|

市場調査レポート

商品コード

1693674

欧州のドライミックスモルタルの市場シェア分析、産業動向と統計、成長予測(2025~2030年)Europe Dry Mix Mortar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のドライミックスモルタルの市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 231 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

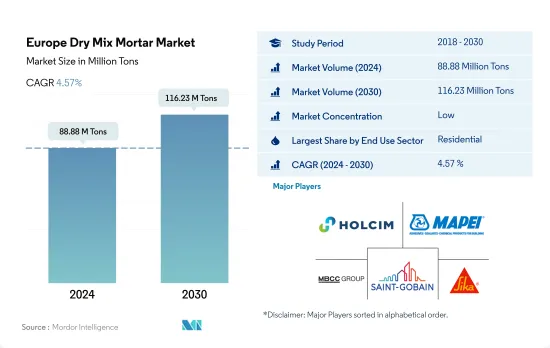

欧州のドライミックスモルタル市場規模は2024年に8,888万トンと推定され、2030年には1億1,623万トンに達し、予測期間中(2024~2030年)のCAGRは4.57%で成長すると予測されます。

欧州における改修の波の高まりがドライミックスモルタル市場の成長を押し上げる

- 2022年、欧州では最終用途部門全体でドライミックスモルタルの消費が5%増加し、前年を上回りました。特筆すべきは、商業セクタの消費量が最も急増したことです。2023年にはロシアとイタリアがそれぞれ5.6%と5%の顕著な伸びを示し、この地域全体の消費量は2022年と比較して約4%増加すると予測されました。

- 欧州のドライミックスモルタル消費は住宅部門が大部分を占めており、特に住宅におけるしっくいとレンダーの用途が多いです。これらの用途は、2022年のドライミックスモルタルの同部門の総消費量の64%を占めています。エネルギー効率の高い改築が重視されるようになり、住宅セクタの消費量は顕著な伸びを見せると考えられます。

- 住宅部門に続いて、この地域では商業部門がドライミックスモルタルの利用で最大のシェアを占めています。特に、レンダー、プラスター、防水スラリーは、このセグメントで最も好まれる用途であり、2022年の総消費量の71%を占めています。

- 商業セクタは、予測期間(2023~2030年)中、欧州市場全体の最終用途セクタの中でドライミックスモルタルの消費量において5.39%の最高のCAGRを示すと予測されています。この急増は、欧州委員会の改修の波に後押しされ、このセグメントで改修率の急増が予想されることに起因しています。アップグレードされた商業ビルは、賃貸料の上昇やテナントへのアクセスの向上といった利点があり、老朽化した商業ビルよりも魅力的です。

急速に拡大するイタリアのドライミックスモルタル市場とドイツ、ロシアの高い需要が市場の成長を後押しする

- 欧州では2022年にドライミックスモルタルの需要が5%急増し、前年の数字を上回りました。特にイタリアとロシアがこの成長を牽引し、2022年の需要はそれぞれ7.7%増となりました。欧州では2023年にドライミックスモルタルの需要が4%増加し、主に住宅と商業部門が牽引しました。

- ドイツは欧州におけるドライミックスモルタルの需要で常にトップを占めており、2022年まで平均15%のシェアを占めています。この優位性は、ドイツが欧州で2番目に人口の多い国であることから、2022年には欧州の総消費量の約12%を占める堅調な住宅部門に起因します。

- ロシアはドライミックスモルタルの欧州第2位の消費国です。住宅部門が消費をリードしている一方で、商業部門が僅差で続いています。2022年、商業部門はロシアの総消費量の12%を占めました。住宅部門の床面積が急速に拡大するにつれて、ドライミックスモルタルの消費量は増加し、2023~2030年のCAGRは約6%になると予測されています。

- イタリアは、予測期間中のCAGRが5.28%と予測され、欧州全体でドライミックスモルタルの需要が最も急速に成長することが予想されます。イタリアはグリーン住宅を推進しており、2033年に1日当たり約7,400戸の住宅を改築してエネルギークラスDの基準を満たすことを目指しているため、さらなる推進力となっています。タイル用接着剤とグラウトの需要は成長が見込まれ、2023~2030年のCAGRはそれぞれ6.56%と6.41%です。

欧州のドライミックスモルタル市場動向

スペインやイタリアなどの国々のオフィスビル拡大プロジェクトが欧州の商業建築市場を押し上げる

- 欧州では、2030年の二酸化炭素排出量目標に沿ったエネルギー効率の高いオフィスビル建設への注目が高まっており、2022年の商業施設の新設床面積が12.70%急増しました。従業員がオフィススペースに戻るにつれて、欧州企業も今度は賃貸の意思決定を活発化させ、その結果、2022年には570万平方フィートの新規オフィススペースが追加されました。この成長は2023年も続くと予想され、2022年比2.68%の成長率が予測されました。

- COVID-19のパンデミックは、大幅な労働力不足と資材不足を引き起こし、いくつかの業務用建設プロジェクトの中止や延期につながりました。しかし、閉鎖が緩和され建設活動が再開されると、欧州では2021年の商業施設の新設床面積が16.60%の堅調な伸びを示し、スペインが105.05%の伸び率で首位に立りました。

- 欧州の商業建築セクタは大幅な成長を遂げる態勢にあり、予測期間中の新設床面積のCAGRは3.88%を記録すると予想されます。イタリアのミラノ米国総領事館複合施設(6,500万米ドル、2025年完成予定)や、スペインのArteixoオフィスビル拡大工事(2億6,000万米ドル、180万平方フィート、2024年稼動予定)などの注目すべきプロジェクトが、同地域の商業建設状況を強化すると予想されます。消費者の嗜好がオンライン小売から対面小売へとシフトする中、欧州の小売ショッピングモールの新規床面積は、2022年と比較して2030年までに4億2,830万平方フィート増加すると予想されます。

英国と欧州における手ごろな価格の住宅計画、住宅プロジェクトの完成件数の増加により、住宅建設の新規床面積が増加すると予想されます。

- 欧州の住宅建設部門では、2022年の新設床面積が前年比2.71%増となりました。この背景には、都市化率の上昇があり、都市人口が2020年の73.5%から2022年には75%を占めるようになります。この動向は2023年も続くと予想され、2022年比で3.21%の成長が予測されました。EURO CONSTRUCTネットワークによると、欧州では2023年の住宅プロジェクト完成件数が2.7%増加し、ハンガリー、アイルランド、ノルウェー、ポーランドで顕著な増加が見られました。

- COVID-19の流行は景気後退につながり、その結果、多くの住宅建設プロジェクトが中止または延期されました。その結果、2020年の欧州の住宅新築床面積は前年比9.40%減となりました。しかし、施錠規制が緩和され建設活動が再開されると、このセクタは力強く回復し、2021年の新設床面積は2020年比で18.28%急増しました。スペインが40.23%増と顕著な伸びを示し、イタリアが25.07%増で続きました。

- 欧州の住宅新設床面積は、予測期間中にCAGR 3.89%を記録すると予測されます。この成長をリードするのは英国で、CAGRは5.94%を記録します。この成長の背景には、特に人口増加と住宅供給の限界に悩む都市部で、手頃な価格の住宅に対する需要が高まっていることなどがあります。英国政府のアフォーダブル・ホームズプログラムは、80億米ドルの投資を背景に、2026年までに13万戸の住宅を供給し、国内の住宅建設床面積を拡大することを目指しています。

欧州のドライミックスモルタル産業概要

欧州のドライミックスモルタル市場は細分化されており、上位5社で16.74%を占めています。この市場の主要企業は、Holcim、MAPEI S.p.A.、MBCC Group、Saint-Gobain、Sika AGなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 最終用途セグメントの動向

- 商業

- 産業・施設

- インフラ

- 住宅用

- 主要インフラプロジェクト(現在と発表済み)

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 最終用途セグメント

- 商業

- 産業・施設

- インフラ

- 住宅用

- 用途

- コンクリートの保護と改修

- グラウト

- 断熱と仕上げシステム

- プラスター

- レンダー

- タイル接着剤

- 防水スラリー

- その他

- 国名

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ardex Group

- Baumit Group

- Grupo Puma

- Henkel AG & Co. KGaA

- Holcim

- Knauf Digital GmbH

- MAPEI S.p.A.

- MBCC Group

- Saint-Gobain

- Sika AG

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 93234

The Europe Dry Mix Mortar Market size is estimated at 88.88 million Tons in 2024, and is expected to reach 116.23 million Tons by 2030, growing at a CAGR of 4.57% during the forecast period (2024-2030).

The rising renovation wave in Europe to boost the dry mix mortar market's growth

- In 2022, Europe witnessed a 5% uptick in its consumption of dry mix mortar across end-use sectors, surpassing the previous year. Notably, the commercial sector saw the most significant surge in consumption. Driven by notable increases of 5.6% and 5% from Russia and Italy, respectively, in 2023, the region's overall consumption was projected to rise by around 4% compared to 2022.

- The residential sector dominates Europe's dry mix mortar consumption, particularly for plaster and render applications in residential buildings. These applications accounted for 64% of the sector's total consumption of dry mix mortar in 2022. With a growing emphasis on energy-efficient renovations, the residential sector's consumption is set to witness a notable upswing.

- Following the residential sector, the commercial sector commands the largest share of dry-mix mortar utilization in the region. Notably, render, plaster, and waterproofing slurries are the most preferred applications in this sector, collectively accounting for a 71% share of its total consumption in 2022.

- The commercial sector is projected to witness the highest CAGR of 5.39% in dry mix mortar consumption among end-use sectors across the European market during the forecast period (2023-2030). This surge is attributed to the sector's anticipated surge in renovation rates, driven by the European Commission's renovation wave. Upgraded commercial buildings offer advantages such as higher rental charges and enhanced tenant accessibility, making them more appealing than their outdated counterparts.

The rapidly expanding dry mix mortar market in Italy, coupled with high demand from Germany and Russia, will aid market growth

- Europe witnessed a 5% surge in its dry mix mortar demand in 2022, surpassing the figures from the previous year. Notably, Italy and Russia led this growth, with demand surges of 7.7% each in 2022. Europe witnessed a 4% uptick in dry mix mortar demand in 2023, driven primarily by the residential and commercial sectors.

- Germany has consistently topped the charts for dry mix mortar demand in Europe, commanding an average share of 15% until 2022. This dominance is attributed to its robust residential sector, which accounted for nearly 12% of Europe's total consumption in 2022, as Germany is the second most populous country in Europe.

- Russia stands as Europe's second-largest consumer of dry mix mortar. While the residential sector leads in consumption, the commercial sector follows closely. In 2022, the commercial sector accounted for a 12% share of Russia's total consumption. With the residential sector's floor area set for rapid expansion, its dry mix mortar consumption is projected to grow, registering a CAGR of approximately 6% from 2023 to 2030.

- Italy is poised to witness the swiftest growth in dry mix mortar demand across Europe, with a projected CAGR of 5.28% during the forecast period. Italy's push for green homes adds further impetus, as it aims to renovate around 7,400 homes per day by 2033 to meet energy class D standards. The demand for tile adhesives and grouts is expected to grow, with CAGRs of 6.56% and 6.41%, respectively, from 2023 to 2030.

Europe Dry Mix Mortar Market Trends

Office building expansion projects in countries such as Spain and Italy are boosting the commercial construction market in Europe

- Europe witnessed a 12.70% surge in the new floor area for commercial construction in 2022, driven by an increased focus on constructing energy-efficient office buildings, which aligns with the region's 2030 carbon emission targets. As employees returned to office spaces, European companies, in turn, ramped up their leasing decisions, resulting in the addition of 5.7 million square feet of new office space in 2022. This growth was expected to persist in 2023, with a projected growth rate of 2.68% over 2022.

- The COVID-19 pandemic caused a significant labor and material shortage, leading to the cancellation or postponement of several commercial construction projects. However, as lockdowns eased and construction activities resumed, Europe witnessed a robust 16.60% growth in new floor area for commercial construction in 2021, with Spain being the leader with a 105.05% growth rate.

- The commercial construction sector in Europe is poised for substantial growth, with the new floor area anticipated to register a CAGR of 3.88% during the forecast period. Noteworthy projects, such as the USD 65 million Milan US Consulate General Complex in Italy, slated for completion by 2025, and the USD 260 million Arteixo Office Building Expansion in Spain, spanning 1.8 million square feet and set to be operational in 2024, are expected to bolster the region's commercial construction landscape. As consumer preferences shift from online to in-person retail experiences, the new floor area is expected to increase by 428.3 million square feet for retail shopping malls in Europe by 2030 compared to 2022.

Affordable housing schemes in the UK and Europe and growth in housing project completions are expected to increase the new floor area for residential construction

- Europe's residential construction sector witnessed a 2.71% growth in new floor area in 2022 compared to the previous year. This can be attributed to the escalating urbanization rate, with the urban population accounting for 75% of the total in 2022, up from 73.5% in 2020. This trend was expected to persist in 2023, with a projected growth rate of 3.21% over 2022. According to the EURO CONSTRUCT network, Europe witnessed a 2.7% rise in housing project completions in 2023, with notable increases in Hungary, Ireland, Norway, and Poland.

- The COVID-19 pandemic led to an economic downturn, resulting in the cancellation or postponement of numerous residential construction projects. Consequently, the new floor area for residential construction in Europe plummeted by 9.40% in 2020 compared to the preceding year. However, as lockdown restrictions eased and construction activities resumed, the sector rebounded strongly, with an 18.28% surge in new floor area in 2021 compared to 2020. Spain led the growth with a remarkable 40.23% increase, followed by Italy at 25.07%.

- The new floor area for residential construction in Europe is projected to witness a CAGR of 3.89% during the forecast period. The United Kingdom is poised to lead this growth, recording a CAGR of 5.94%. This growth can be attributed to factors such as a mounting demand for affordable housing, particularly in urban centers grappling with population growth and limited housing supply. The UK government's Affordable Homes Programme, backed by an investment of USD 8 billion, aims to deliver 130,000 housing units by 2026, bolstering the nation's residential construction floor area.

Europe Dry Mix Mortar Industry Overview

The Europe Dry Mix Mortar Market is fragmented, with the top five companies occupying 16.74%. The major players in this market are Holcim, MAPEI S.p.A., MBCC Group, Saint-Gobain and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Application

- 5.2.1 Concrete Protection and Renovation

- 5.2.2 Grouts

- 5.2.3 Insulation and Finishing Systems

- 5.2.4 Plaster

- 5.2.5 Render

- 5.2.6 Tile Adhesive

- 5.2.7 Water Proofing Slurries

- 5.2.8 Other Applications

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ardex Group

- 6.4.2 Baumit Group

- 6.4.3 Grupo Puma

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Holcim

- 6.4.6 Knauf Digital GmbH

- 6.4.7 MAPEI S.p.A.

- 6.4.8 MBCC Group

- 6.4.9 Saint-Gobain

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms