|

市場調査レポート

商品コード

1693712

中東の民間航空機客室インテリア:市場シェア分析、産業動向、統計、成長動向予測(2025~2030年)Middle East Commercial Aircraft Cabin Interior - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東の民間航空機客室インテリア:市場シェア分析、産業動向、統計、成長動向予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 171 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

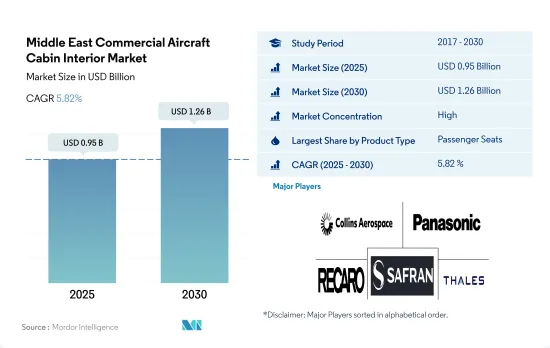

中東の民間航空機客室インテリア市場規模は2025年に9億5,000万米ドルと予測され、2030年には12億6,000万米ドルに達し、予測期間(2025~2030年)のCAGRは5.82%で成長すると予測されます。

旅客機用シートが37.2%で最大シェア

- 中東の民間航空機客室インテリア市場は、製品タイプ別にシート、客室照明、機内エンターテインメントシステム、窓、ギャレーと化粧室、その他の製品タイプに区分されます。同地域の航空会社は、乗客の全体的な快適性と体験を向上させるため、これらの製品の実用性を高めることに注力しています。

- ビジネスクラス利用者の増加により、エコノミークラスよりも広い開発スペースを持つ座席構造の充実が不可欠となっています。中東の航空会社とOEMは、2050年のゼロエミッション目標を考慮し、航空機の軽量化と航空産業のサステイナブル経営方法の開発への取り組みを強化しています。

- この地域の航空会社は、効率、信頼性、耐久性、重量の面で既存の客室内照明のさまざまな欠点を解消するため、先進的なLED照明を採用しています。このように、LED照明ソリューションの進歩に伴い、様々なOEMが従来の客室照明よりもLED照明を採用しています。この地域の主要航空会社は、民間航空機の機内エンターテインメントシステムに4K技術を採用しています。航空機の調達数が急増していることから、予測期間中、中東の旅客航空セクタでは民間航空機の客室インテリアの需要が高まると予想されます。

アラブ首長国連邦市場は同地域で最も高い成長が見込まれる

- 航空会社にとって、顧客体験は常に最優先事項です。最高の体験を提供するため、中東の航空会社は新しい近代化された客室内装に力を入れており、安全で快適な、より美的感覚に優れた環境を高空で乗客に提供しています。

- 航空旅客数の増加により、新たな航空機の調達が促進され、客室インテリアの需要が高まると予想されます。中東の航空会社の2022年の輸送量は、2021年と比較して157.4%増加しました。輸送能力は73.8%増加し、搭乗率は24.6%上昇して75.8%に達しました。2022年12月の需要は、2021年同月比で69.8%増加しました。アラブ首長国連邦、サウジアラビア、カタールなどの主要国は、中東市場における航空旅客輸送量全体の55%を占めています。したがって、これらの国々の成長は、他の中東諸国と比較して、新型航空機に対するより高い需要を生み出すと予想されます。

- 同地域の主要航空会社は、632機の民間航空機を発注しました。このうち、エア・アラビアはA320neoを73機、A321neoを27機、A321XLRを20機、EmiratesはA350-900を50機、B777Xを115機、B787-9を30機、エティハド航空はA321neoを26機、A350-1,000を15機、6機、B777-9型機11機、BB787-10型機21機、カタール航空は737Max10型機25機、B777-9型機40機、B787-10型機23機、フライドバイはB737Max8型機33機、B737Max9型機67機、B737Max10型機50機を発注しました。

- これらの納入により、機内インテリアの需要が高まり、この地域のさまざまな航空会社が、LED機内照明、ワイヤレス軽量IFES、快適で軽量なシート、その他の機内製品など、先進的な航空機システムやコンポーネントを選択しています。

中東の民間航空機客室インテリア市場の動向

一貫した空の旅の成長が中東の航空旅客輸送量の原動力

- 国際旅行や貿易の中継地として人気の高い中東は、ビジネス客やレジャー客の出発地や目的地としても成長しています。2020年、中東の航空旅客輸送量は、COVID-19パンデミックによる渡航制限のため64%減少しました。しかし2022年には、ワクチン接種率の上昇とホリデーシーズンの旺盛な需要により、同地域の航空旅客輸送量は3億4,950万人に達し、2021年比で16%の伸びを示したが、2019年比では45%の伸びでした。アラブ首長国連邦やサウジアラビアなどの主要国が航空旅客輸送量全体の42%を占め、他の中東諸国と比較して新型機に対する高い需要を生み出しました。

- 2022年の旅客輸送能力は2021年比で73.8%増加し、旅客搭乗率は24.6%増の75.8%となりました。同地域の航空旅行回復は引き続き勢いを増しており、航空旅客輸送量は今後20年以内に倍増すると予想されています。バーレーン、クウェート、オマーン、サウジアラビア、アラブ首長国連邦、イラク、イラン、ヨルダン、イエメン、カタールの中東主要国際路線地域の多くは、すでにCOVID-19以前の水準を上回っています。こうしたことは、航空旅行が回復し、勢いを増し続けていることを示しています。中東内でも、多くの主要国際路線がすでにCOVID-19以前の水準を上回っています。観光と旅行意欲の高さが、中東・アフリカにおける産業の回復を引き続き促進しています。航空旅客輸送量は、2022年と比較して2030年には34%増加すると予想されています。

サウジアラビア、域内で最も高い一人当たりGDPを記録

- 中東の2022年のGDPは8兆3,200億米ドルで、2021年比で21%、2020年比で42%の伸びを記録しました。地域全体のGDPのうち、サウジアラビアが2022年に8,330億米ドルと最も高く、アラブ首長国連邦の4,090億米ドル、カタールの1,790億米ドルがこれに続きます。特にサウジアラビアの航空輸送産業は202億米ドル、アラブ首長国連邦は193億米ドルがGDPに寄与しています。

- サウジアラビアはGDPと一人当たりGDPで第1位です。2022年10月現在、同国のGDPは1兆100億米ドル、1人当たりGDPは2万7,940米ドルを記録しました。業績の改善は石油部門の拡大によるもので、2022年第2四半期の成長率は23.1%でした。非石油民間部門の成長率は、前年同期の4.5%から2022年第2四半期には5.4%となりました。

- アラブ首長国連邦の2022年のGDPは5,039億1,000万米ドル、国民1人当たりは4万7,790米ドルを記録しました。炭化水素はアラブ首長国連邦経済において引き続き重要な役割を担っており、同国のGDPの30%が石油・ガス産業、13%が輸出に直接依存しています。

- カタールは2022年に2,213億7,000万米ドルを記録し、1人当たりGDPは6万8,620米ドルでした。GDPと一人当たりGDPの上昇は主にカタールの石油・天然ガス資源によるもので、2021年上半期の193億4,000万米ドルに対し、3,229億8,000万米ドルの収益を記録しました。ほとんどの部門における利益の増加は、最終的にこの地域の一人当たりGDPを押し上げ、それによって航空輸送産業を牽引し、その関連部門に対する需要を生み出す可能性があります。

中東の民間航空機客室インテリア産業の概要

中東の民間航空機客室インテリア市場はかなり統合されており、上位5社で67.35%を占めています。この市場の主要企業は、Collins Aerospace、Panasonic Avionics Corporation、Recaro Group、Safran、Thales Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 航空旅客輸送量

- 新規航空機納入数

- 一人当たりGDP(現行価格)

- 航空機メーカーの売上高

- 航空機受注残

- 受注総額

- 空港建設支出(継続中)

- 航空会社の燃料費

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 製品タイプ

- キャビンライト

- 機内窓

- 機内エンターテインメントシステム

- 乗客シート

- その他

- 航空機タイプ

- ナローボディ

- ワイドボディ

- 客室クラス

- ビジネスクラスとファーストクラス

- エコノミークラスとプレミアムエコノミークラス

- 運航国

- サウジアラビア

- アラブ首長国連邦

- その他の中東地域

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Adient Aerospace

- Astronics Corporation

- Collins Aerospace

- Diehl Aerospace GmbH

- Expliseat

- FACC AG

- GKN Aerospace Service Limited

- Jamco Corporation

- Luminator Technology Group

- Panasonic Avionics Corporation

- Recaro Group

- Safran

- SCHOTT Technical Glass Solutions GmbH

- STG Aerospace

- Thales Group

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Middle East Commercial Aircraft Cabin Interior Market size is estimated at 0.95 billion USD in 2025, and is expected to reach 1.26 billion USD by 2030, growing at a CAGR of 5.82% during the forecast period (2025-2030).

Passenger seats accounted for the largest share of 37.2% in the market

- The Middle Eastern commercial aircraft cabin interior market is segmented by product type into seats, cabin lighting, in-flight entertainment systems, windows, galleys and lavatories, and other product types. Airlines in the region are focusing on increasing the utility of these products to improve overall passenger comfort and experience.

- An enhanced seating structure with more developed space than economy-class seats is becoming highly essential due to the rising number of business-class travelers. Middle Eastern airline operators and OEMs are increasing their efforts to reduce aircraft weight and develop a sustainable way to manage the airline industry in consideration of the zero-emission 2050 goal.

- Airlines in the region are adopting advanced LED lighting to eliminate various drawbacks of existing interior cabin lights in terms of efficiency, reliability, durability, and weight. Thus, with the advancement in LED lighting solutions, various OEMs are adopting them over conventional cabin lighting. Major airlines in the region are adopting 4K technology in their in-flight entertainment systems in their active fleet of commercial aircraft. The surging number of aircraft procurements is expected to boost the demand for commercial aircraft cabin interiors in the Middle Eastern passenger aviation sector during the forecast period.

The UAE market is expected to witness the highest growth in the region

- Customer experience is always a top priority for airlines. To provide the best experience, Middle Eastern airlines are focusing on new modernized cabin interiors, providing passengers with a secure, comfortable, and more aesthetically pleasing environment at high altitudes.

- The increase in air passenger traffic is expected to drive new aircraft procurements, thus creating demand for cabin interiors. Middle Eastern airlines registered a 157.4% traffic rise in 2022 compared to 2021. Their capacity increased by 73.8%, while the load factor increased by 24.6% to reach 75.8%. In December 2022, the demand grew by 69.8% compared to the same month in 2021. Major countries, such as the United Arab Emirates, Saudi Arabia, and Qatar, accounted for 55% of the total air passenger traffic in the Middle Eastern market. Hence, growth in these countries is expected to generate a higher demand for new aircraft compared to other Middle Eastern countries.

- Major airlines in the region have registered total orders for 632 commercial aircraft. Of this total, Air Arabia ordered 73 A320neo, 27 A321neo, and 20 A321XLR, Emirates ordered 50 A350-900, 115 B777X, and 30 B787-9, Etihad ordered 26 A321neo, 15 A350-1000, 6 B777-9, 11 B787-9, and 21 BB787-10, Qatar Airways ordered 25 737 Max 10, 40 B777-9, and 23 B787-10, and Flydubai ordered 33 B737 Max 8, 67 B737 Max 9, and 50 B737 Max 10.

- With these deliveries, the demand for cabin interiors has increased, and various airlines in the region are opting for advanced aircraft systems and components such as LED cabin lights, wireless lightweight IFES, comfortable, lightweight seats, and other cabin products.

Middle East Commercial Aircraft Cabin Interior Market Trends

Consistent growth in air travel is the driving factor for air passenger traffic in the Middle East

- The Middle East, a popular connection point for international travelers and trade, is also growing as a starting point and destination for business and leisure passengers. In 2020, air passenger traffic in the Middle East dropped by 64% due to travel restrictions caused by the COVID-19 pandemic. However, in 2022, due to the rising vaccination rates and strong demand over the holiday season, air passenger traffic in the region reached 349.5 million, a growth of 16% compared to 2021, while the growth was at 45% compared to 2019. Major countries, such as the United Arab Emirates and Saudi Arabia, accounted for 42% of the total air passenger traffic, generating higher demand for new aircraft compared to other Middle Eastern countries.

- In 2022, passenger capacity increased by 73.8%, and passenger load factor grew by 24.6% to 75.8% compared to 2021. Air travel recovery in the region continues to gather momentum, and air passenger traffic is expected to double within the next 20 years. Many major Middle Eastern international route areas in Bahrain, Kuwait, Oman, Saudi Arabia, the United Arab Emirates, Iraq, Iran, Jordan, Yemen, and Qatar are already exceeding pre-COVID-19 levels. Such factors indicate that air travel has recovered and continues to gather momentum. Many major international routes, even within the Middle East, are already exceeding pre-COVID-19 levels. Tourism and the high willingness to travel continue to foster the industry's recovery in the Middle East & Africa. The air passenger traffic levels are expected to grow by 34% in 2030 compared to 2022.

Saudi Arabia records the highest GDP per capita in the region

- The Middle East registered a GDP of USD 8,320 billion in 2022, a growth of 21% compared to 2021 and 42% compared to 2020. Of the total region's GDP, Saudi Arabia recorded the highest GDP at USD 833 billion in 2022, followed by the United Arab Emirates at USD 409 billion and Qatar at USD 179 billion. In particular, the air transport industry in Saudi Arabia contributed USD 20.2 billion, whereas the United Arab Emirates contributed USD 19.3 billion to the GDP.

- Saudi Arabia ranks first in terms of GDP and GDP per capita. As of October 2022, the country recorded USD 1.01 trillion in GDP and USD 27.94 thousand in GDP per capita. The improved performance was due to a stronger expansion in the oil sector, which grew by 23.1% in Q2 2022. The growth in the non-oil private sector was 5.4% in Q2 2022, from 4.5% in the previous quarter of the same year.

- The United Arab Emirates recorded a GDP of USD 503.91 billion in 2022 and USD 47.79 thousand per capita. Hydrocarbons continue to play a critical role in the UAE economy, with 30% of the country's GDP directly based on the oil and gas industry and 13% of its exports.

- Qatar recorded USD 221.37 billion in 2022 and USD 68.62 thousand in GDP per capita. The rise in GDP and GDP per capita was primarily due to Qatar's oil and natural gas resources, which recorded a revenue of USD 322.98 billion compared to USD 19.34 billion in the first half of 2021. The rise in profit in most sectors may eventually boost the region's GDP per capita, thereby driving the air transportation industry and creating demand for its associated sectors.

Middle East Commercial Aircraft Cabin Interior Industry Overview

The Middle East Commercial Aircraft Cabin Interior Market is fairly consolidated, with the top five companies occupying 67.35%. The major players in this market are Collins Aerospace, Panasonic Avionics Corporation, Recaro Group, Safran and Thales Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 New Aircraft Deliveries

- 4.3 GDP Per Capita (current Price)

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product Type

- 5.1.1 Cabin Lights

- 5.1.2 Cabin Windows

- 5.1.3 In-Flight Entertainment System

- 5.1.4 Passenger Seats

- 5.1.5 Other Product Types

- 5.2 Aircraft Type

- 5.2.1 Narrowbody

- 5.2.2 Widebody

- 5.3 Cabin Class

- 5.3.1 Business and First Class

- 5.3.2 Economy and Premium Economy Class

- 5.4 Country

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Adient Aerospace

- 6.4.2 Astronics Corporation

- 6.4.3 Collins Aerospace

- 6.4.4 Diehl Aerospace GmbH

- 6.4.5 Expliseat

- 6.4.6 FACC AG

- 6.4.7 GKN Aerospace Service Limited

- 6.4.8 Jamco Corporation

- 6.4.9 Luminator Technology Group

- 6.4.10 Panasonic Avionics Corporation

- 6.4.11 Recaro Group

- 6.4.12 Safran

- 6.4.13 SCHOTT Technical Glass Solutions GmbH

- 6.4.14 STG Aerospace

- 6.4.15 Thales Group

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms