欧州の民間航空機機客室インテリア:市場シェア分析、産業動向、成長予測(2025年~2030年)

Europe Commercial Aircraft Cabin Interior - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 167 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685902

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

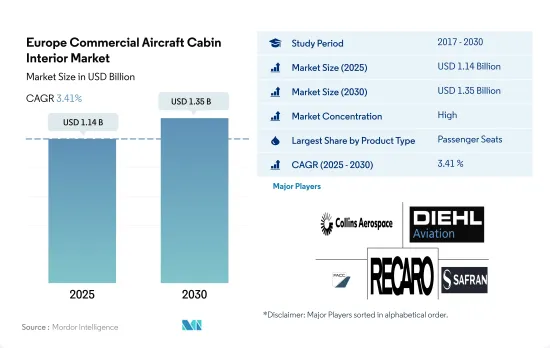

欧州の民間航空機機客室インテリア市場規模は2025年に11億4,000万米ドルと推定・予測され、2030年には13億5,000万米ドルに達し、予測期間(2025年~2030年)のCAGRは3.41%で成長すると予測されます。

欧州の航空会社は機内インテリアの新技術を導入しており、同分野の新製品開発や技術革新に役立つと期待されています。

- 欧州の民間航空機客室インテリア市場は、シート、客室照明、機内エンターテインメントシステム、窓、調理室、化粧室、その他の製品タイプに区分されています。同地域の航空会社は、これらの製品の実用性を高めると同時に、乗客の全体的な快適性と体験を向上させることを重視しています。

- エコノミークラスの座席よりも開発スペースの広い充実した座席構造は、ビジネスクラス利用者の嗜好が高まっているため、非常に不可欠なものとなっています。欧州の航空会社およびOEMは、2050年のゼロ・エミッションの目標を考慮し、軽量化と持続可能な航空産業の経営方法を開発する努力を強めています。

- 航空会社は、乗客の体験を向上させるため、先進的な室内照明を備えた客室の近代化に力を入れています。次世代航空機にLED環境照明技術が広く採用されたことで、機内で一貫したサービス品質を維持するための客室近代化活動が可能になりました。この地域の航空会社は、効率、信頼性、耐久性、重量の面で既存の客室内照明のさまざまな欠点を解消するのに役立つため、先進的なLED照明に移行しています。様々なOEMが、従来の機内灯よりも先進的なLED照明を保有しています。

- エア・欧州、エールフランス、ブリティッシュ・エアウェイズ、イベリア航空といった欧州の大手航空会社は、機内エンターテインメント・システムをスクリーンの品質や機能の面で改善しました。2023年から2030年にかけて、この地域ではおよそ2,500機の旅客機が納入される見込みです。航空機調達数の急増は、予測期間中に欧州の旅客航空セクターにおける民間航空機機客室インテリアの需要を押し上げると予想されます。

格安航空会社の普及と旅客の客室体験向上のニーズが市場の成長を後押しすると予想される

- 航空機の客室内装は、旅客体験全体の重要な要素へと進化しています。欧州の航空会社は現在、旅客体験を向上させるために客室の近代化に注力しています。

- 旅客輸送量の増加が航空機の新規調達需要を牽引し、客室内装品市場をさらに押し上げています。例えば、2022年の欧州全体の航空旅客輸送量は13億人に達し、2021年比で8%の伸びとなりました。欧州の航空会社は、主要国での航空旅客輸送量の増加に対応するため、機体拡張計画を実施しています。英国、ドイツ、スペインは、この地域の航空旅客輸送量全体の36%を占めています。したがって、航空旅客輸送量の増加は、他の欧州諸国と比較して、これらの国々で新しい航空機の需要を生み出すと予想されます。

- 航空旅客輸送量の増加は、最終的に航空機の受注と納入を押し上げる可能性があります。主要な民間航空機製造OEMであるボーイングとエアバスは、予測期間中にこの地域で多数の航空機を納入すると予想されます。同地域には2,800機以上の新型ジェット機が納入される見込みです。このうち2,500機以上がナローボディ機になると予想されるが、これは主に経済的な小型機への嗜好、LCCの成功、長距離ナローボディ機の導入によるものです。エールフランス航空、ブリティッシュ・エアウェイズ、ルフトハンザドイツ航空など、この地域の大手航空会社は、航空機内での全体的な乗客体験の向上に注力しており、この地域の民間航空機機客室インテリアの需要を後押ししています。

欧州の民間航空機客室インテリア市場の動向

航空旅客輸送量の伸びは、国内および国際航空旅行の需要増加によって支えられると予想されます。

- 2022年に欧州各国の渡航制限が徐々に緩和されたことで、欧州大陸内の移動はCOVID-19流行時よりもはるかに容易になりました。この動向により、国際線需要が急増し、封鎖期間中に旅行できなかった旅客は、国内で休暇を取る代わりに再び海外へ飛びました。2022年、欧州全体の航空旅客数は13億人に達し、2021年比で8%の伸びを示しました。英国、ドイツ、スペインは、欧州の航空旅客輸送量全体の36%を占めており、したがって、今後数年間は、他の欧州諸国と比較して、新型航空機に対するより多くの需要を生み出す可能性があります。また、欧州の航空会社は、世界の国際航空旅客数の40%近くを輸送しています。

- 2022年1~6月期の欧州の空港利用者数は2021年比で247%増加し、その結果、欧州大陸全体で6億6,000万人の旅客が増加しました。英国、オランダ、トルコ、ドイツは、最も利用者の多い空港を擁し、2022年上半期の旅客数は大幅な伸びを記録しました。2022年8月、欧州の上位5空港の旅客輸送量は68.1%増加したが、主にアジアで旅行制限が続いたため、流行前の2019年8月の水準を17.5%下回る水準にとどまりました。その他欧州の空港でも、2022年8月に同様の航空旅客輸送量の増加が見られました。ウクライナの空港からは商業航空輸送量が減少し、ベラルーシとロシアの空港でもロシア・ウクライナ戦争が始まって以来、旅客数の減少が記録されました。2023年から2030年にかけての航空旅客輸送量は、国内および国際航空需要の増加により、31%急増すると予想されます。

欧州連合(EU)で実施されている経済開発イニシアティブは、一人当たりGDPの伸びを助長すると予想されます。

- 欧州地域の2022年のGDPは17兆米ドルで2番目に高いです。地域全体のGDPのうち、オランダの成長率は19%と最も高いです。一方、フランスやドイツといった他の主要国の成長率はそれぞれ10%、14%でした。GDP全体のうち、英国の航空輸送産業は年間約870億米ドル、フランスは約860億米ドル、ドイツは約680億米ドルの貢献をしています。

- EU全体の一人当たりGDPは、2023年には約3万9,000米ドルでした。英国、フランス、ドイツを含むこの地域の主要国の一人当たりGDPは、パンデミック以前の水準に戻りました。英国、ドイツ、フランスの一人当たりGDPは、2019年と比較して2022年にはそれぞれ約15%、9%、7%急増しました。2014年から2020年までの結束政策プログラムのピークが、2021年から2027年までのプログラムの開始と並行することで、地域全体の人々や企業への絶え間ない投資の流れが保証されます。COVID-19の大流行以来、レジリエンスと社会的・地域的成長を強化するために、結束政策プログラムを通じて1,860億ユーロ以上が支払われました。航空旅行の普及率は、一人当たりGDPと相関関係があります。国民1人当たりのGDPが高い国ほど、国民1人当たりの航空座席数が多い傾向があります。ドイツの1人当たりGDPは5万1,100米ドルとこの地域で最も高く、2017年から2022年にかけて14%増加しました。フランスの1人当たりGDPは2017年から2022年にかけて12%増加し、英国のそれは同じ5年の期間内に22%増加しました。主要経済圏と全欧州にわたるこのような成長事例は、予測期間中、欧州の航空業界を支援すると予想されます。

欧州の民間航空機機客室インテリア産業の概要

欧州の民間航空機機客室インテリア市場はかなり統合されており、上位5社で68.91%を占めています。この市場の主要企業は以下の通り。 Collins Aerospace, Diehl Aerospace GmbH, FACC AG, Recaro Group and Safran(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 航空旅客輸送量

- 新規航空機納入数

- 一人当たりGDP(現行価格)

- 航空機メーカーの売上高

- 航空機受注残

- 受注総額

- 空港建設支出(継続中)

- 航空会社の燃料費

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 製品タイプ

- キャビンライト

- 機内窓

- 機内エンターテインメントシステム

- 乗客シート

- その他の製品タイプ

- 航空機タイプ

- ナローボディ

- ワイドボディ

- 客室クラス

- ビジネスクラスおよびファーストクラス

- エコノミークラスおよびプレミアムエコノミークラス

- 運航国

- フランス

- ドイツ

- スペイン

- トルコ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Astronics Corporation

- Collins Aerospace

- Diehl Aerospace GmbH

- FACC AG

- GKN Aerospace Service Limited

- Jamco Corporation

- Panasonic Avionics Corporation

- Recaro Group

- Safran

- SCHOTT Technical Glass Solutions GmbH

- Thales Group

- Thompson Aero Seating

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The Europe Commercial Aircraft Cabin Interior Market size is estimated at 1.14 billion USD in 2025, and is expected to reach 1.35 billion USD by 2030, growing at a CAGR of 3.41% during the forecast period (2025-2030).

European airlines are new technologies in the aircraft cabin interiors that are expected to aid in new product developments and innovations in the segment

- The European commercial aircraft cabin interior market has been segmented into seats, cabin lighting, in-flight entertainment systems, windows, galley, lavatories, and other product types. The airline companies in the region are emphasizing increasing the utility of these products while improving the overall passenger comfort and experience.

- An enhanced seating structure with more developed space than economy-class seats is becoming highly essential due to the rising preferences for business-class travelers. European airline operators and OEMs are increasing their efforts to reduce weight and develop a sustainable way to manage the airline industry, considering the zero-emission 2050 goal.

- Airlines are focusing on modernized cabins with advanced interior lighting to improve the passenger experience. The widespread adoption of LED ambient lighting technology on next-generation aircraft has enabled cabin modernization activities to maintain a consistent service quality on board. Airlines in the region are moving toward advanced LED lighting as it helps the airlines eliminate various drawbacks of existing interior cabin lights in terms of efficiency, reliability, durability, and weight. Various OEMs possess advanced LED lighting over conventional aircraft cabin lights.

- Major European carriers, such as Air Europa, Air France, British Airways, and Iberia Airlines, improved their in-flight entertainment systems in terms of screen quality and features. Around 2,500 passenger aircraft are expected to be delivered in the region during 2023-2030. The surge in aircraft procurement numbers is expected to boost the demand for commercial aircraft cabin interior products in the European passenger aviation sector during the forecast period.

The proliferation of low-cost carriers and the need for enhanced passenger cabin experiences are expected to aid the market's growth

- Cabin interiors in aircraft have evolved into a prominent component of the overall passenger experience. European airline companies are now focusing on modernized cabins to improve the passenger experience.

- The increase in air passenger traffic is driving the demand for new aircraft procurements, further boosting the cabin interior market. For instance, in 2022, air passenger traffic in the whole of Europe amounted to 1.3 billion, a growth of 8% compared to 2021. Airline companies in Europe are implementing fleet expansion plans to cater to the growing air passenger traffic in the major countries. The United Kingdom, Germany, and Spain accounted for 36% of the total air passenger traffic in the region. Hence, the growing air passenger traffic is expected to generate demand for new aircraft in these countries compared to other European countries.

- The increasing air passenger traffic may eventually boost aircraft orders and deliveries. The major commercial aircraft manufacturing OEMs, i.e., Boeing and Airbus, are expected to deliver a large number of aircraft in the region over the forecast period. Over 2,800 new jets are expected to be delivered to the region. Of these, 2,500+ are expected to be narrowbody aircraft, primarily due to the preference for economical smaller aircraft, the success of LCCs, and the introduction of long-range narrowbody aircraft. The major airline companies in the region, such as Air France, British Airways, and Lufthansa, are focusing on improving the overall passenger experience in the aircraft, thus aiding the demand for commercial aircraft cabin interior products in the region.

Europe Commercial Aircraft Cabin Interior Market Trends

The growth in air passenger traffic is expected to be supported by the increasing demand for domestic and international air travel

- The gradual relaxation of travel restrictions in various European countries in 2022 made travel within the continent much easier than during the COVID-19 pandemic. Due to this trend, international demand soared, with passengers unable to travel during the lockdowns eager to fly abroad once again instead of taking domestic vacations. In 2022, air passenger traffic in the whole of Europe reached 1.3 billion, a growth of 8% compared to 2021. The United Kingdom, Germany, and Spain accounted for 36% of the total air passenger traffic in Europe and, hence, may generate more demand for new aircraft compared to other European countries over the coming years. European airlines have also been responsible for carrying almost 40% of global international air passengers.

- European airport traffic grew by 247% in the first six months of 2022 compared to 2021, resulting in an additional 660 million passengers handled across the continent. The United Kingdom, the Netherlands, Turkey, and Germany, which have some of the countries with the busiest airports, recorded a significant rise in passenger traffic in H1 2022. In August 2022, passenger traffic in the top five European airports increased by 68.1% but remained -17.5% below pre-pandemic August 2019 levels, mainly due to continued travel restrictions in Asia. A similar increase in air passenger traffic was observed at airports in the Rest of Europe in August 2022. Commercial air traffic declined from Ukrainian airports, and airports in Belarus and Russia recorded declining passenger volumes as well since the beginning of the Russia-Ukraine War. The air passenger traffic is expected to surge by 31% during 2023-2030, with increased demand in domestic and international aviation.

The economic development initiatives implemented in the European Union are expected to aid the GDP per capita income growth

- The European region had the second-highest GDP, with USD 17 trillion, in 2022. Out of the total region's GDP, the Netherlands recorded the highest growth rate, i.e., 19%. In contrast, other major countries such as France and Germany accounted for growth rates of 10% and 14%, respectively. Out of the total GDP, the air transport industry in the United Kingdom contributed around USD 87 billion annually, while France and Germany contributed around USD 86 billion and USD 68 billion, respectively.

- The GDP per capita income of the overall European Union was around USD 39,000 in 2023. The per capita GDP of the region's major economies, including the UK, France, and Germany, has returned to pre-pandemic levels. The GDP per capita income of the UK, Germany, and France surged by around 15%, 9%, and 7%, respectively, in 2022 as compared to 2019. The peak of the cohesion policy programs for the 2014-2020 period, in parallel to the start of the programs for the 2021- 2027 period, ensures a constant flow of investment into people and businesses across the region. Since the COVID-19 pandemic, more than EUR 186 billion has been paid out through cohesion policy programs to enhance resilience and social and regional growth. The penetration of air travel is correlated with the GDP per capita. Countries with higher GDP per capita tend to have higher numbers of airline seats per capita. Germany has the highest GDP per capita in the region at USD 51,100, which increased by 14% from 2017 to 2022. France's GDP per capita increased by 12% from 2017 to 2022, while that of the United Kingdom increased by 22% within the same five-year time frame. Such growth instances across major economies and pan-Europe are anticipated to aid the European airline industry during the forecast period.

Europe Commercial Aircraft Cabin Interior Industry Overview

The Europe Commercial Aircraft Cabin Interior Market is fairly consolidated, with the top five companies occupying 68.91%. The major players in this market are Collins Aerospace, Diehl Aerospace GmbH, FACC AG, Recaro Group and Safran (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 New Aircraft Deliveries

- 4.3 GDP Per Capita (current Price)

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product Type

- 5.1.1 Cabin Lights

- 5.1.2 Cabin Windows

- 5.1.3 In-Flight Entertainment System

- 5.1.4 Passenger Seats

- 5.1.5 Other Product Types

- 5.2 Aircraft Type

- 5.2.1 Narrowbody

- 5.2.2 Widebody

- 5.3 Cabin Class

- 5.3.1 Business and First Class

- 5.3.2 Economy and Premium Economy Class

- 5.4 Country

- 5.4.1 France

- 5.4.2 Germany

- 5.4.3 Spain

- 5.4.4 Turkey

- 5.4.5 United Kingdom

- 5.4.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Astronics Corporation

- 6.4.2 Collins Aerospace

- 6.4.3 Diehl Aerospace GmbH

- 6.4.4 FACC AG

- 6.4.5 GKN Aerospace Service Limited

- 6.4.6 Jamco Corporation

- 6.4.7 Panasonic Avionics Corporation

- 6.4.8 Recaro Group

- 6.4.9 Safran

- 6.4.10 SCHOTT Technical Glass Solutions GmbH

- 6.4.11 Thales Group

- 6.4.12 Thompson Aero Seating

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 167 Pages

- 納期

- 2~3営業日