商用車- 市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 409 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693647

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

商用車市場規模は2025年に9,100億米ドルと推定・予測され、2029年には1兆2,200億米ドルに達し、予測期間中(2025~2029年)のCAGRは7.61%で成長すると予測されます。

- 新興経済圏における産業部門の成長と商業ロジスティクス活動の活発化が、商用車需要の主要促進要因となっています。この需要急増の主要因は、建設産業とeコマース産業の拡大であり、効率的な資材輸送の必要性が高まっています。商用車の生産台数は、2020年に300万台減少した後、回復し、2021年には約2,320万台に達し、着実な回復を示します。

- COVID-19の流行によりほとんどの国際国境が閉鎖されたため、商用車製造産業は2021年にサプライチェーンの長期的な混乱に直面し、市場成長の妨げとなりました。パンデミックの輸送部門への影響は甚大で、貨物の円滑な移動を確保する上で、貨物産業と製造産業の双方に大きな障害をもたらしました。

- 商用車に対する需要の増加により、トラックメーカーは需要の高まりと排ガス規制に対応するため、先進的な新型トラックを導入しています。商用車リースとレンタル産業も、業務効率化の要求の高まりと、多業種にわたる企業によるスケールメリットの実現により成長しています。eコマースは近年、世界の小売の枠組みにおいて不可欠な要素となっています。2020年には20億人以上がオンラインで商品やサービスを購入し、同年、世界のeコマース売上高は4兆2,000億米ドルを突破しました。商用車市場全体は、今後大幅な成長が見込まれます。

輸送部門からの二酸化炭素排出に対する懸念の高まりは、今後数年間、電気商用車の普及を促進すると予想されます。

- 2021年、世界の商用車生産台数は回復し、2020年の300万台の減少に続いて約2,320万台に達しました。小型商用車は、一般的に重量3.5トン以下に分類されます。広義には、商用車とは、物資や人の輸送用に設計された自動車を指します。生産台数では北米がリードし、2021年には1,090万台の商用車が生産されます。アジアとオセアニアは大型トラックのトップ生産国に浮上し、2021年の推定生産台数は約330万台です。このセグメントの特筆すべき成長要因は、自動車産業におけるクリーンエネルギー需要の増加です。

- 2019~2020年にかけて13%落ち込んだ世界の商用車生産台数は、2021年には回復しました。世界の商用車市場は、パンデミック時に大きな混乱に直面し、2020年まで続いた国の封鎖により製造施設が停止しました。2021年には需要も生産台数も回復したが、世界のチップ不足により市場は後退に直面し、生産削減につながりました。

- 運輸部門からの二酸化炭素排出に対する懸念が高まるなか、商用車産業は代替燃料源を優先しています。世界各国の政府は、電気自動車の普及を促進するための規制を率先して実施しています。中国、インド、フランス、英国は、2040年までにガソリン車とディーゼル車の生産を停止する計画を発表しています。このシフトにより、今後数年間は電気商用車の普及が促進されると予想されます。

世界の商用車市場動向

世界の需要の高まりと政府の支援が電気自動車市場の成長を後押し

- 電気自動車(EV)は、エネルギー効率を高め、温室効果ガスや公害の排出を削減する可能性に後押しされ、自動車産業において不可欠なものとなっています。この急成長の主要因は、環境に対する関心の高まりと政府の支援策にあります。特に、EVの世界販売台数は、2021年と比較して2022年には10.82%増と堅調な伸びを示しました。予測によると、電気乗用車の年間販売台数は2025年末までに500万台を突破し、自動車販売台数全体の約15%を占めるようになります。

- ロンドン警視庁消防局のような大手メーカーや組織は、電動モビリティ戦略を積極的に推進しています。例えば、2025年までに車両をゼロエミッション化し、2030年までにバンの40%を電動化、2040年までに完全電動化を達成するという目標を掲げています。世界的にも同様の動向が予想され、2024~2030年にかけて電気自動車の需要と販売が急増します。

- アジア太平洋と欧州は、バッテリー技術と車両電化の進歩に牽引され、電気自動車生産を支配する態勢を整えています。2020年5月、起亜自動車欧州は「プランS」を発表し、電動化への戦略的シフトを表明しました。この決定は、起亜のEVが欧州で記録的な販売台数を達成したことを受けてのものです。起亜は2025年までに、乗用車、SUV、MPVなどさまざまなセグメントにまたがる11のEVモデルを世界に投入するという野心的な計画を掲げています。同社は、2026年までにEVの世界年間販売台数50万台の達成を目指しています。

商用車産業概要

商用車市場は細分化されており、上位5社で30%を占めています。この市場の主要企業は、BAIC Motor Corporation Ltd.、Daimler AG(Mercedes-Benz AG)、Ford Motor Company、Toyota Motor Corporation、Volkswagen AGなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- アフリカ

- アジア太平洋

- 欧州

- 中東

- 北米

- 南米

- 一人当たりGDP

- アフリカ

- アジア太平洋

- 欧州

- 中東

- 北米

- 南米

- 自動車購入のための消費支出(cvp)

- アフリカ

- アジア太平洋

- 欧州

- 中東

- 北米

- 南米

- インフレ率

- アフリカ

- アジア太平洋

- 欧州

- 中東

- 北米

- 南米

- 自動車ローンの金利

- 電化の影響

- EV充電ステーション

- バッテリーパック価格

- アフリカ

- アジア太平洋

- 欧州

- 中東

- 北米

- 南米

- Xev新モデル発表

- ロジスティクスパフォーマンスインデックス

- アフリカ

- アジア太平洋

- 欧州

- 中東

- 北米

- 南米

- 燃料価格

- メーカー別生産統計

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車種

- 商用車

- 大型商用トラック

- 小型商用ピックアップトラック

- 小型商用バン

- 中型商用トラック

- 商用車

- 推進タイプ

- ハイブリッドと電気自動車

- 燃料カテゴリー別

- BEV

- FCEV

- HEV

- PHEV

- 内燃機関

- 燃料カテゴリー別

- 天然ガス

- ディーゼル

- ガソリン

- LPG

- ハイブリッドと電気自動車

- 地域別

- アフリカ

- アジア太平洋

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- 韓国

- タイ

- その他のアジア太平洋

- 欧州

- チェコ共和国

- 中東

- 北米

- カナダ

- 南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BAIC Motor Corporation Ltd.

- BYD Auto Co. Ltd.

- Daimler AG(Mercedes-Benz AG)

- Dongfeng Motor Corporation

- Ford Motor Company

- General Motors Company

- Groupe Renault

- Mahindra & Mahindra Limited

- Nissan Motor Co. Ltd.

- Rivian Automotive Inc.

- Saic General Motors Corporation Limited

- Scania AB

- Tata Motors Limited

- Toyota Motor Corporation

- Volkswagen AG

- Volvo Group

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 93035

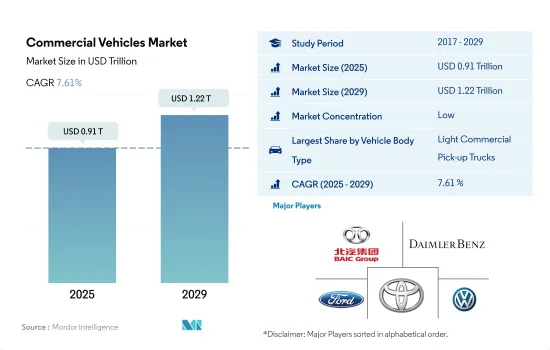

The Commercial Vehicles Market size is estimated at 0.91 trillion USD in 2025, and is expected to reach 1.22 trillion USD by 2029, growing at a CAGR of 7.61% during the forecast period (2025-2029).

- The industrial sector's growth in emerging economies and the rise in commercial logistics activities are key drivers of the demand for commercial vehicles. This demand surge is primarily fueled by the expanding construction and e-commerce industries, which are driving the need for efficient material transportation. Following a dip of three million units in 2020, the production of commercial vehicles rebounded, reaching approximately 23.2 million units in 2021, marking a steady recovery.

- With most international borders closed due to the COVID-19 pandemic, the commercial vehicle manufacturing industry faced prolonged disruptions in its supply chain in 2021, hampering market growth. The pandemic's impact on the transportation sector was profound, presenting significant hurdles for both the freight and manufacturing industries in ensuring smooth movement of goods.

- Due to increased demand for commercial vehicles, truck manufacturers have been introducing new advanced trucks to meet the rising demand and emission standards. Commercial vehicle leasing and the rental industry are also growing due to the increasing demand for operational efficiencies and the realization of economies of scale by businesses across multiple industries. E-commerce has become an essential component of the global retail framework in recent years. Over 2 billion people purchased goods or services online in 2020, and global e-commerce sales surpassed USD 4.2 trillion in the same year. The overall commercial vehicle market is expected to grow significantly in the future.

The rising concerns over carbon emissions from the transportation sector are expected to drive the penetration of electric commercial vehicles in the coming years

- In 2021, global commercial vehicle manufacturing rebounded, reaching approximately 23.2 million units, following a decline of 3 million units in 2020. Light commercial vehicles, typically weighing under 3.5 tons, are classified as such. Broadly, commercial vehicles refer to motor vehicles designed for transporting goods and people. North America took the lead in production, manufacturing 10.9 million commercial vehicles in 2021. Asia and Oceania emerged as the top producers of heavy trucks, with an estimated output of nearly 3.3 million units in 2021. A notable growth driver for this sector is the increasing demand for clean energy in the automotive industry.

- After a 13% dip from 2019 to 2020, global commercial vehicle output rebounded in 2021. The global commercial vehicles market faced significant disruptions during the pandemic, with manufacturing facilities shutting down due to national lockdowns that extended into 2020. Although the demand and output recovered in 2021, the market faced a setback due to a global chip shortage, leading to production cutbacks.

- Amid the rising concerns over carbon emissions from the transportation sector, the commercial fleet industry is prioritizing alternative fuel sources. Governments worldwide are taking the lead in implementing regulations to promote electric vehicle adoption. China, India, France, and the United Kingdom have announced plans to halt gasoline and diesel vehicle production by 2040. This shift is expected to drive the penetration of electric commercial vehicles in the coming years.

Global Commercial Vehicles Market Trends

The rising global demand and government support propel electric vehicle market growth

- Electric vehicles (EVs) have become indispensable in the automotive industry, driven by their potential to enhance energy efficiency and reduce greenhouse gas and pollution emissions. This surge is primarily attributed to growing environmental concerns and supportive government initiatives. Notably, global EV sales witnessed a robust 10.82% growth in 2022 compared to 2021. Projections indicate that annual sales of electric passenger cars will surpass 5 million by the end of 2025, accounting for approximately 15% of total vehicle sales.

- Leading manufacturers and organizations, like the London Metropolitan Police & Fire Service, have been actively pursuing their electric mobility strategies. For instance, they have set a target of a zero-emission fleet by 2025, with a goal of electrifying 40% of their vans by 2030 and achieving full electrification by 2040. Similar trends are expected globally, with the period from 2024 to 2030 witnessing a surge in demand and sales of electric vehicles.

- Asia-Pacific and Europe are poised to dominate electric vehicle production, driven by their advancements in battery technology and vehicle electrification. In May 2020, Kia Motors Europe unveiled its "Plan S," signaling a strategic shift toward electrification. This decision came on the heels of record-breaking sales of Kia's EVs in Europe. Kia has ambitious plans to introduce 11 EV models globally by 2025, spanning various segments like passenger vehicles, SUVs, and MPVs. The company aims to achieve annual global EV sales of 500,000 by 2026.

Commercial Vehicles Industry Overview

The Commercial Vehicles Market is fragmented, with the top five companies occupying 30%. The major players in this market are BAIC Motor Corporation Ltd., Daimler AG (Mercedes-Benz AG), Ford Motor Company, Toyota Motor Corporation and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.1.1 Africa

- 4.1.2 Asia-Pacific

- 4.1.3 Europe

- 4.1.4 Middle East

- 4.1.5 North America

- 4.1.6 South America

- 4.2 GDP Per Capita

- 4.2.1 Africa

- 4.2.2 Asia-Pacific

- 4.2.3 Europe

- 4.2.4 Middle East

- 4.2.5 North America

- 4.2.6 South America

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.3.1 Africa

- 4.3.2 Asia-Pacific

- 4.3.3 Europe

- 4.3.4 Middle East

- 4.3.5 North America

- 4.3.6 South America

- 4.4 Inflation

- 4.4.1 Africa

- 4.4.2 Asia-Pacific

- 4.4.3 Europe

- 4.4.4 Middle East

- 4.4.5 North America

- 4.4.6 South America

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.8.1 Africa

- 4.8.2 Asia-Pacific

- 4.8.3 Europe

- 4.8.4 Middle East

- 4.8.5 North America

- 4.8.6 South America

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.10.1 Africa

- 4.10.2 Asia-Pacific

- 4.10.3 Europe

- 4.10.4 Middle East

- 4.10.5 North America

- 4.10.6 South America

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Heavy-duty Commercial Trucks

- 5.1.1.2 Light Commercial Pick-up Trucks

- 5.1.1.3 Light Commercial Vans

- 5.1.1.4 Medium-duty Commercial Trucks

- 5.1.1 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 CNG

- 5.2.2.1.2 Diesel

- 5.2.2.1.3 Gasoline

- 5.2.2.1.4 LPG

- 5.2.1 Hybrid and Electric Vehicles

- 5.3 Region

- 5.3.1 Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 Australia

- 5.3.2.2 China

- 5.3.2.3 India

- 5.3.2.4 Indonesia

- 5.3.2.5 Japan

- 5.3.2.6 Malaysia

- 5.3.2.7 South Korea

- 5.3.2.8 Thailand

- 5.3.2.9 Rest-of-APAC

- 5.3.3 Europe

- 5.3.3.1 Czech Republic

- 5.3.4 Middle East

- 5.3.5 North America

- 5.3.5.1 Canada

- 5.3.6 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BAIC Motor Corporation Ltd.

- 6.4.2 BYD Auto Co. Ltd.

- 6.4.3 Daimler AG (Mercedes-Benz AG)

- 6.4.4 Dongfeng Motor Corporation

- 6.4.5 Ford Motor Company

- 6.4.6 General Motors Company

- 6.4.7 Groupe Renault

- 6.4.8 Mahindra & Mahindra Limited

- 6.4.9 Nissan Motor Co. Ltd.

- 6.4.10 Rivian Automotive Inc.

- 6.4.11 Saic General Motors Corporation Limited

- 6.4.12 Scania AB

- 6.4.13 Tata Motors Limited

- 6.4.14 Toyota Motor Corporation

- 6.4.15 Volkswagen AG

- 6.4.16 Volvo Group

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

商用車- 市場シェア分析、産業動向・統計、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 409 Pages

- 納期

- 2~3営業日