|

市場調査レポート

商品コード

1693632

欧州の中型・大型商用車:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Medium and Heavy-duty Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の中型・大型商用車:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 228 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

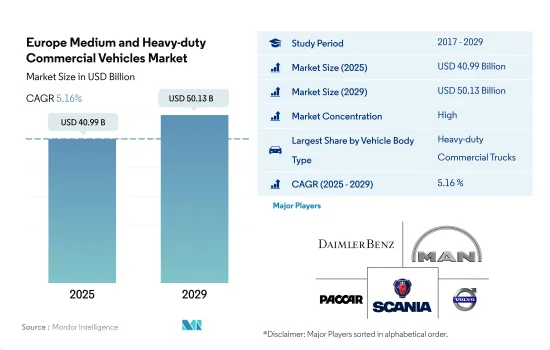

欧州の中型・大型商用車市場規模は2025年に409億9,000万米ドルと推計され、2029年には501億3,000万米ドルに達すると予測され、予測期間(2025-2029年)のCAGRは5.16%で成長すると予測されます。

欧州の商業輸送における中型・大型商用車の戦略的重要性から、企業は効率性と規制状況の遵守に注力しています。

- 輸送は欧州経済の強化、成長促進、競争力強化において極めて重要な役割を果たしています。商用車部門は、パリ協定に概説された気候変動目標に積極的に歩調を合わせています。代替燃料やパワートレインの採用が進む一方で、商用車用の充電・給油インフラの利用可能性は依然として限られています。EUの道路を走る630万台以上の車両は、陸上貨物全体の76.7%という驚異的な割合を占め、年間150億トンという途方もない量の貨物を輸送しています。

- 欧州はCOVID-19の影響の矢面に立たされ、3月と4月に約5万台の生産台数の減少を目の当たりにしました。これは主に、厳しい工場閉鎖、職場規制、サプライチェーンの混乱、自宅待機の注文によるものです。2020年末までに、欧州の商用車生産台数は前年比で20%近く減少しました。特筆すべきは、中欧のポーランドや西欧のイタリアのような、欧州大陸のトラック産業にとって極めて重要な拠点である国々が、最も急激な需要減少を目の当たりにすると予測されていることです。

- ロジスティクスと建設活動の成長は、資材輸送の需要に拍車をかけ、欧州全域での商用車販売の急増につながっています。この動向は、近い将来、商用車市場をさらに活性化させると予想されます。同市場は、建設やeコマース事業の活発化によって成長する態勢を整えています。さらに、電気自動車へのシフトは、今後数年間の市場拡大の有望な展望を秘めています。

欧州の中型・大型商用車市場の動向

環境問題、政府の支援、脱炭素化目標が欧州の電気自動車需要と販売に拍車

- 欧州諸国における電気自動車の需要と販売は、ここ数年で大きく伸びています。ドイツは2022年に電気自動車の販売台数が2021年比で22%増加し、次いで英国が2022年に2021年比で18.40%増加しました。環境問題への関心の高まり、政府の厳しい規範、燃費の良さ、サービスコストの低さ、二酸化炭素排出量の少なさといった電気自動車の利点、政府による補助金などが、欧州諸国における電気自動車の成長に寄与している要因のひとつです。

- 電気商用車、特に小型トラックの需要は、欧州諸国で徐々に伸びています。さらに、各国政府も電気自動車の導入を支援しています。2021年11月、英国政府は2040年までにすべての大型商用車をゼロ・エミッションにするという公約を発表しました。このような要因により、英国における2022年の電気商用車販売台数は2021年比で23.17%増加し、各国における同様の慣行が欧州全体の電気商用車需要を高めています。

- 欧州諸国における車両の電動化は、今後数年間で飛躍的に成長すると予測されています。脱炭素化に向けた各国政府の取り組みが、欧州の電気商用車市場を牽引すると予想されます。例えば、2022年1月、ドイツの運輸大臣は、2030年までに1,500万台の電気自動車を走らせるという目標を発表しました。こうした要因により、欧州諸国では2024~2030年の間に電気自動車の販売が増加すると予想されます。

欧州の中型・大型商用車産業の概要

欧州の中型・大型商用車市場はかなり統合されており、上位5社で87%を占めています。この市場の主要企業は以下の通り。 Daimler AG(Mercedes-Benz AG), Man Truck & Bus, PACCAR Inc., Scania AB and Volvo Group(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- 一人当たりGDP

- 自動車購入のための消費者支出(cvp)

- インフレ率

- 自動車ローン金利

- 電化の影響

- EV充電ステーション

- バッテリーパック価格

- Xev新モデル発表

- 物流性能指数

- 燃料価格

- OEM生産統計

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車両タイプ

- 商用車

- 推進タイプ

- ハイブリッド車と電気自動車

- 燃料カテゴリー別

- BEV

- FCEV

- HEV

- PHEV

- ICE

- 燃料カテゴリー別

- 天然ガス

- ディーゼル

- ガソリン

- LPG

- ハイブリッド車と電気自動車

- 国名

- オーストリア

- ベルギー

- チェコ共和国

- デンマーク

- エストニア

- フランス

- ドイツ

- アイルランド

- イタリア

- ノルウェー

- ポーランド

- ロシア

- スペイン

- スウェーデン

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Daimler AG(Mercedes-Benz AG)

- Man Truck & Bus

- PACCAR Inc.

- Scania AB

- Volvo Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Europe Medium and Heavy-duty Commercial Vehicles Market size is estimated at 40.99 billion USD in 2025, and is expected to reach 50.13 billion USD by 2029, growing at a CAGR of 5.16% during the forecast period (2025-2029).

Due to the strategic importance of medium and heavy-duty vehicles in Europe's commercial transport landscape, businesses are focusing on efficiency and regulatory compliance

- Transport plays a pivotal role in bolstering Europe's economy, fostering growth, and enhancing its competitiveness. The commercial vehicle sector is actively aligning with the climate goals outlined in the Paris Agreement. While the adoption of alternative fuels and powertrains is gaining traction, the availability of charging and refueling infrastructure for commercial vehicles remains limited. With over 6.3 million vehicles plying the roads of the EU, they account for a staggering 76.7% of all land-based freight, moving a colossal 15 billion tonnes annually.

- Europe bore the brunt of the COVID-19 impact, witnessing a production loss of approximately 50,000 units in March and April. This was primarily due to stringent factory closures, workplace regulations, supply chain disruptions, and stay-at-home orders. By the close of 2020, commercial vehicle manufacturing in Europe had plummeted by nearly 20% compared to the preceding year. Notably, countries like Poland in Central Europe and Italy in the West, pivotal hubs for the continent's trucking industry, are projected to witness the sharpest demand decline.

- The growth in logistics and construction activities has spurred the demand for material transportation, leading to a surge in commercial vehicle sales across Europe. This trend is expected to further bolster the business vehicle market in the near future. The market is poised for growth, driven by the uptick in construction and e-commerce operations. Additionally, the shift toward electric vehicles holds promising prospects for market expansion in the coming years.

Europe Medium and Heavy-duty Commercial Vehicles Market Trends

Environmental concerns, government support, and decarbonization goals fuel European electric vehicle demand and sales

- The demand and sales of electric vehicles in European countries have grown significantly over the past few years. Germany witnessed a growth in the sales of electric cars by 22% in 2022 over 2021, followed by the United Kingdom with an 18.40% increase in 2022 over 2021. Growing environmental concerns, stringent governmental norms, advantages of electric vehicles such as fuel efficiency, low service cost, no carbon emissions, and subsidies by the government are some of the factors contributing to the growth of electric vehicles in European countries.

- The demand for electric commercial vehicles, especially light trucks, is growing gradually in European countries. Moreover, the governments of various countries are also supporting the adoption of electric vehicles. In November 2021, the government of the United Kingdom announced a pledge that all heavy-duty vehicles would be zero-emission by the year 2040. Such factors have increased the sales of electric commercial vehicles in the United Kingdom by 23.17% in 2022 over 2021, and similar practices in various countries are enhancing the demand for electric commercial vehicles across Europe.

- It is projected that the electrification of vehicles in European countries is expected to grow tremendously in the next few years. The efforts of the governments in the regions for decarbonization are expected to drive the electric commercial vehicle market in Europe. For instance, in January 2022, the transport minister of Germany announced a goal to put 15 million electric vehicles on the road by 2030. Such factors are expected to increase the sales of electric vehicles during the 2024-2030 period in European countries.

Europe Medium and Heavy-duty Commercial Vehicles Industry Overview

The Europe Medium and Heavy-duty Commercial Vehicles Market is fairly consolidated, with the top five companies occupying 87%. The major players in this market are Daimler AG (Mercedes-Benz AG), Man Truck & Bus, PACCAR Inc., Scania AB and Volvo Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 CNG

- 5.2.2.1.2 Diesel

- 5.2.2.1.3 Gasoline

- 5.2.2.1.4 LPG

- 5.2.1 Hybrid and Electric Vehicles

- 5.3 Country

- 5.3.1 Austria

- 5.3.2 Belgium

- 5.3.3 Czech Republic

- 5.3.4 Denmark

- 5.3.5 Estonia

- 5.3.6 France

- 5.3.7 Germany

- 5.3.8 Ireland

- 5.3.9 Italy

- 5.3.10 Norway

- 5.3.11 Poland

- 5.3.12 Russia

- 5.3.13 Spain

- 5.3.14 Sweden

- 5.3.15 UK

- 5.3.16 Rest-of-Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Daimler AG (Mercedes-Benz AG)

- 6.4.2 Man Truck & Bus

- 6.4.3 PACCAR Inc.

- 6.4.4 Scania AB

- 6.4.5 Volvo Group

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms