|

市場調査レポート

商品コード

1693473

南米の飼料用種子の市場シェア分析、産業動向、成長予測(2025~2030年)South America Forage Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の飼料用種子の市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 209 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

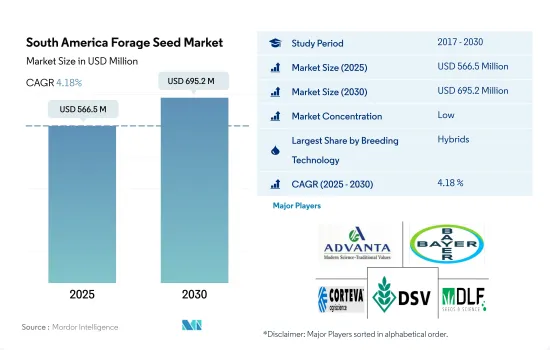

南米の飼料用種子市場規模は2025年に5億6,650万米ドルと推定され、2030年には6億9,520万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは4.18%で成長する見込みです。

飼料作物の栽培面積の増加や、畜牛業者がエタノール加工を施した非遺伝子組み換え種子を好むことが、同地域におけるハイブリッド種子需要の増加に寄与すると予想されます。

- 南米では、2022年の飼料作物の栽培面積は870万ヘクタールで、2017年は約780万ヘクタールでした。動物飼料需要の増加により、2017~2022年にかけて11.5%の増加です。

- 2022年には、飼料生産の原料として近隣諸国に輸出するための生産量の増加により、南米が世界の飼料種子市場の9.3%を占めます。

- ブラジルは飼料栽培用のハイブリッド種子の最大のユーザーであり、2022年にはこの地域のハイブリッド飼料生産面積の59.7%を占めます。しかし、アルゼンチンではトランスジェニックハイブリッドの普及が進んでいます。

- 非トランスジェニックハイブリッド種子を使用して生産された飼料用作物は牛に消化されやすいため、これを好む畜産家もいます。ブラジルではトウモロコシサイレージがトウモロコシエタノール生産に利用されており、飼料用トウモロコシはこの地域で最も急速に成長している作物となりました。

- 2022年の同国における、開放受粉品種とハイブリッド派生種子を用いた飼料作物の栽培シェアは26.1%でした。その大部分はブラキアリア属の在来牧草が占めています。

- ブラキアリア属の牧草は、自生しているか、農業従事者が2つの季節の間に余分な作物を栽培するための被覆作物や輪作作物として栽培されており、養分循環に役立っています。そのため、OPVはこれらの要因によって予測期間中に成長すると予想されます。しかし、商業的な栽培はハイブリッドや遺伝子組み換え品種によって行われており、投入量が少なくて済み、生産性も高いことから、南米では予測期間中にCAGR 2.4%を記録すると予想されています。

ブラジルは、飼料栽培に対する政府の支援プログラムと畜産業の旺盛な需要により、南米の飼料用種子市場で最大のシェアを占めています。

- ブラジルは、牛肉生産需要の増加、家畜人口の増加、飼料作物栽培に対する政府の支援プログラムにより、南米の飼料種子市場で最大の国となっています。

- 米国農務省によると、ブラジルの牛肉生産は、牛の入手可能性の増加と食肉処理場の利幅の改善により、2023~2030年にかけて増加すると推定されています。例えば、2021年のブラジルの牛の頭数は3億7,280万頭で、2017年から4.2%増加しました。家畜の増加は、同国における食肉需要を増加させ、飼料作物の生産を押し上げる可能性が高いです。

- アルゼンチンは、1人当たりの年間消費量が55kgと世界第2位の牛肉消費国であるため、予測期間中にCAGR 4.6%を記録すると予想されます。2019年、アルゼンチンには約400のと畜場がありました。過去数年間、消費の増加により、畜能力を高めるための産業投資が拡大しています。そのため、予測期間中、飼料需要が増加し、南米市場の成長を後押しすると予想されます。

- その他の南米市場は、これらの国々で入手可能な種子の品質が低いため、同地域で最も小さなシェアを占めているが、コロンビアとベネズエラのリアノスは南米における家畜の主要な商業中心地です。そのため、予測期間中に種子の需要は伸びると予想されます。

- したがって、飼料作物の栽培に資金を提供する政府支援、家畜人口の増加、この地域における食肉消費の増加が、予測期間中の飼料種子市場の成長を後押しする可能性があります。

南米の飼料用種子市場の動向

健康的な動物飼料の需要の増加、畜産業と食肉産業の成長が飼料作物の栽培面積を増加させています。

- 南米地域における牧畜業者、食肉産業、家畜の増加による需要の増加により、飼料作物の栽培面積は2017~2022年にかけて約13.6%増加しています。2022年には、アルファルファの耕作面積は飼料作物全体の耕作面積の約50.1%を占めます。このアルファルファの優位性は主に、家畜に健康的な飼料を提供する同作物の高タンパク質含有量に起因しています。

- 飼料作物の栽培面積が最も大きいのはアルゼンチンで、2022年には470万ヘクタールとなり、この地域の飼料作物栽培面積の53.9%を占めました。これに続くのがブラジルで同40.2%です。アルゼンチンが最大の飼料作付面積を有するにもかかわらず、アルゼンチンの業務用飼料作付面積はブラジルに比べて少ないです。例えば、アルゼンチンの飼料作物の商業栽培面積は50万ヘクタールで、ブラジルは2022年に110万ヘクタールでした。この差は、主にアルゼンチンの自然牧草地の面積が大きいことに起因しています。さらに、ブラジルの飼料面積は2017~2022年の間に約14.3%増加しています。この増加は主に、畜産業からの飼料作物に対する需要の増加に起因しています。さらに、ブラジルには2021年時点で約1,200万ヘクタールの荒廃牧草地があり、この牧草地を耕作牧草地に転換することで、新たな農地の必要性を減らしつつ、1,770万頭のウシの追加生産を生み出すことができます。このことは、予測期間中、同国の飼料作物栽培面積全体を押し上げる可能性があります。

- 畜産業からの飼料作物に対する需要の増加は、予測期間中、この地域の飼料作物全体の作付面積を押し上げると予想されます。

異なる気候条件と高い雑草濃度が、より広い適応性と除草剤耐性のアルファルファ種子形質への需要を促進しています。

- アルファルファは南米地域の主要飼料作物であり、主にアルゼンチンとブラジルで栽培されています。南米では、栽培されているアルファルファ品種の50%以上が病害抵抗性、除草剤耐性、様々な栽培条件への適応性を有しています。2019年、アルゼンチンは雑草の蔓延による収量減を軽減するため、遺伝子組み換え(GM)アルファルファの栽培を開始しました。Bioceresが開発したこれらの遺伝子組み換えアルファルファ品種は、グリホサート系除草剤に耐性があります。これらの除草剤耐性品種は雑草の蔓延を抑えるのに役立ち、その結果、作物の損失が20~30%減少します。現在、除草剤耐性品種はBayer AG、Corteva Agriscience、Limagrainによってこの地域で広く提供されています。

- 同様に、幅広い適応性と耐病性形質を持つアルファルファ品種に対する需要も高まっています。これらの形質により、作物は様々な生育条件に耐えることができ、根や冠の病害に対する抵抗性を得ることができます。DLF、S& W、Limagrain、Bayerなどの企業は、これらの複数の形質を持つ品種を種子で提供しています。DLFが市販しているこれらの形質を持つ品種には、PGW 931、ACA 903、Crioulaがあり、S& WはSW 3407、SW 6330、SW 10を提供しています。

- この地域で人気のあるその他のアルファルファの形質には、様々な季節に適した休眠性・非休眠性品種、耐宿根性、高乾物含量などがあります。その結果、病害の蔓延、雑草の個体数の増加、気候条件の変化が、これらの課題に対処するためにこれらの形質への需要を促進する主要因となっており、この需要は予測期間中も伸び続けると予想されます。

南米の飼料種子産業概要

南米の飼料用種子市場はセグメント化されており、上位5社で32.07%を占めています。この市場の主要企業は、Advanta Seeds-UPL、Bayer AG、Corteva Agriscience、Deutsche Saatveredelung AG、DLFなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 最も人気のある形質

- アルファルファ

- 育種技術

- 畑作物

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非トランスジェニックハイブリッド

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 作物

- アルファルファ

- 飼料用トウモロコシ

- 飼料用ソルガム

- その他の飼料作物

- 国名

- アルゼンチン

- ブラジル

- その他の南米

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- Bayer AG

- Corteva Agriscience

- Deutsche Saatveredelung AG

- DLF

- Groupe Limagrain

- KWS SAAT SE & Co. KGaA

- Peman

- Royal Barenbrug Group

- S& W Seed Co.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92536

The South America Forage Seed Market size is estimated at 566.5 million USD in 2025, and is expected to reach 695.2 million USD by 2030, growing at a CAGR of 4.18% during the forecast period (2025-2030).

Increasing forage crop cultivation area and cattlemen preferring non-transgenic seeds with ethanol processing are expected to help in increasing the demand for hybrid seeds in the region

- In South America, the area under the cultivation of forage crops in 2022 was 8.7 million hectares, which was about 7.8 million hectares in 2017. It is an increase of 11.5% from 2017 to 2022 due to an increase in the demand for animal feed.

- In 2022, South America accounted for 9.3% of the global forage seed market due to the increase in the production for export to neighboring countries as a raw material for feed production.

- Brazil is the largest user of hybrid seeds for forage cultivation, which accounted for 59.7% of the region's hybrid forage production area in 2022. However, transgenic hybrid penetration is more prevalent in Argentina.

- Some cattlemen have a preference for forage crops produced using non-transgenic hybrid seeds because they are easily digestible by the cattle. Corn silage is being used for corn ethanol production in Brazil, which led to forage corn becoming the fastest-growing crop in the region.

- The share of forage crops cultivated using open-pollinated varieties and hybrid derivative seeds in the country was 26.1% in 2022. It is largely contributed by native grasses of the Brachiaria genus.

- The Brachiaria grasses are grown either wild or as cover crops or rotation crops for extra for farmers between two seasons, which helps in nutrient cycling. Therefore, OPVs are expected to grow over the forecast period owing to those factors. However, commercial cultivation is done by hybrids and GM varieties that require lesser inputs and more productivity, which is expected to register a CAGR of 2.4% in South America during the forecast period.

Brazil holds the largest share of the South American forage seed market due to government support programs for forage cultivation and robust demand from the livestock industry

- Brazil is the largest country in the South American forage seed market due to the increased demand for beef production, the growing livestock population, and government support programs for the cultivation of forage crops.

- According to the USDA, beef production in Brazil is estimated to grow from 2023 to 2030 due to the increasing availability of cattle and improved margins for slaughterhouses. For instance, the number of cattle in Brazil was 372.8 million in 2021, an increase of 4.2% from 2017. The increasing livestock will likely increase the demand for meat in the country and boost the production of forage crops.

- Argentina is anticipated to register a CAGR of 4.6% during the forecast period as it is globally the second-highest consumer of beef, with a yearly consumption of 55 kg per person. In 2019, Argentina had about 400 slaughter plants. Over the past several years, industry investments have grown to increase slaughter capacity due to increasing consumption. Therefore, the demand for feed is expected to increase and boost the market's growth in South America during the forecast period.

- The Rest of South American market held the smallest share in the region because of the low-quality seeds available in these countries, but the Lianos of Colombia and Venezuela are major commercial centers for livestock in South America. Therefore, the demand for seeds is anticipated to grow during the forecast period.

- Therefore, government support in funding the cultivation of forage crops, an increase in the livestock population, and increasing meat consumption in the region may boost the growth of the forage seed market during the forecast period.

South America Forage Seed Market Trends

An increase in the demand for healthy animal feed, growing livestock farming and meat industry are driving the cultivation area for forage crops

- The area cultivated under forage crops has increased by about 13.6% between 2017 and 2022 because of the increase in the demand by cattlemen, the meat industry, and the increase in livestock in the South American region. In 2022, the cultivated area for alfalfa was about 50.1% of the total cultivated area of forage crops. This domination of alfalfa is mainly attributed to the crop's high protein content, which provides healthy feed for livestock.

- Argentina held the largest area under forage crops, with 4.7 million hectares in 2022, which accounted for 53.9% of the region's forage crop area. This is followed by Brazil with 40.2% in the same year. Despite Argentina holding the largest area under forage cultivation, the commercial forage cultivation area is less in Argentina compared to Brazil. For instance, the commercial cultivation area of forage crops in Argentina was 0.5 million hectares compared to Brazil, which had 1.1 million hectares in 2022. This variation is mainly attributed to the large area of natural pastures in Argentina. Furthermore, the forage area in Brazil has increased by about 14.3% between 2017 and 2022. This increase is mainly attributed to the growing demand for the forage crops from the livestock industry. Moreover, Brazil had about 12.0 million hectares of degraded pasture land as of 2021, and the conversion of this pasture to cultivated pastures could generate an additional production of 17.7 million bovines while reducing the need for new agricultural land. This may drive the overall forage crop area in the country during the forecast period.

- The increasing demand for forage crops from the livestock industries is anticipated to drive the overall forage crop area in the region during the forecast period.

Different climatic conditions and higher weed concentrations are driving the demand for wider adaptability and herbicide-tolerant alfalfa seed traits

- Alfalfa is the primary forage crop in the South American region, predominantly grown in Argentina and Brazil. In South America, over 50% of the alfalfa varieties cultivated possess disease resistance, herbicide tolerance, and adaptability to various growing conditions. In 2019, Argentina began cultivating genetically modified (GM) alfalfa to mitigate yield losses caused by weed infestations. These GM alfalfa varieties, developed by Bioceres, are tolerant to glyphosate herbicides. These herbicide-tolerant cultivars help reduce weed infestations, resulting in a 20-30% reduction in crop losses. Currently, herbicide-tolerant varieties are widely offered in the region by Bayer AG, Corteva Agriscience, and Limagrain.

- Similarly, there is a growing demand for alfalfa varieties with wider adaptability and disease-resistant traits. These traits enable crops to withstand various growing conditions and provide resistance to root and crown diseases. Companies such as DLF, S&W, Limagrain, and Bayer offer varieties with these multiple traits in their seeds. Some commercially available varieties with these traits from DLF include PGW 931, ACA 903, and Crioula, while S&W offers SW 3407, SW 6330, and SW 10.

- Other popular alfalfa traits in the region include dormant and non-dormant cultivars suitable for different seasons, lodging resistance, and high dry matter content. Consequently, the increasing prevalence of diseases, weed populations, and changing climatic conditions are major factors driving the demand for these traits to combat these challenges, and this demand is anticipated to continue growing during the forecast period.

South America Forage Seed Industry Overview

The South America Forage Seed Market is fragmented, with the top five companies occupying 32.07%. The major players in this market are Advanta Seeds - UPL, Bayer AG, Corteva Agriscience, Deutsche Saatveredelung AG and DLF (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Alfalfa

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Alfalfa

- 5.2.2 Forage Corn

- 5.2.3 Forage Sorghum

- 5.2.4 Other Forage Crops

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 Deutsche Saatveredelung AG

- 6.4.5 DLF

- 6.4.6 Groupe Limagrain

- 6.4.7 KWS SAAT SE & Co. KGaA

- 6.4.8 Peman

- 6.4.9 Royal Barenbrug Group

- 6.4.10 S&W Seed Co.

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms