|

市場調査レポート

商品コード

1693710

欧州の民間航空機客室用照明:市場シェア分析、産業動向、成長予測(2025~2030年)Europe Commercial Aircraft Cabin Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の民間航空機客室用照明:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 116 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

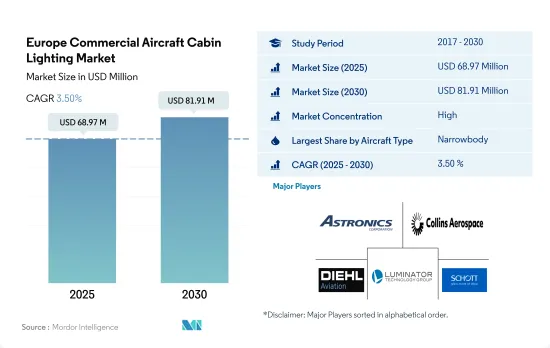

欧州の民間航空機客室用照明市場規模は、2025年に6,897万米ドルと推定され、2030年には8,191万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは3.50%で成長します。

この地域では、ナローボディ航空機の需要の増加と航空会社の台頭により、軽量化と乗客の全体的な体験の向上のため、洗練されたLED照明へのシフトが進んでいます。

- 最新世代の航空機のシートは、燃料費を削減し、航空機の持続可能性を高めるため、軽量で非金属の材料と軽量設計で作られています。ワイドボディ機と比較して、ナローボディ機はより積極的な成長率を示す可能性があります。2017~2022年にかけて、ナローボディ航空機は納入機数の大半を記録し、全体の82%を占めました。

- また、この地域の航空会社は、性能、信頼性、耐久性、重量の面で現在の客室内照明の欠点の多くを解消することから、高品質のLED照明への移行を進めています。次世代航空機にLEDアンビエント照明(LED)が広く導入されたことで、一貫したサービス品質を維持しながら客室の近代化活動を継続することができるようになりました。

- ほとんどの航空会社が乗客の体験を向上させるために革新的な客室用照明を選択しているため、さまざまな航空会社が発注する膨大な数の航空機が市場を牽引すると予想されます。ロステック航空、ライアンエアー、ウィズエアー、エールフランス航空、ルフトハンザドイツ航空、トルコ航空などの大手航空会社は、約670機の航空機を発注しています。このような巨大な航空機の発注は、予測期間中に航空機客室用照明の需要を押し上げると予想されます。

- 快適性と体験の向上を重視する傾向が強まっていることが、機内照明の需要を牽引しています。メンテナンスコストを削減し、従来のかさばる照明を近代的でコンパクトなLED照明ソリューションに置き換えるための絶え間ない技術革新は、航空機客室用照明市場の成長を助ける上で非常に重要です。

機内照明やその他の先進的機内照明製品における最先端技術の開発と導入は、欧州における航空機照明ソリューションのニーズを大幅に高めています。

- LEDムード照明、人間中心照明、その他の革新的な客室用照明製品などの新技術の革新と導入が、欧州における航空機照明システムの需要を大幅に促進しています。数色から選べる幅広い照明オプションは、航空会社や航空機メーカーが空の旅中の顧客の気分や体験を高め、時差ぼけを軽減するのに役立っています。

- この地域ではLCCの成功率が高いです。エールフランス航空、ブリティッシュ・エアウェイズ、ルフトハンザドイツ航空など、この地域の大手航空会社は、民間航空機市場における全体的な乗客体験の向上に注力しています。このことは、同地域における照明システムなどの民間航空機客室内装品の需要を助長する上で重要な役割を果たすと予想されます。

- 様々な航空会社が発注する相当数の航空機が市場を牽引すると予想されます。欧州の航空会社の大半は、移動中の乗客体験を向上させるために最先端の客室用照明を活用しています。ロシア航空、エア・ライアンエアー、ウィズ・エアーをはじめ、フランスのエールフランス航空、ドイツの航空会社、トルコ航空など、欧州の主要航空会社は合計670機の航空機を発注しています。ブリティッシュ・エアウェイズやアエロフロート航空など、他の大手航空会社の一部も、航空機に先進的なLEDムード照明を導入しています。ナローボディ機やワイドボディ機に対するこのような莫大な航空機発注と、より良い旅行体験のための新技術の導入は、予測期間中に航空機客室用照明の需要を生み出すと予想されます。

欧州の民間航空機客室用照明市場動向

航空旅行の回復や様々な航空会社による航空機の大量発注などの要因が市場の成長を促進しています。

- 中国と米国の間で続いている政治的緊張がBoeing社に影響を与えており、同社は現在、中国の顧客向けに発注した737 MAXジェット機の一部を再販する計画です。Boeingは、中国の航空会社がジェット機を発注しなくなり、厳しい状況に直面しています。中国の舟山にあるBoeingのデリバリーセンターは準備が整っており、737 MAXの納入を再開する予定です。舟山工場は年間100機の航空機を受け入れることができます。

- Airbusは2022年上半期に259件(442件)の新規純受注を記録したのに対し、今年累計では1,044件(1,080件)の新規純受注を記録しました。2022年には、Airbusは820件の新規受注(1,078件のグロス受注)を計上し、2021年のグロス受注と新規受注を上回りました。2022年、AirbusはBoeingにわずか46機という僅差で4年連続の受注王座を獲得しました。2021年、Airbusは合計771機のグロス受注を計上し、264機のキャンセルを受け、合計507機の純新規受注を獲得しました。2023年6月、Airbusは12社の顧客に902機を発注し、2機のA321neoのキャンセルを報告しました。

- 累計では、Boeingは415機(グロス527機)の新規受注を獲得し、昨年上半期の186機(グロス286機)を上回りました。2022年には、Boeingは2021年の479件(グロス909件)を上回る774件(グロス935件)の新規受注を計上しました。2023年6月現在、Boeingは9社の顧客から合計304機のジェット機(グロス受注)を予約しました。しかし、同社は16機の777Xのキャンセルも報告しており、その結果、288機の純新規受注となりました。

航空旅客輸送量の伸びは、国内と国際航空旅行の需要増に支えられると予想されます。

- 2022年に欧州各国で渡航制限が徐々に緩和されたことにより、欧州大陸内の移動はCOVID-19の流行時よりもはるかに容易になりました。この動向により、国際線需要が急増し、封鎖期間中に旅行できなかった旅客は、国内で休暇を取る代わりに再び海外へ飛びたがりました。2022年、欧州全体の航空旅客数は13億人に達し、2021年比で8%の伸びを示しました。英国、ドイツ、スペインは、欧州の航空旅客輸送量全体の36%を占めており、したがって、今後数年間は、他の欧州諸国と比較して、新型航空機に対するより多くの需要を生み出す可能性があります。また、欧州の航空会社は、世界の国際航空旅客数の40%近くを輸送しています。

- 2022年1~6月期の欧州の空港利用者数は2021年比で247%増加し、その結果、欧州大陸全体で6億6,000万人の旅客が増加しました。英国、オランダ、トルコ、ドイツは、最も利用者の多い空港を擁し、2022年上半期の旅客数は大幅な伸びを記録しました。2022年8月、欧州の上位5空港の旅客輸送量は68.1%増加したが、主にアジアで旅行制限が続いたため、流行前の2019年8月の水準を17.5%下回る水準にとどまりました。その他の欧州の空港でも、2022年8月に同様の航空旅客輸送量の増加が見られました。ウクライナの空港からは商業航空輸送量が減少し、ベラルーシとロシアの空港でもロシア・ウクライナ戦争が始まって以来、旅客数の減少が記録されました。2023~2030年にかけての航空旅客輸送量は、国内と国際航空需要の増加により31%急増すると予想されます。

欧州の民間航空機客室用照明産業概要

欧州の民間航空機客室用照明市場はかなり統合されており、上位5社で90.56%を占めています。この市場の主要企業は、Astronics Corporation、Collins Aerospace、Diehl Aerospace GmbH、Luminator Technology Group、SCHOTT Technical Glass Solutions GmbHなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 航空旅客輸送量

- 新規航空機納入数

- 一人当たりGDP(現行価格)

- 航空機メーカーの売上高

- 航空機受注残

- 受注総額

- 空港建設支出(継続中)

- 航空会社の燃料費

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 航空機タイプ

- ナローボディ

- ワイドボディ

- 国名

- フランス

- ドイツ

- スペイン

- トルコ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Astronics Corporation

- Collins Aerospace

- Diehl Aerospace GmbH

- Luminator Technology Group

- Safran

- SCHOTT Technical Glass Solutions GmbH

- STG Aerospace

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Europe Commercial Aircraft Cabin Lighting Market size is estimated at 68.97 million USD in 2025, and is expected to reach 81.91 million USD by 2030, growing at a CAGR of 3.50% during the forecast period (2025-2030).

The increasing demand for narrowbody aircraft and the emergence of airlines in the region are leading to a shift toward sophisticated LED lighting in order to reduce weight and improve the overall passenger experience

- Modern-generation aircraft seats are made from lightweight, non-metallic materials and lightweight designs to reduce fuel expenses and increase the aircraft's sustainability. Compared to widebody aircraft, narrowbody aircraft may witness a more aggressive growth rate. During 2017-2022, narrowbody aircraft recorded a majority of the deliveries, accounting for 82% of the total number of aircraft delivered.

- The region's airlines are also transitioning to high-quality LED lighting, as it eliminates many of the shortcomings of the current interior cabin lighting in terms of performance, dependability, durability, and weight. The widespread implementation of LED Ambient Lighting (LED) on next-generation aircraft has helped keep cabin modernization activities ongoing while maintaining consistent service quality.

- It is anticipated that the huge number of aircraft orders placed by various airlines will drive the market as most airlines are opting for innovative cabin lighting to enhance passengers' experience. Major airlines, such as Rostec, Ryanair, Wizz Air, Air France, Lufthansa, and Turkish Airlines, have ordered approximately 670 aircraft. Huge aircraft orders such as these are expected to boost the demand for aircraft cabin lighting during the forecast period.

- The rising emphasis on improving comfort and experience is driving the demand for aircraft cabin lighting. Constant innovations to reduce maintenance costs and replace traditionally bulky lighting with modern and compact LED lighting solutions are critical in aiding the growth of the aircraft cabin lighting market.

The development and implementation of cutting-edge technologies in cabin lighting and other advanced cabin lighting products are significantly increasing the need for aircraft lighting solutions in Europe

- The innovations and introduction of new technologies, such as LED mood lighting, human-centric lighting, and other innovative cabin lighting products, are significantly fueling the demand for aircraft lighting systems in Europe. A wide range of lighting options in several colors is aiding airlines and aircraft manufacturers in enhancing customers' moods and experiences during air travel and lessening jetlag.

- The success of LCCs is high in this region. Major airline companies in the region, such as Air France, British Airways, and Lufthansa, are focusing on improving the overall passenger experience in the commercial aircraft market. This is expected to play a vital role in aiding the demand for commercial aircraft cabin interior products such as lighting systems in the region.

- A considerable number of aircraft orders placed by various airlines is expected to drive the market. The majority of airlines in Europe are utilizing cutting-edge cabin lighting to improve the passenger experience while on the move. Major European carriers, such as Russian Airlines, Air Ryanair, and Wizz Air, as well as French Air France, German Airlines, and Turkey Airlines, have placed orders for a total of 670 aircraft. Some of the other major airlines, such as British Airways and Aeroflot, also implemented advanced LED mood lighting in their aircraft. Such huge aircraft orders for narrowbody and widebody aircraft and the implementation of new technologies for better travel experience are expected to create demand for aircraft cabin lighting during the forecast period.

Europe Commercial Aircraft Cabin Lighting Market Trends

Factors such as recovery in air travel and substantial aircraft orders being placed by various airlines are driving the growth of the market

- Ongoing political tensions between China and the United States have impacted Boeing, and it now plans to remarket some 737 MAX jets earmarked for Chinese customers. Boeing is facing a difficult situation as Chinese airlines are no longer ordering its jets. The Boeing delivery center in Zhoushan, China, is ready and is expected to resume delivery of 737 MAX aircraft. The Zhoushan plant can accommodate 100 aircraft annually.

- Year-to-date, Airbus accumulated 1,044 net new orders (1,080 gross orders), compared to 259 net new orders (442 gross orders) in the first half of 2022. In 2022, Airbus booked 820 net new orders (1,078 gross orders), surpassing both 2021 gross orders and net new orders. In 2022, Airbus won the orders crown for the fourth consecutive year by a fairly slim margin of just 46 aircraft compared to Boeing. In 2021, Airbus booked a total of 771 gross orders and received 264 cancellations, for a total of 507 net new orders. In June 2023, Airbus booked orders for a whopping 902 aircraft for 12 different customers and reported two A321neo cancellations, for a total of 900 net new orders.

- Year-to-date, Boeing accumulated 415 net new orders (527 gross orders), compared to 186 net new orders (286 gross orders) in the first six months of last year. In 2022, Boeing booked 774 net new orders (935 gross orders), up from 479 net new orders (909 gross orders) in 2021. As of June 2023, Boeing booked orders from nine customers for a total of 304 jets (gross orders). However, the company also reported 16 777X cancellations, resulting in 288 net new orders.

The growth in air passenger traffic is expected to be supported by the increasing demand for domestic and international air travel

- The gradual relaxation of travel restrictions in various European countries in 2022 made travel within the continent much easier than during the COVID-19 pandemic. Due to this trend, international demand soared, with passengers unable to travel during the lockdowns eager to fly abroad once again instead of taking domestic vacations. In 2022, air passenger traffic in the whole of Europe reached 1.3 billion, a growth of 8% compared to 2021. The United Kingdom, Germany, and Spain accounted for 36% of the total air passenger traffic in Europe and, hence, may generate more demand for new aircraft compared to other European countries over the coming years. European airlines have also been responsible for carrying almost 40% of global international air passengers.

- European airport traffic grew by 247% in the first six months of 2022 compared to 2021, resulting in an additional 660 million passengers handled across the continent. The United Kingdom, the Netherlands, Turkey, and Germany, which have some of the countries with the busiest airports, recorded a significant rise in passenger traffic in H1 2022. In August 2022, passenger traffic in the top five European airports increased by 68.1% but remained -17.5% below pre-pandemic August 2019 levels, mainly due to continued travel restrictions in Asia. A similar increase in air passenger traffic was observed at airports in the Rest of Europe in August 2022. Commercial air traffic declined from Ukrainian airports, and airports in Belarus and Russia recorded declining passenger volumes as well since the beginning of the Russia-Ukraine War. The air passenger traffic is expected to surge by 31% during 2023-2030, with increased demand in domestic and international aviation.

Europe Commercial Aircraft Cabin Lighting Industry Overview

The Europe Commercial Aircraft Cabin Lighting Market is fairly consolidated, with the top five companies occupying 90.56%. The major players in this market are Astronics Corporation, Collins Aerospace, Diehl Aerospace GmbH, Luminator Technology Group and SCHOTT Technical Glass Solutions GmbH (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 New Aircraft Deliveries

- 4.3 GDP Per Capita (current Price)

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 Spain

- 5.2.4 Turkey

- 5.2.5 United Kingdom

- 5.2.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Astronics Corporation

- 6.4.2 Collins Aerospace

- 6.4.3 Diehl Aerospace GmbH

- 6.4.4 Luminator Technology Group

- 6.4.5 Safran

- 6.4.6 SCHOTT Technical Glass Solutions GmbH

- 6.4.7 STG Aerospace

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms