|

市場調査レポート

商品コード

1693731

中東の飼料用アミノ酸-市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Middle East Feed Amino Acids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東の飼料用アミノ酸-市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 204 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

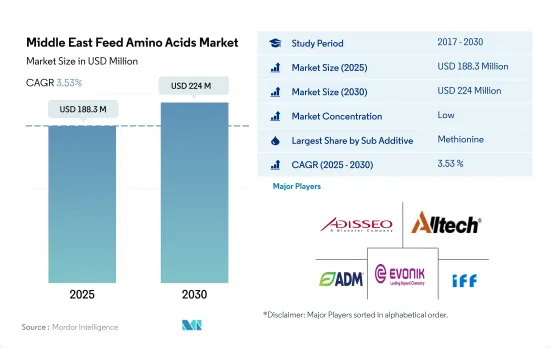

中東の飼料用アミノ酸市場規模は2025年に1億8,830万米ドルと推定され、2030年には2億2,400万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは3.53%で成長する見込みです。

- 中東地域では、動物飼料におけるアミノ酸の需要が増加しています。アミノ酸は動物の成長、筋肉の発達、肉の生産性向上に不可欠です。2022年の中東におけるアミノ酸の市場規模は、同地域の飼料添加物市場全体の20.4%でした。しかし、口蹄疫、アフリカ豚熱、鳥インフルエンザなどの動物伝染病の発生により、市場規模は2018~2021年の間に変動しました。

- 中東ではメチオニンとリジンが最も重要な飼料用アミノ酸であり、2022年の総市場額の63.5%以上を占めました。これらのアミノ酸は、腸の健康状態の改善、効率的な消化、肉生産量の増加など、動物の効率向上に寄与しています。トリプトファンもこの地域では重要なアミノ酸であり、予測期間中にCAGR 3.7%を記録すると予想されています。トリプトファンは希少であるため市場シェアは最も低いが、動物の早期成長と飼料消費量の増加には不可欠です。

- スレオニンも動物の健康に欠かせないアミノ酸であり、その市場規模は2022年の2,740万米ドルから2029年には3,500万米ドルに増加すると予測されています。食肉と食肉製品の需要の増加と、腸内pHのバランス調整と感染予防におけるアミノ酸の使用に対する意識の高まりが、この地域の飼料用アミノ酸市場を牽引すると予想されます。同市場は予測期間中にCAGR 3.5%を記録すると予想され、動物飼料産業における成長と投資の大きな可能性を示しています。

- 中東の飼料添加物市場は、2022年に飼料用アミノ酸のシェア値20.4%を記録し、2020~2022年には3.7%増加しました。2019~2020年の市場の落ち込みは、COVID-19の影響によるもので、世界貿易と現地のサプライチェーンが混乱し、その年の飼料生産が減少しました。

- 中東の飼料用アミノ酸市場では、サウジアラビアが2022年に6,070万米ドルを占めて最大の市場シェアを占め、次いでイランが4,560万米ドルの市場シェアを占めています。サウジアラビアは、同地域の他の国に比べて動物飼料への飼料添加物の採用率が高いことが、消費量の多さに寄与しています。

- 中東で消費される飼料用アミノ酸の最大シェアを占めるのは家禽類で、2022年のシェア値は58%でした。反芻動物は市場の38.9%を占めています。家禽肉の需要はサウジアラビアやイランのような国々で高く、2021年にはこの地域の家禽鳥の59%が飼育されました。

- イランだけで中東の配合飼料生産の45%以上を占め、2022年には全動物タイプで約2,400万トンを生産します。同国は畜産人口が多く、2021年には同地域の反芻家畜の18%を超えます。

- 中東では食肉需要の高まりと、動物用飼料における健康的な食生活への意識の高まりが見られ、飼料用アミノ酸の使用量の増加につながっています。同地域の市場は、予測期間中(2023~2029年)に3.5%の力強いCAGRで推移すると予測されています。

中東の飼料用アミノ酸市場動向

中東地域では、家禽の一人当たり消費量の増加に伴う新規農場の設立により、家禽セクタが拡大し、家禽生産の需要が増加しています。

- 中東では、養鶏業は農業セクタの中で最大のセグメントです。2022年には同地域の家畜頭数の90%を占めていました。この部門は大きな成長を遂げ、2022年の生産量は2017年比で10.9%増加しました。同地域における食肉と卵製品の需要増加が、この成長の主要原動力となっています。加えて、観光、ビジネス旅行、ホテル・レストラン・施設(HRI)部門からの需要が、2022年の鶏肉生産量の前年比2.5%増に寄与しました。この生産量の増加は、家禽生産に使用される飼料添加物の金額も2.9%上昇させました。

- 増大する需要に対応するため、中東諸国は養鶏部門に投資して生産を拡大しています。例えば、サウジアラビアのAlmaraiは、11億2,000万米ドルを投資して工場と新しい農場を設立し、鶏肉生産を拡大しようとしています。2022年、サウジアラビアの環境・水・農業省は275件の家禽プロジェクトライセンスを発行し、そのうち119件がブロイラープロジェクト、26件が年間20億個以上の卵生産能力、12件がブロイラー母鶏の繁殖・生産と年間4億8,050万羽の雛の生産能力を持つ孵化場の運営となっています。

- 同地域の鶏肉製品の一人当たり消費量も、2017年の44.9kgから2022年には45.5kgへと増加しており、増産需要をさらに押し上げています。その結果、養鶏産業への投資の増加や鶏肉製品の需要拡大といった要因が、予測期間中も家禽動物生産の成長を促進すると予想されます。

サウジアラビア、オマーン、アラブ首長国連邦などの政府は、大規模養殖場の設立に投資しており、この地域における水産飼料の需要を増加させると考えられます。

- 中東の養殖産業は近年著しい成長を遂げ、養殖飼料の需要増加につながりました。2017~2022年の間に、この種の飼料の需要は25.1%増加しました。この成長は、同地域の養殖産業が拡大し、養殖種の生産が増加したためです。2022年には、養殖用飼料の生産量はこの地域の総飼料生産量の2.1%を占め、合計50万トンとなります。イランはこの地域で最大の養殖飼料生産国で、2022年の生産量は28万トンでした。この高い生産量は、同国の強力な養殖生産によるもので、さまざまな種類の養殖種を養殖するための淡水資源の利用可能性から恩恵を受けています。

- 魚類はこの地域で生産される最大の養殖種であり、2022年の養殖飼料生産量の78.6%を占めます。サウジアラビア、オマーン、アラブ首長国連邦などの国々は、養殖に投資し、国際的な専門家や組織と提携して、生産性の高い地元養殖場を設立しています。例えば、湾岸地域の水産養殖団体は、英国湾岸海洋環境パートナーシップ(GMEP)プログラムを通じて、英国政府の環境漁業・水産養殖科学センター(Cefas)と協力し、魚類養殖の改善と生物多様性の損失に取り組んでいます。

- オマーンとアラブ首長国連邦は、この地域で養殖魚種の一人当たり消費量が最も多く、その消費量は一人当たり年間28.6kgに達します。輸出を減らし、国内生産を増やすため、オマーン政府は、漁業・養殖業を補助金部門から同国経済への重要な貢献へと転換させることを目指しています。

中東の飼料用アミノ酸産業概要

中東の飼料用アミノ酸市場は細分化されており、上位5社で36.01%を占めています。同市場の主要企業は以下の通りです。Adisseo、Alltech、Inc.、Archer Daniel Midland Co.、Evonik Industries AG、IFF(Danisco Animal Nutrition)などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 動物頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 養豚

- 規制の枠組み

- イラン

- サウジアラビア

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ添加物

- リジン

- メチオニン

- スレオニン

- トリプトファン

- その他のアミノ酸

- 動物

- 水産養殖

- サブアニマル別

- 魚類

- エビ

- その他の養殖種

- 家禽類

- 小動物別

- ブロイラー

- レイヤー

- その他の鳥類

- 反芻動物

- 小動物別

- 肉牛

- 乳牛

- その他の反芻動物

- 豚

- その他の動物

- 水産養殖

- 国名

- イラン

- サウジアラビア

- その他の中東地域

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Adisseo

- Alltech, Inc.

- Archer Daniel Midland Co.

- Evonik Industries AG

- IFF(Danisco Animal Nutrition)

- Kemin Industries

- Marubeni Corporation(Orffa International Holding B.V.)

- Novus International, Inc.

- Saudi Mix

- SHV(Nutreco NV)

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 93765

The Middle East Feed Amino Acids Market size is estimated at 188.3 million USD in 2025, and is expected to reach 224 million USD by 2030, growing at a CAGR of 3.53% during the forecast period (2025-2030).

- The Middle Eastern region is experiencing an increasing demand for amino acids in animal feed. Amino acids are essential for animal growth, muscle development, and improved meat productivity. In 2022, the market value of amino acids in the Middle East was 20.4% of the total feed additives market in the region. However, the market value fluctuated between 2018-2021 due to the occurrence of infectious animal diseases such as foot and mouth disease, African swine fever, and Avian influenza.

- Methionine and lysine were the most significant feed amino acids in the Middle East, accounting for over 63.5% of the total market value in 2022. These amino acids have been attributed to greater efficiency in animals, such as improved gut health, efficient digestion, and higher meat output. Tryptophan is also a significant amino acid in the region, and it is expected to register a CAGR of 3.7% during the forecast period. Although it has the lowest market share due to its scarcity, it is essential for early animal growth and increased feed consumption.

- Threonine is another crucial amino acid for animal health, and its market value is projected to increase from USD 27.4 million in 2022 to USD 35 million by 2029. The increasing demand for meat and meat products and the growing awareness of amino acid usage in balancing gut pH and preventing infection is expected to drive the region's feed amino acids market. The market is expected to register a CAGR of 3.5% during the forecast period, indicating a significant potential for growth and investment in the animal feed industry.

- The Middle Eastern feed additives market registered a 20.4% share value for feed amino acids in 2022, with an increase of 3.7% during 2020-2022. The dip in the market in 2019-2020 was due to COVID-19, which disrupted global trade and local supply chains, causing reduced feed production in those years.

- Saudi Arabia held the largest market share in the Middle Eastern feed amino acids market, accounting for USD 60.7 million in 2022, followed by Iran with a market share of USD 45.6 million. Saudi Arabia's high adoption of feed additives in animal diets compared to other countries in the region contributes to its high consumption.

- Poultry birds accounted for the largest share of feed amino acids consumed in the Middle East, with a 58% share value in 2022. Ruminants accounted for 38.9% of the market. The demand for poultry meat is high in countries like Saudi Arabia and Iran, where 59% of the region's poultry birds were raised in 2021.

- Iran alone accounted for over 45% of the compound feed production in the Middle East, producing around 24 million metric tons for all animal types in 2022. The country has a high animal population, with over 18% of ruminant cattle in the region in 2021.

- The Middle East is witnessing a rising demand for meat and increased awareness of healthy diets in animal feeds, leading to the increased usage of feed amino acids. The market in the region is expected to register a strong CAGR of 3.5% during the forecast period (2023-2029).

Middle East Feed Amino Acids Market Trends

Expanding poultry sector in the Middle East region with establishment of new farms with increasing per capita consumption of poultry has been increasing the demand for poultry production

- In the Middle East, the poultry industry is the largest segment in the agriculture sector. It represented 90% of the animal headcount in the region in 2022. The sector experienced significant growth, with production increasing by 10.9% in 2022 compared to 2017. The rise in demand for meat and egg products in the region has been the primary driver of this growth. Additionally, the demand from tourism, business travel, and the hotels, restaurants, and institutional (HRI) sector contributed to a 2.5% increase in poultry production in 2022 compared to the previous year. This increased production also led to a 2.9% rise in the value of feed additives used in poultry production.

- To meet the growing demand, Middle Eastern countries are investing in their poultry sectors to expand production. Saudi Arabia's Almarai company, for example, is investing USD 1.12 billion to establish a factory and new farms to increase poultry production. In 2022, the Saudi Arabian Ministry of Environment, Water, and Agriculture issued 275 poultry project licenses, including 119 for broiler projects, 26 for egg production with a capacity of more than two billion eggs per year, and 12 for breeding and producing broiler mothers and operating hatcheries with a capacity of 480.5 million chicks per year.

- The per capita consumption of poultry products in the region also increased, from 44.9 kg in 2017 to 45.5 kg in 2022, further driving the demand for increased production. As a result, factors such as increasing investment in the poultry industry and growing demand for poultry products are expected to continue to fuel the growth of poultry animal production during the forecast period.

Government in the countries such as Saudi Arabia, Oman and the United Arab Emirates invested to establish large fish farms which will increase the demand for aqua feed in the region

- The aquaculture industry in the Middle East experienced significant growth in recent years, leading to increased demand for aquaculture feed. Between 2017 and 2022, demand for this type of feed increased by 25.1%. This growth is due to the expansion of the aquaculture industry in the region, which led to increased production of aquaculture species. In 2022, aquaculture feed production accounted for 2.1% of total feed production in the region, totaling 0.5 million metric tons. Iran was the largest producer of aquaculture feed in the region, with a production of 0.28 million metric tons in 2022. This high production is attributed to the country's strong aquaculture production, which benefits from the availability of freshwater resources for cultivating different types of aquaculture species.

- Fish were the largest aquaculture species produced in the region, accounting for 78.6% of aquaculture feed production in 2022. Countries such as Saudi Arabia, Oman, and the United Arab Emirates have invested in aquaculture and partnered with international experts and organizations to establish productive local fish farms. For example, aquaculture organizations in the Gulf region are working with the UK Government's Centre for Environment Fisheries and Aquaculture Science (Cefas) through the UK Gulf Marine Environment Partnership (GMEP) Programme to improve fish farming and tackle biodiversity loss.

- Oman and the United Arab Emirates have the highest per capita consumption of aquaculture species in the region, with consumption reaching 28.6 kg per person per year. In an effort to reduce exports and increase domestic production, the Omani government aims to transform the fisheries and aquaculture industry from a subsidy sector to a significant contributor to the country's economy.

Middle East Feed Amino Acids Industry Overview

The Middle East Feed Amino Acids Market is fragmented, with the top five companies occupying 36.01%. The major players in this market are Adisseo, Alltech, Inc., Archer Daniel Midland Co., Evonik Industries AG and IFF(Danisco Animal Nutrition) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Iran

- 4.3.2 Saudi Arabia

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Additive

- 5.1.1 Lysine

- 5.1.2 Methionine

- 5.1.3 Threonine

- 5.1.4 Tryptophan

- 5.1.5 Other Amino Acids

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 Country

- 5.3.1 Iran

- 5.3.2 Saudi Arabia

- 5.3.3 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Adisseo

- 6.4.2 Alltech, Inc.

- 6.4.3 Archer Daniel Midland Co.

- 6.4.4 Evonik Industries AG

- 6.4.5 IFF(Danisco Animal Nutrition)

- 6.4.6 Kemin Industries

- 6.4.7 Marubeni Corporation (Orffa International Holding B.V.)

- 6.4.8 Novus International, Inc.

- 6.4.9 Saudi Mix

- 6.4.10 SHV (Nutreco NV)

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms