北米のバン:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

North America Van - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 202 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693615

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

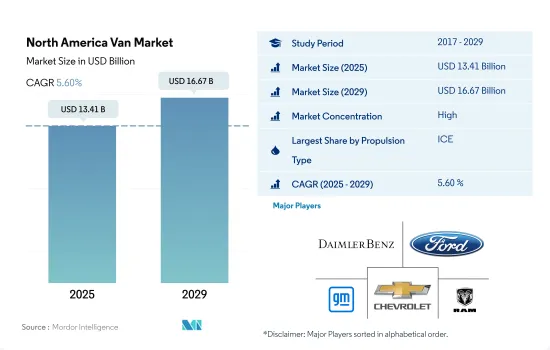

北米のバン市場規模は2025年に134億1,000万米ドルと推定・予測され、2029年には166億7,000万米ドルに達し、予測期間中(2025~2029年)のCAGRは5.60%で成長すると予測されます。

北米のLCV市場は、経済開発、新興国市場の物流ニーズ、持続可能な輸送への注力に後押しされ、着実な成長が見込まれる

- 2023年、北米のLCV市場はすべての推進タイプで微増を示し、販売台数は2022年の4,046,122台から4,055,770台に達します。この成長は緩やかではあるが、経済や環境情勢が変化する中、物流、小売、サービスなど様々なセクターを支える重要な役割を果たし続けている市場の安定化を示しています。2024年の販売台数は405万8,449台に達すると予想され、北米におけるLCVの需要が安定していることを示しています。この安定した市場実績は、この地域の経済の回復力と商業部門の多様なニーズを反映し、商業と貿易を促進する上でLCVが不可欠な役割を担っていることを強調しています。

- 北米のLCV市場の緩やかな成長は、景気回復、eコマースの急増、持続可能性への関心の高まりなど、より広範な動向と一致しています。電気自動車やハイブリッド車にスポットライトが当たることが多いが、LCVの需要は様々な推進タイプにまたがっており、よりクリーンな輸送機関へのバランスの取れたシフトを示しています。

- 2024年から2030年にかけて、北米のLCV市場は徐々に拡大し、2030年末には販売台数が4,473,267台に達する可能性があると予測されています。この成長は、経済拡大、都市化、eコマース需要の急増によって推進され、堅牢な物流が必要となります。さらに、環境への配慮と車両効率の進歩が牽引役となり、電気自動車やハイブリッドLCVの市場は顕著な伸びを見せ、北米の商業輸送の展望をさらに形作ることになります。

北米のバン市場は著しい成長を遂げており、各国の動向は多用途で効率的な輸送ソリューションへの嗜好の高まりを指し示しています。

- 自動車メーカーは、石油供給の減少やガソリン価格の高騰を背景に、自動車の代替燃料源を積極的に模索しています。2022年のロシアとウクライナの紛争は、過去数十年間すでに2倍になっていた石油価格をさらに悪化させ、より経済的な日常の移動手段として電気自動車(EV)への世界の後押しを促しました。税率も世界の燃料費に一役買っており、米国の燃料税は19%と最も低く、インドは69%という高額な税金を課しています。こうした要因が、過去20年間の燃料価格の上昇と相まって、従来の内燃機関(ICE)車に比べて大幅に低い運転コストを誇るEVの魅力を際立たせています。

- 自動車メーカーにとって、車両ポートフォリオの電動化は最重要目標となっています。ボルボは2025年までに世界販売台数の50%をEVにすることを目指しています。スバルは2035年までに全車種にハイブリッド車か電気自動車を導入する計画です。フォードは2025年までにEVに290億米ドルを投資する計画であり、GMは2035年までに小型車の全ラインナップを電動化するというビジョンを掲げ、270億米ドルを投資する予定です。他のメーカーも、時期や目標は異なるもの、同様の野心を掲げているが、いずれも電動化へのコミットメントで一致しています。

- 北米では、2020年から2028年の間に12車種の新型電気バンが発売される予定です。注目すべきは、ELMS UD-1、Rivian R1A、BrightDrop EV600など、大半がまったく新しいモデルになることです。さらに、メルセデス・ベンツeSprinterやフォード・トランジットのような既存のバン・ラインも、将来的に全電気バンを導入する準備を進めています。

北米のバン市場の動向

北米では、政府の支援と環境問題への関心の高まりにより、電気自動車の需要が拡大

- ロシアのCVPは近年大きな変動を経験しています。2017年の2億820万米ドルから着実に上昇し、2019年にピークを迎えました。しかし、2020年には1億9,390万米ドルまで落ち込み、これは主にCOVID-19パンデミックがもたらした経済的課題によるものでした。注目すべきは、2022年に市場が急回復し、2億6,980万米ドルに達したことです。この復活は、ロシアの自動車セクターの回復力と、景気刺激策と消費者需要の高まりの潜在的影響の両方を浮き彫りにしています。

- 政府の優遇措置や補助金は、顧客、特に物流やeコマース企業にとって、電気商用車を採用する際の強力な魅力となっています。その一例がカナダと北米で、政府は2022年4月、小型・中型の電気自動車に対して5000米ドルの連邦政府リベートを発表しました。こうした取り組みにより、北米では2024年から2030年にかけて、電気商用車の需要が大幅に拡大すると予想されます。

- EV配備計画、魅力的な優遇措置、外国投資手当などの政府の取り組みは、北米各国の電気自動車市場を推進することになります。注目すべき動きとして、2022年3月、フォルクスワーゲンは北米に電気自動車製造施設を設立するため、70億米ドルという驚異的な資金を投じた。フォルクスワーゲンは2030年までに、米国、メキシコ、カナダの顧客向けに25の新型EVモデルを投入する計画です。その結果、電気自動車の需要は、2024年から2030年にかけて、北米各国で顕著な急増を見せると予測されています。

北米のバン産業概要

北米のバン市場はかなり統合されており、上位5社で93.82%を占めています。この市場の主要企業は以下の通り。 Daimler AG(Mercedes-Benz AG), Ford Motor Company, General Motors Company, GM Motor(Chevrolet)and Ram Trucking, Inc.(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- 一人当たりGDP

- 自動車購入のための消費者支出(cvp)

- インフレ率

- 自動車ローン金利

- シェアライド

- 電動化の影響

- EV充電ステーション

- バッテリーパック価格

- Xev新モデル発表

- 燃料価格

- OEM生産統計

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 推進タイプ

- ハイブリッド車と電気自動車

- 燃料カテゴリー別

- BEV

- PHEV

- ICE

- 燃料カテゴリー別

- ディーゼル

- ガソリン

- ハイブリッド車と電気自動車

- 国名

- カナダ

- メキシコ

- 米国

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Daimler AG(Mercedes-Benz AG)

- Fiat Chrysler Automobiles N.V

- Ford Motor Company

- General Motors Company

- GM Motor(Chevrolet)

- Nissan Motor Co. Ltd.

- Peugeot S.A.

- Ram Trucking, Inc.

- Toyota Motor Corporation

- Volkswagen AG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The North America Van Market size is estimated at 13.41 billion USD in 2025, and is expected to reach 16.67 billion USD by 2029, growing at a CAGR of 5.60% during the forecast period (2025-2029).

Steady growth is anticipated in North America's LCV market, fueled by economic development, evolving logistics needs, and a focus on sustainable transportation

- In 2023, the North American market for LCVs across all propulsion types exhibited a slight increase, with sales volumes reaching 4,055,770 units from 4,046,122 units in 2022. This growth, albeit modest, indicates a stabilizing market that continues to play a crucial role in supporting various sectors, including logistics, retail, and services, amid evolving economic and environmental landscapes. In 2024, sales are expected to reach 4,058,449 units, indicating a steady demand for LCVs in North America. This steady market performance underscores the essential role of LCVs in facilitating commerce and trade, reflecting the region's economic resilience and the diverse needs of its commercial sectors.

- The North American LCV market's modest growth aligns with broader trends, including economic recovery, a surge in e-commerce, and a heightened focus on sustainability. While the spotlight often falls on electric and hybrid vehicles, the demand for LCVs spans a spectrum of propulsion types, signaling a balanced shift toward cleaner transportation.

- From 2024 to 2030, the North American LCV market is poised for gradual expansion, with projections pointing to sales potentially reaching 4,473,267 units by the end of 2030. This growth is propelled by economic expansion, urbanization, and the surging demands of e-commerce, necessitating robust logistics. Moreover, as environmental concerns and advancements in vehicle efficiency gain traction, the market for electric and hybrid LCVs is poised for a notable increase, further shaping the commercial transportation landscape in North America.

The North American van market is witnessing significant growth, with distinct trends in each country pointing toward a rising preference for versatile and efficient transportation solutions

- Automakers are proactively exploring alternative fuel sources for their vehicles, driven by the dwindling petroleum supplies and escalating gasoline costs. The 2022 Russia-Ukraine conflict further exacerbated the already doubled petroleum prices over the past few decades, prompting a global push towards electric vehicles (EVs) for more economical everyday transportation. Tax rates also play a role in global fuel costs, with the US having the lowest fuel tax at 19% and India imposing a hefty 69% tax. These factors, combined with the rising fuel prices over the last two decades, underscore the appeal of EVs, which boast significantly lower operating costs compared to traditional internal combustion engine (ICE) vehicles.

- Electrifying their vehicle portfolios has become a paramount objective for automakers. Volvo aims for EVs to constitute 50% of its global sales by 2025. Subaru plans to introduce hybrid or electric versions for all its models by 2035. Ford is planning to invest a substantial USD 29 billion in EVs by 2025, while GM is allocating USD 27 billion, with a vision to electrify its entire light-duty vehicle lineup by 2035. Other manufacturers have set similar ambitions, albeit with varying timelines and targets, all united by their commitment to electrification.

- North America is set to witness the launch of 12 new electric vans between 2020 and 2028. Notably, the majority will be entirely new models, including the ELMS UD-1, Rivian R1A, and BrightDrop EV600. Additionally, established van lines like the Mercedes-Benz eSprinter and Ford Transit are also gearing up to introduce all-electric variants in the future.

North America Van Market Trends

Growing demand for electric vehicles in North America driven by government support and growing environmental concerns

- The CVP in Russia has experienced significant fluctuations in recent years. It climbed steadily from USD 208.2 million in 2017, peaking in 2019. However, it dipped to USD 193.9 million in 2020, largely due to the economic challenges brought on by the COVID-19 pandemic. Notably, the market rebounded sharply in 2022, reaching USD 269.8 million. This resurgence highlights both the resilience of the Russian automotive sector and the potential impact of economic stimulus measures and heightened consumer demand.

- Government incentives and subsidies are proving to be a strong draw for customers, particularly logistics and e-commerce firms, in their adoption of electric commercial vehicles. A case in point is Canada and North America, where, in April 2022, the government unveiled federal rebates of USD 5000 for electric light- and medium-duty vehicles. These initiatives are expected to significantly bolster the demand for electric commercial vehicles in North America from 2024 to 2030.

- Government initiatives, including plans for EV deployment, attractive incentives, and foreign investment allowances, are set to propel the electric vehicle market across North American nations. In a notable move, in March 2022, Volkswagen committed a staggering USD 7 billion to establish an electric car manufacturing facility in North America. By 2030, the automaker plans to roll out 25 new EV models, catering to customers in the US, Mexico, and Canada. As a result, the demand for electric vehicles is projected to witness a notable surge across various North American countries from 2024 to 2030.

North America Van Industry Overview

The North America Van Market is fairly consolidated, with the top five companies occupying 93.82%. The major players in this market are Daimler AG (Mercedes-Benz AG), Ford Motor Company, General Motors Company, GM Motor (Chevrolet) and Ram Trucking, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Impact Of Electrification

- 4.8 EV Charging Station

- 4.9 Battery Pack Price

- 4.10 New Xev Models Announced

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Propulsion Type

- 5.1.1 Hybrid and Electric Vehicles

- 5.1.1.1 By Fuel Category

- 5.1.1.1.1 BEV

- 5.1.1.1.2 PHEV

- 5.1.2 ICE

- 5.1.2.1 By Fuel Category

- 5.1.2.1.1 Diesel

- 5.1.2.1.2 Gasoline

- 5.1.1 Hybrid and Electric Vehicles

- 5.2 Country

- 5.2.1 Canada

- 5.2.2 Mexico

- 5.2.3 US

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Daimler AG (Mercedes-Benz AG)

- 6.4.2 Fiat Chrysler Automobiles N.V

- 6.4.3 Ford Motor Company

- 6.4.4 General Motors Company

- 6.4.5 GM Motor (Chevrolet)

- 6.4.6 Nissan Motor Co. Ltd.

- 6.4.7 Peugeot S.A.

- 6.4.8 Ram Trucking, Inc.

- 6.4.9 Toyota Motor Corporation

- 6.4.10 Volkswagen AG

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 202 Pages

- 納期

- 2~3営業日