of organic olive trees, with an area of 256,507, 208,212, and 56,507 hectares, respectively, in 2021. Both olives and grapes are crucial for the European economy as they can be turned into specialty products that generate demand locally and internationally. The growing organic acreage in the region is expected to further strengthen the European organic cultivation industry.

Growing demand for organic food, rising the per capita spending, will have a positive effect over organic fertilizer market

- Consumers in Europe are purchasing more goods made using natural materials and methods. Even though organic food only makes up a small fraction of the total EU agricultural production, it is no longer a niche industry. The European Union represents the second-largest single market for organic goods internationally, with an average per capita spending of USD 74.8 annually. The per capita spending on organic food in Europe has doubled in the last decade. In 2020, Swiss and Danish consumers spent the most on organic food (USD 494.09 and USD 453.90 per capita, respectively).

- Germany is the largest organic food market in the European region and the second largest in the world after the United States, with a market size of USD 6.3 billion and a per capita consumption of USD 75.6 in 2021, as per Global Organic Trade data. The country accounted for 10.0% of the global organic food demand, with its share estimated to record a CAGR of 2.7% between 2021 and 2026.

- The French organic food market witnessed strong growth, with a 12.6% rise in retail sales in 2021. The country's per capita spending on organic food was recorded at USD 88.8 in 2021, as per Global Organic Trade data. In 2018, as recorded by the Agence BIO/Spirit Insight Barometer, 88% of French people declared having consumed organic products. Preserving health, environment, and animal welfare are the primary justifications for consumers of organic foods in France. The organic food industry has begun to grow in several other nations, including Spain, the Netherlands, and Sweden, with the opening of organic stores. The growth in organic sales was triggered during and after the COVID-19 pandemic, as consumers began paying more attention to health issues and becoming aware of the adverse effects of conventionally grown food.

Europe Organic Fertilizer Industry Overview

The Europe Organic Fertilizer Market is fragmented, with the top five companies occupying 1.36%. The major players in this market are Agribios Italiana s.r.l., Coromandel International Ltd., HELLO NATURE ITALIA srl, ORGANAZOTO FERTILIZZANTI SPA and Sustane Natural Fertilizer Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 Turkey

- 4.3.8 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Manure

- 5.1.2 Meal Based Fertilizers

- 5.1.3 Oilcakes

- 5.1.4 Other Organic Fertilizers

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Russia

- 5.3.6 Spain

- 5.3.7 Turkey

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Agribios Italiana s.r.l.

- 6.4.2 Angibaud

- 6.4.3 APC AGRO

- 6.4.4 Coromandel International Ltd.

- 6.4.5 Fertikal NV

- 6.4.6 HELLO NATURE ITALIA srl

- 6.4.7 Indogulf BioAg LLC (Biotech Division of Indogulf Company)

- 6.4.8 ORGANAZOTO FERTILIZZANTI SPA

- 6.4.9 Plantin

- 6.4.10 Sustane Natural Fertilizer Inc.

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms