|

市場調査レポート

商品コード

1687239

米国の電気自動車(EV)用充電機器:市場シェア分析、産業動向、成長予測(2025~2030年)US Electric Vehicle (EV) Charging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の電気自動車(EV)用充電機器:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

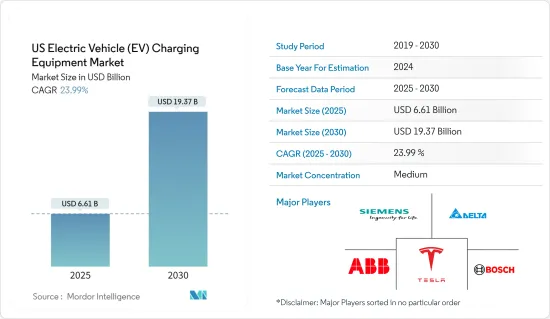

米国の電気自動車(EV)用充電器市場規模は2025年に66億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは23.99%で、2030年には193億7,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、国内における電気自動車の普及拡大や電気自動車インフラの開発といった要因が、予測期間中の充電機市場を牽引すると見込まれます。

- その一方で、充電ステーションの設置に伴う設置コストやメンテナンスコストの高さが、予測期間中の市場成長の妨げになると予想されます。

- EVへの投資の増加とEV充電装置の技術進歩は、予測期間中、米国の電気自動車充電装置市場に大きなビジネス機会をもたらすと期待されています。

米国の電気自動車充電機市場の動向

同国における電気自動車の普及拡大

- 電気自動車は、そのエコフレンドリー性質と費用対効果の高さから、ますます人気が高まっています。しかし、EV所有者にとっての主要懸念事項の1つは、充電ステーションの利用可能性です。電気自動車の利用が増加するにつれて、そのニーズを満たすためにより多くの充電設備やインフラが必要となります。

- 電気自動車の普及が進むにつれ、充電装置や関連インフラのニーズは拡大しています。需要を満たすため、政府や会社は駐車場、ショッピングモール、高速道路などの公共エリアに充電ステーションを設置するよう取り組んでいます。また、電気自動車の所有者の多くは、個人使用のために自宅に充電ステーションを設置しています。

- 国際エネルギー機関(IEA)によると、米国では2022年に電気自動車の販売台数が2021年比で55%増加し、バッテリー電気自動車(BEV)が牽引しました。BEVの販売台数は70%増加し、約80万台に達し、2019~2020年にかけて落ち込んだ後、2年連続で堅調な伸びを確認しました。PHEVの販売台数も15%増にとどまったもの、増加しました。

- 米国エネルギー省科学局によると、2023年12月中に米国で販売されたプラグイン車は合計14万1,055台(BEV 10万928台、PHEV 4万127台)で、2022年12月の販売台数から42.4%増加しました。また、2023年12月に米国で販売されたHEVは11万7,690台(乗用車3万1,825台、LT8万5,865台)で、2022年12月比70.3%増となりました。電気自動車の総ストックは2022年に300万台となり、2021年比で36%以上増加し、世界全体の10%を占めました。

- 2023年2月、バイデン超党派インフラ法の下、国は電気自動車用充電に75億米ドル、クリーン輸送に100億米ドル、電気自動車バッテリー部品、重要鉱物、材料に70億米ドル以上を投資する計画を発表しました。

- さらに、自動車メーカーとバッテリーメーカーは、37のEVバッテリー専用製造施設に500億米ドル以上を投じる計画です。総設備容量では654GWhの生産が可能で、これは2030年までに年間約1,000万台の小型車をサポートし、電気自動車の製造と販売を支えるのに十分な容量です。これらの投資はすべて、米国全土でEVの普及を後押しすると考えられます。その結果、予測期間中にEV充電装置とインフラのニーズが高まることになります。

- したがって、同国における電気自動車の普及と投資の増加は、EV充電装置の需要を加速し続け、予測期間にわたって有望な市場を維持すると予想されます。

市場を独占するバッテリー電気自動車。

- バッテリー電気自動車(BEV)は、一般に電気モーターを搭載した電気自動車とも呼ばれます。この車両は、電気モーターに電力を供給するために大型のトラクション・バッテリー・パックを使用します。EVは、壁のコンセントまたは電気自動車供給設備(EVSE)と呼ばれる充電設備に接続する必要があります。

- BEVは完全な電気自動車であり、通常、内燃機関(ICE)、燃料タンク、排気管を含まないです。推進力は電気だけに頼っています。車両のエネルギーはバッテリーパックから供給され、グリッドから充電されます。BEVはゼロ・エミッション車であり、従来のガソリン車による有害なテールパイプ排出や大気汚染の危険はないです。

- 米国では、バッテリー電気自動車(BEV)の普及が加速し、自動車産業に変革をもたらしています。技術の進歩、政府の支援、環境問題への関心の高まりにより、BEVは気候変動という課題に対処し、化石燃料への依存を減らす有望なソリューションとして浮上しました。

- 近年、米国ではバッテリー電気自動車の採用が大幅に増加しました。バッテリー技術の向上、航続距離の延長、充電インフラの急増により、当初の参入障壁を克服することができました。Tesla、Chevrolet、Nissan、Fordなどの自動車メーカーは、幅広い消費者にアピールする手頃な価格のモデルを提供し、BEVの普及に大きな役割を果たしました。

- 2022年、米国では99万台の電気自動車が新規登録され、そのうち約80%がBEVでした。国際エネルギー機関(IEA)によると、米国におけるバッテリー電気自動車(BEV)の販売台数は2021年比で40%増加しました。

- 米国エネルギー省によると、公的に利用可能な電気自動車用充電ポイント(レベル1、レベル2、DC急速)の数は、2022年の14万3,729から2023年には17万5,547に増加しました。2023年の充電ポイント数17万5,547カ所のうち、約13万7,795カ所が低速充電ポイントであり、残りの3万7,752カ所が急速充電ポイントでした。国内では近年、一般に利用可能な急速充電ポイントの割合が大きく伸びています。予測期間中も同じ傾向が続くと予想されます。

- 技術が進化し続ける中、米国におけるバッテリー電気自動車の将来は有望です。自動車メーカーは米国政府とともに、バッテリーの効率改善、コスト削減、車両全体の性能向上のための研究開発に多額の投資を行っています。

- 例えば、2022年第3四半期には、同国はEVとバッテリー製造に約2,100億米ドルを投資しました。Teslaは2022~2024年にかけて、米国とドイツに毎年60億~80億米ドルを投じるなど、投資の増加が見込まれています。さらに、自動車メーカーとバッテリーメーカーも、国内37カ所のEVバッテリー製造施設に540億米ドルの支出を計画しています。これらの施設では、2030年までに年間654ギガワット時(GWh)のEVバッテリー容量が生産される見込みです。このようなシナリオは、BEV製造産業に好影響を与えると予想されます。

- さらに、自律走行技術とビークル・ツー・グリッドの統合の出現は、BEVが輸送部門に革命をもたらす可能性をさらに高めています。これにより、バッテリー電気自動車用充電装置の需要が高まっている

米国の電気自動車用充電機産業概要

米国の電気自動車充電機市場は半分断されています。同市場の主要企業(順不同)には、ABB Ltd、Robert Bosch GmbH、Delta Electronics Inc.、Siemens AG、Tesla Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及と関連投資の増加

- 政府の支援施策とイニシアティブ

- 抑制要因

- 電気自動車用充電ステーションの設置にかかる高コスト

- 促進要因

- サプライチェーン分析

- PESTLE分析

第5章 市場セグメンテーション

- 車種

- バッテリー電気自動車(BEV)

- プラグインハイブリッド車(PHEV)

- ハイブリッド電気自動車(HEV)

- 用途

- 家庭用充電

- 職場充電

- 公共充電

- 充電タイプ

- AC充電(レベル1とレベル2)

- DC充電

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- ABB Ltd.

- Robert Bosch GmbH

- ChargePoint Inc.

- Enphase Energy, Inc.

- Delta Electronics Inc.

- Powercharge

- Siemens AG

- Tesla Inc.

- KOSTAL Automobil Elektrik GmbH & Co. KG.

- Webasto SE

- 市場ランキング分析

第7章 市場機会と今後の動向

- EV充電機の技術進歩

目次

Product Code: 56960

The US Electric Vehicle Charging Equipment Market size is estimated at USD 6.61 billion in 2025, and is expected to reach USD 19.37 billion by 2030, at a CAGR of 23.99% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors like the growing adoption of electric vehicles in the country and the development of electric vehicle infrastructure are expected to drive the charging equipment market during the forecast period.

- On the other hand, high installation costs associated with setting up charging stations and maintenance costs are expected to hinder the market's growth during the forecast period.

- Nevertheless, increasing investments in EVs and technological advancements in EV charging Equipment are expected to provide significant opportunities for the US electric vehicle (EV) charging equipment market during the forecast period.

US Electric Vehicle (EV) Charging Equipment Market Trends

Increasing Adoption of Electric Vehicles in the Country

- Electric vehicles (EVs) became increasingly popular due to their eco-friendly nature and cost-effective benefits. However, one of the main concerns for EV owners is the availability of charging stations. As the usage of electric vehicles increases, more charging equipment and infrastructures are required to fulfill the need.

- As the adoption of electric vehicles increases, the need for charging devices and relevant infrastructure is expanding. To meet the demand, the government and companies work on installing more charging stations in public areas such as parking lots, malls, and highways. Many electric vehicle owners also install charging stations in their homes for personal use.

- According to the International Energy Agency (IEA), in the United States, electric car sales increased by 55% in 2022 relative to 2021, led by battery electric vehicles (BEV). Sales of BEVs increased by 70%, reaching nearly 800,000 and confirming a second consecutive year of solid growth after the 2019-2020 dip. Sales of PHEVs also grew, albeit by only 15%.

- According to the United States Department of Energy Office of Science, a total of 141,055 plug-in vehicles (100,928 BEVs and 40,127 PHEVs) were sold during December 2023 in the United States, up 42.4% from the sales in December 2022. Also, In December 2023, 117,690 HEVs (31,825 cars and 85,865 LTs) were sold in the United States, up 70.3% from the sales in December 2022. The total stock of electric cars stood at 3 million in 2022, recording more than a 36% increase compared to 2021, accounting for 10% of the global total.

- In February 2023, Under Biden's Bipartisan Infrastructure Law, the country announced its plan to invest USD 7.5 billion in electric vehicle charging, USD 10 billion in clean transportation, and over USD 7 billion in electric vehicle (EV) battery components, critical minerals, and materials.

- Furthermore, the automakers and battery makers plan to spend over USD 50 billion across 37 dedicated EV battery manufacturing facilities. At total capacity, the facilities could produce 654 GWh in capacity, which is enough to support about 10 million light-duty vehicles annually by 2030 to support their electric vehicle manufacturing and sales. All these investments are likely to boost the adoption of EVs across the United States. It, in turn, is driving the need for EV charging devices and infrastructures over the forecast period.

- Hence, the increasing adoption of electric vehicles (EVs) and investments in the country are expected to continue accelerating the demand for EV charging equipment and hold a promising market over the forecast period.

Battery Electric Vehicles to Dominate the market.

- Battery electric vehicles (BEVs) are also commonly referred to as electric vehicles with an electric motor. The vehicle uses a large traction battery pack to power the electric motor. The EV must be plugged into a wall outlet or charging equipment called electric vehicle supply equipment (EVSE).

- BEVs are fully electric vehicles and typically do not include an internal combustion engine (ICE), fuel tank, or exhaust pipe. They rely only on electricity for propulsion. The vehicle's energy comes from the battery pack, which is recharged from the grid. BEVs are zero-emission vehicles, as they do not generate any harmful tailpipe emissions or air pollution hazards caused by traditional gasoline-powered vehicles.

- The United States is transforming the automotive industry as battery electric vehicles (BEVs) gain momentum and popularity. With technological advancements, government support, and increasing environmental concerns, BEVs emerged as a promising solution to address the challenges of climate change and reduce reliance on fossil fuels.

- In recent years, the adoption of battery-electric vehicles in the United States grew significantly. Improved battery technology, extended driving ranges, and a surge in charging infrastructure helped overcome the initial entry barriers. Automakers like Tesla, Chevrolet, Nissan, and Ford played instrumental roles in popularizing BEVs, offering affordable models that appeal to a broader range of consumers.

- In 2022, the United States registered 990,000 new electric cars, of which about 80% were BEVs, and witnessed a rise of 70% compared to 2021. According to the International Energy Agency (IEA), battery electric vehicle (BEV) sales increased by 40% in the United States relative to 2021.

- According to the United States Department of Energy, the number of publicly available electric vehicle charging points (Level 1, Level 2, and DC Fast) grew from 143,729 in 2022 to 175,547 in 2023. Of the 175,547 charging points in 2023, around 137,795 were slow charging points, and the rest 37,752 were fast charging points. The share of publicly available fast charging points witnessed significant growth in the country in recent years. It is expected to continue the same trend during the forecast period.

- As technology continues to evolve, the future of battery-electric vehicles in the United States looks promising. Automakers, along with the United States government, are investing heavily in research and development to improve battery efficiency, reduce costs, and enhance overall vehicle performance.

- For instance, in Q3 2022, the country invested nearly USD 210 billion in EV and battery manufacturing. The investment is expected to increase, with Tesla including USD 6-8 billion annually in the United States and Germany between 2022 and 2024. Further, automakers and battery makers also planned to spend USD 54 billion across 37 EV battery manufacturing facilities across the country. These facilities are expected to produce 654 gigawatt hours (GWh) of EV battery capacity annually by 2030. Such a scenario is expected with a positive impact on the BEV manufacturing industry.

- Moreover, the emergence of autonomous driving technology and vehicle-to-grid integration further adds to the potential of BEVs to revolutionize the transportation sector. It is thereby driving the demand for charging equipment for battery electric vehicles.

US Electric Vehicle (EV) Charging Equipment Industry Overview

The US electric vehicle (EV) charging equipment market is semi-fragmented. Some of the key players in the market (not in any particular order) include ABB Ltd, Robert Bosch GmbH, Delta Electronics Inc., Siemens AG, and Tesla Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles and Related Investments

- 4.5.1.2 Supportive Government Policies And Initiatives

- 4.5.2 Restraints

- 4.5.2.1 High Cost Of Setting Up Ev Charging Stations

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Battery Electric Vehicle (BEV)

- 5.1.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.1.3 Hybrid Electric Vehicle (HEV)

- 5.2 Application

- 5.2.1 Home Charging

- 5.2.2 Workplace Charging

- 5.2.3 Public Charging

- 5.3 Charging Type

- 5.3.1 AC Charging (Level 1 and Level 2)

- 5.3.2 DC Charging

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd.

- 6.3.2 Robert Bosch GmbH

- 6.3.3 ChargePoint Inc.

- 6.3.4 Enphase Energy, Inc.

- 6.3.5 Delta Electronics Inc.

- 6.3.6 Powercharge

- 6.3.7 Siemens AG

- 6.3.8 Tesla Inc.

- 6.3.9 KOSTAL Automobil Elektrik GmbH & Co. KG.

- 6.3.10 Webasto SE

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in the EV Charging Equipment