|

市場調査レポート

商品コード

1693617

米国の商用車:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)United States Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の商用車:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 245 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

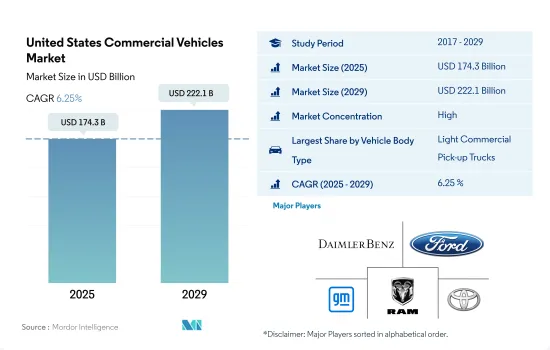

米国の商用車市場規模は2025年に1,743億米ドルと推定され、2029年には2,221億米ドルに達すると予測され、予測期間中(2025-2029年)のCAGRは6.25%で成長すると予測されます。

米国の商用車の多様性は堅調な経済に牽引され、都市部の配達用バンから長距離トラックまで幅広い需要があります。

- 商用車市場は、貨物輸送量の増加、地域バリューチェーンの世界化、駆動技術の進歩、安全性への関心の高まりなどの要因により、絶え間ない進化を遂げています。2005年以降、燃料価格は着実に上昇しており、ディーゼル・トラックの成長に影響を与えています。さらに、米国の燃料メーカーはほぼ最大限の生産能力で操業しており、生産拡大の余地はほとんどないです。

- パンデミックの発生は、商用車業界のサプライチェーンに前例のない混乱をもたらしました。世界的に施されたロックダウンやその他の制限により、前例のない規模の移動・移動制限が発生しました。インフラや物流など、輸送に大きく依存する産業は行き詰まり、製造業や貨物部門に新たな障害をもたらしました。

- 電気自動車やハイブリッド車の需要が急増するなか、いくつかの国は電気自動車充電インフラの整備を優先してきました。その結果、インフラの成長を促進するために数多くの政策やインセンティブが導入されました。米国政府は、2040年までにガソリン車とディーゼル車の生産を段階的に廃止し、大半の車両をバッテリーで走行させることを目標に、電気自動車の普及を促進するための法律を率先して制定しました。政府や自治体も、持続可能なモビリティへの移行を促進するためのインセンティブや規制を導入しています。米国政府は2030年までに、あらゆる車種と技術に対応する50万基の公共充電器を設置する計画です。

米国の商用車市場動向

米国における政府の取り組みと需要増加が牽引する電気自動車販売の急成長

- 米国では近年、電気自動車(EV)の導入が急増しています。この上昇の背景には、EVに対する意識の高まり、環境問題への関心の高まり、政府規制の実施があります。特に2016年、カリフォルニア州は二酸化炭素排出量の抑制と大気環境の改善を目的としたゼロエミッションビークル(ZEV)プログラムを導入しました。この取り組みは、カリフォルニア州内での電気自動車の普及に拍車をかけただけでなく、他の州にも同様のZEV規制を導入するよう影響を与えました。その結果、2017年から2022年にかけて、バッテリー式電気自動車(BEV)の需要が634%急増しました。

- 米国の電気商用車の需要も増加傾向にあります。eコマース産業の活況、物流活動の増加、よりクリーンな輸送を求める政府の取り組みといった要因が、この成長を後押ししています。重要な動きとして、ニューヨーク州知事は2021年9月に先進クリーントラック(ACT)規則に署名しました。この規則では、2035年までにすべての新型小型車をゼロ・エミッション化し、2045年までに中型車と大型車もゼロ・エミッション化するという目標が設定されています。その結果、米国では2022年に電気商用車の需要が前年比で21%急増しました。

- リベート、補助金、戦略的計画などの政府の取り組みが、全国的な自動車の電動化をさらに後押ししています。2022年5月、バイデン大統領は、ガス自動車から電気自動車への移行を目指し、国内でのバッテリー製造を促進する30億米ドルの計画を発表しました。この推進により、特に2024年から2030年にかけて、国内での電動モビリティが大幅に促進され、それによってバッテリーパックの需要が増大すると予想されます。

米国の商用車産業の概要

米国の商用車市場はかなり統合されており、上位5社で80.10%を占めています。この市場の主要企業は以下の通り。 Daimler AG(Mercedes-Benz AG), Ford Motor Company, General Motors Company, Ram Trucking, Inc. and Toyota Motor Corporation(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- 一人当たりGDP

- 自動車購入のための消費者支出(cvp)

- インフレ率

- 自動車ローン金利

- 電化の影響

- EV充電ステーション

- バッテリーパック価格

- Xev新モデル発表

- 物流性能指数

- 燃料価格

- OEM生産統計

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車両タイプ

- 商用車

- バス

- 大型商用トラック

- 小型商用ピックアップトラック

- 小型商用バン

- 中型商用トラック

- 商用車

- 推進タイプ

- ハイブリッドおよび電気自動車

- 燃料カテゴリー別

- BEV

- FCEV

- HEV

- PHEV

- ICE

- 燃料カテゴリー別

- 天然ガス

- ディーゼル

- ガソリン

- LPG

- ハイブリッドおよび電気自動車

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Daimler AG(Mercedes-Benz AG)

- Daimler Truck Holding AG

- Ford Motor Company

- General Motors Company

- Hino Motors Ltd.

- Isuzu Motors Limited

- PACCAR Inc.

- Ram Trucking, Inc.

- Toyota Motor Corporation

- Volvo Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The United States Commercial Vehicles Market size is estimated at 174.3 billion USD in 2025, and is expected to reach 222.1 billion USD by 2029, growing at a CAGR of 6.25% during the forecast period (2025-2029).

The diversity of commercial vehicles in the United States is driven by a robust economy, with demands ranging from urban delivery vans to long-haul trucks

- The commercial vehicle market is undergoing constant evolution due to factors like increased traffic in goods, globalization of regional value chains, advancements in drive technology, and a heightened focus on safety. Since 2005, fuel prices have been on a steady rise, impacting the growth of diesel trucks. Additionally, fuel producers in the United States are operating at near-maximum capacity, leaving little room for production expansion.

- The onset of the pandemic led to unprecedented disruptions in the commercial vehicle industry's supply chains. Lockdowns and other restrictions imposed globally resulted in mobility and travel limitations of an unprecedented scale. Industries heavily reliant on transportation, such as infrastructure and logistics, came to a standstill, presenting new hurdles for the manufacturing and freight sectors.

- With the surging demand for electric and hybrid vehicles, several countries have prioritized upgrading their electric vehicle charging infrastructure. Consequently, numerous policies and incentives have been introduced to foster infrastructure growth. The US government has taken the lead in enacting legislation to promote electric vehicle adoption, aiming to phase out gasoline and diesel vehicle production by 2040, with a majority of vehicles running on batteries. Governments and municipalities have also implemented incentives and regulations to expedite the shift toward sustainable mobility. By 2030, the US government plans to establish 500,000 public chargers, catering to all vehicle types and technologies.

United States Commercial Vehicles Market Trends

Rapid growth in electric vehicle sales driven by government initiatives and increasing demand in the US

- The United States has witnessed a significant surge in the adoption of electric vehicles (EVs) in recent years. This uptick can be attributed to a heightened awareness of EVs, growing environmental concerns, and the implementation of government regulations. Notably, in 2016, California introduced the Zero-Emission Vehicle (ZEV) program aimed at curbing carbon emissions and improving air quality. This initiative has not only spurred the growth of electric cars within California but has also influenced other states to adopt similar ZEV regulations. Consequently, the nation saw a remarkable 634% surge in demand for battery electric vehicles (BEVs) from 2017 to 2022.

- The demand for electric commercial vehicles in the United States is also on the rise. Factors such as the booming e-commerce industry, increased logistics activities, and governmental initiatives for cleaner transportation have fueled this growth. In a significant move, the governor of New York signed the Advanced Clean Truck (ACT) Rule in September 2021. This rule sets a target for all new light-duty vehicles to be zero-emission by 2035 and the same for medium- and heavy-duty vehicles by 2045. As a result, the United States witnessed a 21% surge in demand for electric commercial vehicles in 2022 compared to the previous year.

- Governmental efforts, including rebates, subsidies, and strategic plans, are further bolstering the electrification of vehicles nationwide. In May 2022, President Biden unveiled a USD 3 billion plan to expedite domestic battery manufacturing, with the aim of transitioning gas-powered vehicles to electric ones. This push is expected to significantly boost electric mobility in the country, particularly during 2024-2030, thereby amplifying the demand for battery packs.

United States Commercial Vehicles Industry Overview

The United States Commercial Vehicles Market is fairly consolidated, with the top five companies occupying 80.10%. The major players in this market are Daimler AG (Mercedes-Benz AG), Ford Motor Company, General Motors Company, Ram Trucking, Inc. and Toyota Motor Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Buses

- 5.1.1.2 Heavy-duty Commercial Trucks

- 5.1.1.3 Light Commercial Pick-up Trucks

- 5.1.1.4 Light Commercial Vans

- 5.1.1.5 Medium-duty Commercial Trucks

- 5.1.1 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 CNG

- 5.2.2.1.2 Diesel

- 5.2.2.1.3 Gasoline

- 5.2.2.1.4 LPG

- 5.2.1 Hybrid and Electric Vehicles

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Daimler AG (Mercedes-Benz AG)

- 6.4.2 Daimler Truck Holding AG

- 6.4.3 Ford Motor Company

- 6.4.4 General Motors Company

- 6.4.5 Hino Motors Ltd.

- 6.4.6 Isuzu Motors Limited

- 6.4.7 PACCAR Inc.

- 6.4.8 Ram Trucking, Inc.

- 6.4.9 Toyota Motor Corporation

- 6.4.10 Volvo Group

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms