|

市場調査レポート

商品コード

1693713

中東の民間航空機客室用座席:市場シェア分析、産業動向、統計、成長動向予測(2025年~2030年)Middle East Commercial Aircraft Cabin Seating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東の民間航空機客室用座席:市場シェア分析、産業動向、統計、成長動向予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 111 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

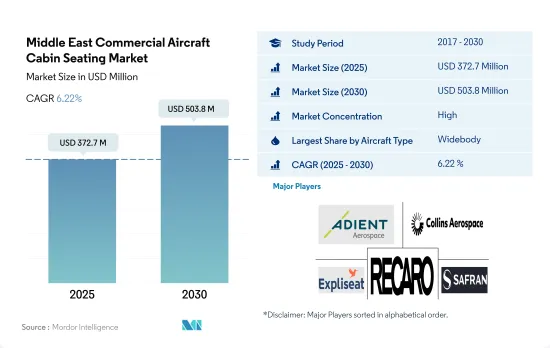

中東の民間航空機用客室用座席の市場規模は2025年に3億7,270万米ドルと推定され、2030年には5億380万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは6.22%で成長する見込みです。

ワイドボディ機への需要の高まりと、乗客の快適性とプライバシーを重視する航空会社により、中東の客室用座席の需要が促進される見込みです。

- 中東の航空産業は、観光客の増加、経済開発、航空会社の増便などを背景に、長年にわたり着実に成長を続けています。この成長の重要な側面の一つが客室用座席市場であり、乗客の快適性と航空会社の収益性を確保する上で極めて重要です。中東では航空旅行の人気が高まり続けているため、航空会社は乗客の快適性を高め、座席数を最大化するための革新的な方法を常に模索しています。この地域の客室用座席市場の需要は、様々な航空会社が調達する新しい航空機によって牽引されています。納入数では、中東ではワイドボディ機が圧倒的に多く、2017~2022年の全体シェアは52%でした。

- 中東の航空会社による長距離路線でのナローボディ機の採用が増加し、ナローボディ機への人間工学的シートの配備を後押ししています。Emiratesなどの航空会社は、ビジネスクラスの座席数を増やし、顧客体験を向上させることに注力しています。この地域の航空会社は、軽量シートの採用に重点を置き始めています。

- 2023~2030年の間に、サウジアラビア、カタール、アラブ首長国連邦などの主要市場を中心に、この地域で約543機のナローボディ機と401機のワイドボディ機の納入が見込まれています。同地域における航空機の拡大計画は、ナローボディ機とワイドボディ機の調達を促進すると予想されます。その結果、予測期間中に同地域の民間航空機客室用座席市場の成長を8.30%押し上げると期待されます。

アラブ首長国連邦は、同地域の航空会社が大量の航空機を発注しているため、同地域でより大きな成長が見込まれています。

- 航空会社にとって、顧客体験は常に最優先事項です。不満足な顧客や離反した顧客は、必然的に乗客の減少を招き、航空会社の利益を減少させています。旅客にとって、いつ旅行してもポジティブな体験をしてもらうことは不可欠です。最高の体験を提供するため、中東の航空会社は、旅行中に乗客に快適さと全体的な楽しさを提供する客室用座席の近代化に力を入れています。中東の航空会社は、航空機全体の重量を軽減するため、より軽量なシートの採用に乗り出しています。このアップグレードはまた、効率を改善し、客室スペースの有効活用を促進します。

- 同地域の航空機客室用座席市場の需要を牽引しているのは、様々な航空会社が機材更新の一環として発注している航空機であり、長距離で燃費の良い航空機の必要性です。エア・アラビア、エミレーツ航空、エティハド航空、カタール航空、サウディア、リヤド航空、フライドバイなどの大手航空会社は、合計391機のナローボディ機と413機のワイドボディ機を発注しています。これらの航空機のうち、Emirates、エティハド航空、フライドバイといったアラブ首長国連邦のトップ航空会社は361機を発注しています。アラブ首長国連邦は、その巨大な航空機受注に牽引され、より大きな成長を遂げると予想されます。これらの受注航空機は予測期間を通じて納入される見込みであり、これらの航空機受注が航空機座席市場の需要を牽引すると予想されます。Boeing社によると、中東は今後20年間で巨大な拡大が見込まれ、急成長する旅客輸送に対応するために約3,400機のジェット機が必要となります。このような要因により、この地域の航空機シート市場の需要は、2023~2030年の間に8.30%増加すると予想されます。

中東の民間航空機キャビンシート市場動向

市場成長の主要因は、中東諸国における航空機保有機数の拡大と旅客航空需要の増加

- 中東の航空産業はその他よりも早く、かつ強力にCOVID-19パンデミックから回復しました。2021年には中東の航空旅客数は3億200万人に達し、2020年比で249%、2019年比で25%の伸びを示しました。航空旅客数の増加は、最終的に航空機の新規調達を促進し、同地域の客室内装品市場を押し上げる可能性があります。大手航空会社は機材拡大戦略を採用しています。

- 2017~2022年にかけて、この地域では合計498機の航空機が新たに納入されました。2023~2030年には、この地域で約1,058機の航空機が新たに納入される見込みです。予測期間中、航空機の大半はナローボディになると予想されます。また、小型で経済的な航空機の人気、格安航空会社の成功、航続距離の長いナローボディの登場などが、この動向に拍車をかけています。サウジアラビアとアラブ首長国連邦が、航空機納入数の多くを占める主要国です。

- この地域のさまざまな航空会社が、LEDキャビンライト、ワイヤレス軽量IFES、快適で軽量なシート、その他のキャビン製品など、先進的な航空機システムやコンポーネントを選択しているため、新しい航空機の納入や受注残は、客室内装品の需要を生み出すと予想されます。2022年11月現在、Emirates、カタール航空、サウディア・アラビア航空、エティハド航空、フライドバイ航空などの大手航空会社は、合わせて1,013機以上の航空機を発注済みであり、そのうち589機がナローボディ・ジェットであると予想されています。このような要因が、予測期間中、客室内装品市場をプラスに牽引すると予想されます。

一貫した航空旅行の成長が中東の航空旅客輸送量の原動力

- 国際的な旅行者や貿易の中継地として人気の高い中東は、ビジネス客やレジャー客の出発地や目的地としても成長しています。2020年、中東の航空旅客輸送量は、COVID-19パンデミックによる渡航制限のため64%減少しました。しかし2022年には、ワクチン接種率の上昇とホリデーシーズンの旺盛な需要により、同地域の航空旅客輸送量は3億4,950万人に達し、2021年比で16%の伸びを示したが、2019年比では45%の伸びでした。アラブ首長国連邦やサウジアラビアなどの主要国が航空旅客輸送量全体の42%を占め、他の中東諸国と比較して新型機に対する高い需要を生み出しました。

- 2022年の旅客輸送能力は2021年比で73.8%増加し、旅客搭乗率は24.6%増の75.8%となりました。同地域の航空旅行回復は引き続き勢いを増しており、航空旅客輸送量は今後20年以内に倍増すると予想されています。バーレーン、クウェート、オマーン、サウジアラビア、アラブ首長国連邦、イラク、イラン、ヨルダン、イエメン、カタールの中東主要国際路線地域の多くは、すでにCOVID-19以前の水準を上回っています。こうしたことは、航空旅行が回復し、勢いを増し続けていることを示しています。中東内でも、多くの主要国際路線がすでにCOVID-19以前の水準を上回っています。観光と旅行意欲の高さが、中東・アフリカにおける航空産業の回復を引き続き後押ししています。航空旅客輸送量は、2022年と比較して2030年には34%増加すると予想されています。

中東の民間航空機客室用座席産業の概要

中東の民間航空機客室用座席市場はかなり統合されており、上位5社で88.57%を占めています。この市場の主要企業は、Adient Aerospace、Collins Aerospace、Expliseat、Recaro Group、Safranなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 航空旅客輸送量

- 新規航空機納入数

- 一人当たりGDP(現行価格)

- 航空機メーカーの売上高

- 航空機受注残

- 受注総額

- 空港建設支出(継続中)

- 航空会社の燃料費

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 航空機タイプ

- ナローボディ

- ワイドボディ

- 国名

- サウジアラビア

- アラブ首長国連邦

- その他の中東地域

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Adient Aerospace

- Collins Aerospace

- Expliseat

- Recaro Group

- Safran

- STELIA Aerospace(Airbus Atlantic Merginac)

- ZIM Aircraft Seating GmbH

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 93609

The Middle East Commercial Aircraft Cabin Seating Market size is estimated at 372.7 million USD in 2025, and is expected to reach 503.8 million USD by 2030, growing at a CAGR of 6.22% during the forecast period (2025-2030).

Rising demand for widebody aircraft and airlines focusing on passenger comfort and privacy is expected to drive the demand for cabin seating in the Middle East

- The aviation industry in the Middle East has been steadily growing over the years, driven by increased tourism, economic development, and the expansion of airline fleets. One crucial aspect of this growth is the cabin seat market, which is pivotal in ensuring passenger comfort and airline profitability. As air travel continues to gain popularity in the Middle East, airlines constantly seek innovative ways to enhance passenger comfort and maximize seating capacity. The region's demand for cabin seating market is driven by new aircraft procured by various airlines. In terms of deliveries, widebody aircraft dominated the number of deliveries in the Middle East, with an overall share of 52% during 2017-2022.

- The adoption of narrowbody aircraft in the longer haul routes by the Middle East airlines has increased, aiding the deployment of ergonomic seats in narrowbody aircraft. The airlines such as Emirates have focused on increasing their business class seats and improving customer experience. The airlines in the region have started emphasizing the adoption of lighter seats.

- Around 543 narrowbody aircraft and 401 widebody aircraft are expected to be delivered in the region with major markets such as Saudi Arabia, Qatar, and the United Arab Emirates during 2023-2030. The fleet expansion plans in the region are expected to aid the procurement of narrowbody and widebody aircraft. This will, in turn, be expected to drive the growth of the region's commercial aircraft cabin seating market during the forecast period by 8.30%.

The UAE is expected to witness a larger growth in the region because of huge aircraft orders placed by the countries' airlines

- Customer experience is always the top priority for airlines. Dissatisfied or disengaged customers inevitably result in fewer passengers and reduced profits for airlines. It is vital for passengers to have a positive experience whenever they travel. To provide the best experience, airlines in the Middle East are focused on modernized cabin seats that provide comfort and overall enjoyment to passengers during their travel. Airlines in the Middle East have started adopting lighter seats for a reduction in the overall weight of aircraft. This upgrade will also improve efficiency and promote better utilization of cabin spaces.

- The demand for the aircraft cabin seating market in the region is driven by aircraft orders that are being placed by various airlines as part of fleet renewal and the need for long-range, fuel-efficient aircraft. Some of the major airlines, such as Air Arabia, Emirates, Etihad, Qatar Airways, Saudia, Riyadh Air, and Flydubai, have ordered a total of 391 narrowbody and 413 widebody aircraft. Of these total aircraft ordered, the UAE's top airlines, such as Emirates, Etihad, and Flydubai, have ordered 361 aircraft. The UAE is expected to witness a larger growth driven by its huge aircraft orders. These ordered aircraft are expected to be delivered throughout the forecast period, and these aircraft orders are expected to drive the demand for aircraft seating market. The Middle East is expected to see enormous expansion over the next 20 years, requiring a fleet of around 3,400 jets to serve fast-growing passenger traffic, according to Boeing. Factors such as these are expected to drive the demand in the region's aircraft seat market by 8.30% during 2023-2030.

Middle East Commercial Aircraft Cabin Seating Market Trends

The main reasons for market growth are the expansion of the fleet and the increased demand for passenger air travel in Middle Eastern countries

- The aviation industry in the Middle East recovered from the COVID-19 pandemic faster and stronger than the rest of the world. In 2021, air passenger traffic in the Middle East reached 302 million, a growth of 249% compared to 2020 and 25% compared to 2019. The increase in air passenger traffic may eventually drive new aircraft procurements, boosting the cabin interior market in the region. Major airlines have adopted fleet expansion strategies.

- A total of 498 new aircraft were delivered in the region between 2017 and 2022. During 2023-2030, around 1,058 new aircraft are expected to be delivered in the region. During the forecast period, the majority of aircraft are expected to be narrowbody. In addition, the popularity of small and economical aircraft, the success of low-cost carriers, and the advent of narrowbodies with long ranges have contributed to this trend. Saudi Arabia and the United Arab Emirates are the major countries accounting for a significant number of aircraft deliveries.

- New aircraft deliveries and backlogs are expected to generate demand for cabin interiors, as various airlines in the region are opting for advanced aircraft systems and components such as LED cabin lights, wireless lightweight IFES, comfortable, lightweight seats, and other cabin products. As of November 2022, major airlines, such as Emirates, Qatar Airways, Saudia Arabia Airlines, Etihad Airways, and FlyDubai Airlines, together had a backlog of over 1,013 aircraft, of which 589 were expected to be narrowbody jets. Factors such as these are expected to drive the cabin interior market positively during the forecast period.

Consistent growth in air travel is the driving factor for air passenger traffic in the Middle East

- The Middle East, a popular connection point for international travelers and trade, is also growing as a starting point and destination for business and leisure passengers. In 2020, air passenger traffic in the Middle East dropped by 64% due to travel restrictions caused by the COVID-19 pandemic. However, in 2022, due to the rising vaccination rates and strong demand over the holiday season, air passenger traffic in the region reached 349.5 million, a growth of 16% compared to 2021, while the growth was at 45% compared to 2019. Major countries, such as the United Arab Emirates and Saudi Arabia, accounted for 42% of the total air passenger traffic, generating higher demand for new aircraft compared to other Middle Eastern countries.

- In 2022, passenger capacity increased by 73.8%, and passenger load factor grew by 24.6% to 75.8% compared to 2021. Air travel recovery in the region continues to gather momentum, and air passenger traffic is expected to double within the next 20 years. Many major Middle Eastern international route areas in Bahrain, Kuwait, Oman, Saudi Arabia, the United Arab Emirates, Iraq, Iran, Jordan, Yemen, and Qatar are already exceeding pre-COVID-19 levels. Such factors indicate that air travel has recovered and continues to gather momentum. Many major international routes, even within the Middle East, are already exceeding pre-COVID-19 levels. Tourism and the high willingness to travel continue to foster the industry's recovery in the Middle East & Africa. The air passenger traffic levels are expected to grow by 34% in 2030 compared to 2022.

Middle East Commercial Aircraft Cabin Seating Industry Overview

The Middle East Commercial Aircraft Cabin Seating Market is fairly consolidated, with the top five companies occupying 88.57%. The major players in this market are Adient Aerospace, Collins Aerospace, Expliseat, Recaro Group and Safran (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 New Aircraft Deliveries

- 4.3 GDP Per Capita (current Price)

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.2 Country

- 5.2.1 Saudi Arabia

- 5.2.2 United Arab Emirates

- 5.2.3 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Adient Aerospace

- 6.4.2 Collins Aerospace

- 6.4.3 Expliseat

- 6.4.4 Recaro Group

- 6.4.5 Safran

- 6.4.6 STELIA Aerospace (Airbus Atlantic Merginac)

- 6.4.7 ZIM Aircraft Seating GmbH

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms