インドの有機肥料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

India Organic Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693765

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

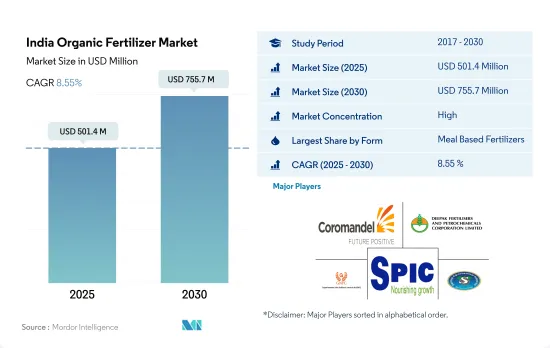

インドの有機肥料市場規模は2025年に5億140万米ドルと推定され、2030年には7億5,570万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは8.55%で成長する見込みです。

- 有機肥料は有機物を大量に含み、土壌の生物活性を高め、土壌の生物多様性を維持・向上させています。有機肥料は有機農法とプラクティス農法で広く使用されているため、2022年にはインドの作物栄養セグメント全体の69.9%を占めました。

- ミールベースの肥料は最も評価の高い有機肥料を構成し、2022年の有機肥料市場の67.5%を占めました。しかし、肉粉市場、特に牛肉ベースの肉粉はインドではあまり受け入れられておらず、骨粉の生産はインドの多くの地域で限られています。

- 肥料はインドで最も消費されている有機肥料であり、その入手のしやすさが最大の市場シェアを占めています。作物の品種に関係なく、ほとんどすべての作物に施用されています。農業従事者は、肥料としてたい肥を適切に使用することで、しばしば費用を節約することができます。このセグメントの量は、2023~2029年にかけて推定CAGR 4.8%で成長すると予測されています。

- 有機肥料の消費は連作作物で優位を占めており、2022年の市場規模の約85.0%を占めました。連作作物が優勢なのは、主に国内での栽培面積が大きいためで、2022年には有機作物総面積の約59.8%を占めました。

- 国内外市場において有機製品に対する需要は高く、化学肥料の過剰使用は同国の大きな課題のひとつです。インド政府は、有機肥料にインセンティブを与えることで、様々な制度やプログラムを通じてサステイナブル有機栽培の実践を推進しており、2023~2029年の間に市場を牽引すると予想されます。

インドの有機肥料市場動向

有機生産者の増加により、主に連作作物で有機栽培面積が増加

- インドは、認証された有機生産者の総数では世界最大の国であり、2019年には130万人の有機生産者がいます。多くの有機生産者がいるにもかかわらず、同国の有機栽培面積は同国の全農業面積の約2.0%です。2021年の同国の有機栽培面積は711,094.0haで、2017年と比較して約3.4%増加しました。

- 国内の有機農業はいくつかの州に集中しています。国内の有機農業上位10州が有機作物総面積の約80.0%を占めています。有機農業の普及率向上で先陣を切っている州はいくつかあります。マディヤ・プラデシュ州、ラジャスタン州、マハラシュトラ州が有機農業の上位3州です。マディヤ・プラデシュ州は、2019年のインド全体の有機栽培面積の約27.0%を占めました。

- 国内では連作作物の有機栽培が優勢です。2021年の有機栽培作物総面積の約59.7%を列作物が占めています。国内では穀類作物の生産が優勢で、米、小麦、キビ、トウモロコシが主要穀類作物です。ほとんどの穀類はカリフ期(6~9月)に栽培されます。この時期に栽培される作物は、主に雨に左右されるか、稲、トウモロコシ、綿花、大豆など、より多くの水を必要とします。

- 有機換金作物全体の栽培面積は増加傾向にあり、2017年の27万haから2021年には28万haとなります。同国で生産される主要換金作物には、綿花、サトウキビ、紅茶、スパイスなどがあります。現在、同国では有機園芸作物の成長は限られています。有機製品に対する需要の増加とインド政府による有機栽培への取り組みにより、2023~2029年にかけて有機作物栽培面積は増加すると予想されます。

需要の高まりとeコマースチャネルを通じた入手の容易さにより、有機食品への1人当たり支出が増加

- インドのオーガニック製品に対する1人当たり支出は0.23米ドルと、アジア太平洋のオーガニック製品に対する1人当たり支出の平均と比べると比較的低いです。しかし近年、消費者の需要はオーガニック製品にますますシフトしています。オーガニック製品は免疫力が高く、品質が高く、eコマースチャネルを通じて入手しやすいからです。インドは有機食品と飲食品の有望な市場です。インド国内の有機飲食品産業は、2024年までに1億3,800万米ドルの規模になると予想され、2019~2024年のCAGRは13%です。

- 2022年には、1億800万米ドル相当の有機飲食品が国内で消費されました。同国における有機製品の消費額は、2016年の4,500万米ドルから2021年には9,600万米ドルに増加しました。有機食品の売上が増加したのは主に消費者の意識が高まったためであり、高所得の消費者が有機食品と飲食品の消費を促進しています。最も需要が多かったカテゴリーには、有機卵、乳製品、果物・野菜などの必須食品が含まれます。

- 有機飲料の消費が市場を独占し、2022年の有機食品と有機飲料の合計市場額の約85.2%を占めました。有機飲料セグメントには、承認された認証機関によって認証された有機包装飲食品が含まれます。有機飲料の消費額は、2020~2022年にかけてCAGR 14%の成長を記録しました。有機製品に関連する価格プレミアムは、低所得層の消費者のアクセスを妨げ、有機食品消費の主要制限要因となっています。しかし、有機製品の積極的な販売促進と利点が、予測期間中の有機食品市場を牽引すると予想されます。

インドの有機肥料産業概要

インドの有機肥料市場はかなり統合されており、上位5社で72.35%を占めています。この市場の主要企業は、Coromandel International Ltd、Deepak Fertilisers & Petrochemicals Corp. Ltd、Gujarat Narmada Valley Fertilizers & Chemicals Ltd、Southern Petrochemical Industries Corp. Ltd、Swaroop Agrochemical Industriesなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 有機栽培面積

- 一人当たりのオーガニック製品への支出

- 規制の枠組み

- インド

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 形態

- 肥料

- ミールベース肥料

- オイルケーキ

- その他の有機肥料

- 作物タイプ

- 換金作物

- 園芸作物

- 畑作物

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Amruth Organic Fertilizers

- Coromandel International Ltd

- Deepak Fertilisers & Petrochemicals Corp. Ltd

- GrowTech Agri Science Private Limited

- Gujarat Narmada Valley Fertilizers & Chemicals Ltd

- Gujarat State Fertilizers & Chemicals Ltd

- Prabhat Fertilizer And Chemical Works

- Southern Petrochemical Industries Corp. Ltd

- Swaroop Agrochemical Industries

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The India Organic Fertilizer Market size is estimated at 501.4 million USD in 2025, and is expected to reach 755.7 million USD by 2030, growing at a CAGR of 8.55% during the forecast period (2025-2030).

- Organic fertilizers contain organic matter in large quantities, which boosts biological activities in soil and aids in maintaining and enhancing soil biodiversity. Organic fertilizers accounted for 69.9% of the total Indian crop nutrition segment in 2022, owing to their widespread use in organic and conventional farming.

- Meal-based fertilizers constituted the most valued organic fertilizer, accounting for 67.5% of the organic fertilizer market in 2022. However, the meat meal market, especially cattle meat-based meals, is not well accepted in India, and the production of bone meals is limited in many parts of India.

- Manures constitute the most consumed organic fertilizer in India, with the largest market share attributed to their easy availability. They are applied to almost all crops, regardless of crop variety. Farmers can often save money by properly using manure as a fertilizer. The segment's volume is projected to grow, with an estimated CAGR of 4.8% between 2023 and 2029.

- The consumption of organic fertilizers is dominant in row crops and accounted for about 85.0% of the market volume in 2022. The dominance of row crops is mainly due to their large cultivation area in the country, which accounted for approximately 59.8% of the total organic crop area in 2022.

- There is a high demand for organic products in domestic and international markets, and the overuse of chemical fertilizers is one of the major challenges in the country. The Indian government's promotion of sustainable or organic cultivation practices through various schemes or programs by providing incentives for organic fertilizers is expected to drive the market between 2023 and 2029.

India Organic Fertilizer Market Trends

Growing number of organic producers helping the increase in area under organic cultivation, primarily in row crops

- India is the largest country, in terms of the total number of certified organic producers in the world, with 1.3 million organic producers in 2019. Despite a large number of organic producers, organic cultivation areas in the country account for around 2.0% of the total agriculture area in the country. In 2021, the organic area in the country was 711,094.0 ha, which increased by about 3.4% compared to 2017.

- Organic farming in the country is concentrated in only a few states. The top ten organic farming states in the country account for about 80.0% of the total organic crop area. A few states have taken the lead in improving organic farming coverage. Madhya Pradesh, Rajasthan, and Maharashtra are the top three organic farming states in the country. Madhya Pradesh accounted for about 27.0% of India's total organic cultivation area in 2019.

- Organic cultivation of row crops is dominant in the country. Row crops accounted for about 59.7% of the total organic crop area in 2021. Cereal crop production dominates in the country, with rice, wheat, millet, and maize being the major cereals produced. Most cereal crops are grown in the Kharif season (June-September). The crops grown in this season mainly depend on rain or require more water, like rice, maize, cotton, soybean, etc.

- There has been an increasing trend in the overall organic cash crop cultivation area, from 270,000 ha in 2017 to 280,000 ha in 2021. The major cash crops produced in the country include cotton, sugarcane, tea, and spices. Currently, there is limited growth of organic horticultural crops in the country. The increasing demand for organic products and initiatives by the Indian government to go organic are anticipated to increase the organic crop area between 2023 and 2029.

Growing demand and their easy accessibility through e-commerce channels, rising the per capita spending on organic food

- India's per capita spending on organic products is relatively low at USD 0.23 compared to the average per capita spending on organic products of the Asia-Pacific region. However, in recent years, consumer demand has been increasingly shifting toward organic products as these items offer better immunity, higher quality, and more accessibility through e-commerce channels. India is a promising, developing market for organic foods and beverages. India's domestic organic food and beverage industry is expected to be worth USD 138.0 million by 2024, a CAGR of 13% between 2019 to 2024.

- In 2022, organic food and beverages worth USD 108.0 million were consumed in the country. The consumption value of organic products in the country increased from USD 45.0 million in 2016 to USD 96.0 million in 2021. Organic food sales increased mainly due to increasing consumer awareness, and high-income consumers are propelling organic food and beverage consumption. Categories that experienced the most demand included essential foods such as organic eggs, dairy, and fruits and vegetables.

- The consumption of organic beverages dominated the market and accounted for about 85.2% of the total combined organic food and beverages market value in 2022. The organic beverages segment includes organic packaged food and beverages that are certified by the approved certification body. The consumption value of organic beverages registered growth with a CAGR of 14% between 2020 to 2022. The price premium associated with organic products hampers lower-income consumer access and is the major limiting factor for organic food consumption. However, the active promotion and advantages of organic products are expected to drive the organic food market in the forecast period.

India Organic Fertilizer Industry Overview

The India Organic Fertilizer Market is fairly consolidated, with the top five companies occupying 72.35%. The major players in this market are Coromandel International Ltd, Deepak Fertilisers & Petrochemicals Corp. Ltd, Gujarat Narmada Valley Fertilizers & Chemicals Ltd, Southern Petrochemical Industries Corp. Ltd and Swaroop Agrochemical Industries (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Manure

- 5.1.2 Meal Based Fertilizers

- 5.1.3 Oilcakes

- 5.1.4 Other Organic Fertilizers

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Amruth Organic Fertilizers

- 6.4.2 Coromandel International Ltd

- 6.4.3 Deepak Fertilisers & Petrochemicals Corp. Ltd

- 6.4.4 GrowTech Agri Science Private Limited

- 6.4.5 Gujarat Narmada Valley Fertilizers & Chemicals Ltd

- 6.4.6 Gujarat State Fertilizers & Chemicals Ltd

- 6.4.7 Prabhat Fertilizer And Chemical Works

- 6.4.8 Southern Petrochemical Industries Corp. Ltd

- 6.4.9 Swaroop Agrochemical Industries

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日