|

市場調査レポート

商品コード

1693469

アジア太平洋地域の飼料用種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia-Pacific Forage Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の飼料用種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 238 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

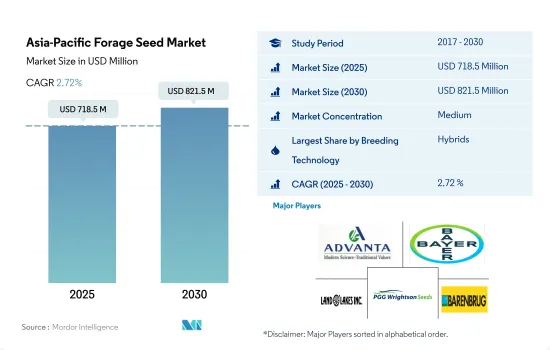

アジア太平洋地域の飼料種子市場規模は2025年に7億1,850万米ドルと予測され、2030年には8億2,150万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは2.72%で成長すると予測されます。

高収量と動物への嗜好性によりハイブリッド種子がこの地域の飼料用種子市場を独占

- アジア太平洋地域では、ハイブリッド種子が、露地受粉品種やハイブリッド派生品種と比較して、数量および金額で飼料用種子市場を独占しています。2022年には、ハイブリッド飼料用種子が同地域の飼料用種子市場の80.6%のシェアを占め、2017年から2022年の間に22.3%の大幅な伸びを示しました。これは高収量、早熟、家畜への嗜好性の高さによるものです。

- 2022年には、ハイブリッド種子セグメントの中で非遺伝子組み換えハイブリッド種子が市場を独占し、この地域では99%以上を占めました。これは主に、遺伝子組換え形質が家畜や動物の健康に及ぼす影響が認識され、インドを含む主要国では遺伝子組換え作物が禁止されているため、遺伝子組換え種子と比較して非遺伝子組換え種子が多く使用されているためです。

- 2022年には、非遺伝子組換えハイブリッド種子の中でアルファルファが主要作物であり、市場における金額シェアは19.9%、次いで飼料用トウモロコシが10.1%でした。これはアルファルファの栽培面積が大きいことと、インド、バングラデシュ、パキスタンなど一部の国で遺伝子組み換えアルファルファが禁止されていることによる。

- 2022年の同地域の飼料用種子市場では、開放受粉品種とハイブリッド派生品種が19.4%のシェアを占めました。アルファルファは、この地域のOPVの45.6%のシェアを占め、このセグメントをリードしています。大量の種子を必要とし、ハイブリッド技術革新が不足しているため、アジア太平洋地域ではアルファルファ、飼料用ソルガム、その他の飼料作物においてOPVが普及しています。

- 最も急速に成長しているのはインドで、この地域のOPVシェアは36.1%です。ハイブリッドに比べてシェアが低いのは、主に生産性が低いためです。

- そのため、ハイブリッド種子以下の非遺伝子組み換え飼料用種子が市場を独占しています。以上のことから、市場は予測期間中に成長すると予想されます。

日本がこの地域の飼料用種子市場を独占、国内の家畜人口増加により栽培面積が増加

- 2022年、アジア太平洋地域は世界の飼料用種子市場の15.1%を占めました。飼料加工産業からの飼料需要の増加により、市場額は2017年から2022年の間に19.4%増加しました。

- 日本は飼料用種子の最大の消費国であり、主に栽培の増加と飼料産業からの需要の増加により、2022年には同地域の飼料用種子市場の48.8%の市場シェアを占めました。

- インドではアルファルファが主要作物として消費され、2022年にはアジア太平洋地域の飼料用種子市場の25%を占める。需要が高いのは、生産面積が多く、牛の頭数が増加しているためです。例えば、牛の頭数は2017年の3億頭から2021年には3億500万頭以上に増加しており、これは主に乳製品と肉製品の需要増加によるものです。したがって、需要の増加により耕作面積が増加し、種子市場を牽引すると推定されます。

- 2022年には、日本を除けば、インド、オーストラリア、中国などの国々が合計で44.6%の最大市場シェア値を占めたが、これは主にこれらの国々における畜牛人口の増加と飼料需要の増加によるものです。

- 日本では、農林水産省が2030年までに飼料自給率を77%から100%に引き上げるという目標を掲げています。国内の飼料生産を支援するため、農林水産省は飼料作物や飼料用作物を作付する生産者に支援金を支給しています。そのため、同国では今後数年間、種子の需要が高まると予測されています。

- 増産のための政府支援、商業用種子の採用増加、飼料用種子の需要拡大などの要因が、予測期間中に同地域の市場を押し上げると予測されます。

アジア太平洋地域の飼料用種子市場の動向

酪農場からの高品質飼料に対する需要の増加と、飼料作物の維持管理の容易さが栽培面積を増加させています。

- アジア太平洋地域で栽培されている主な飼料作物には、アルファルファ、飼料用ソルガム、飼料用トウモロコシ、その他の牧草が含まれます。2022年の飼料作物の栽培面積は、同地域の連作作物総栽培面積の約1.7%を占めました。2016年から2019年にかけて、大豆やトウモロコシを含む他の収益性の高い作物への作物シフトにより、飼料作物の総栽培面積は減少しました。しかし、家畜からの飼料需要の増加と酪農産業の開発により、2020年から2022年にかけて面積が増加しました。そのため、2020年から2022年の間に面積は約3.2%増加しました。

- アルファルファはこの地域で栽培されている主要な飼料作物のひとつで、2022年の栽培面積は650万ヘクタールです。アルファルファの栽培面積は2017年から2022年の間に0.4%増加しました。様々な天候や土壌条件のもとで、豊富なタンパク質と魅力的な飼料を生産するその卓越した能力による作付面積の増加です。さらに、2022年には飼料用ソルガムの栽培面積は290万ヘクタールとなりました。この地域における飼料用ソルガム栽培の93.4%をインドが占め、2022年には270万ヘクタールとなります。家畜頭数の多さと飼料需要の高まりが栽培拡大の主な要因です。例えば、インドの牛の頭数は2017年の1億9,040万頭から2021年には1億9,340万頭に増加します。

- アジア太平洋地域では、インドが飼料作物の栽培面積の52.9%を占め、最大の面積を占めているが、これは同国が畜産業からの需要が高いためです。そのため、農家は需要を満たすために飼料作物の栽培面積を拡大せざるを得ず、それによって飼料用種子の売上が増加しています。

畜産における飼料需要の増加は、耐病性、幅広い適応性、早熟の特徴を持つハイブリッド飼料種子の使用を促進しています。

- アルファルファと飼料用トウモロコシは、消化率が高く高タンパク質であるなど、家畜の飼育に有利であることから、主要な飼料作物となっています。また、農家は品質を犠牲にすることなく、より高い収量を達成することができます。アルファルファは、天候の変化、早熟に対する需要の高さ、異なる投入資材の使用を最小限に抑えるために単一製品でリグニン含有量が低いことから、適応性の広さが最も採用された形質でした。

- アルファルファの最も一般的で有害な菌類病害は、フザリウムと褐斑病です。これらは植物の生産性を30%以上低下させる。そのため、アルファルファ生産者がより高い生産性を達成するためには、耐病性形質を持つアルファルファ品種への需要が高まっています。さらに、低リグニン形質のアルファルファは消化性が高く、収量が15~20%増加するため、日本では低リグニン形質のアルファルファが栽培されています。したがって、低リグニン形質を持つアルファルファの需要は、予測期間中にこの地域で増加すると予想されます。

- 高収量ポテンシャル、耐乾性、耐病性、早熟性、耐宿宿根性の形質を持つ飼料用コーンは需要が高いです。これらの形質のうち、早熟形質は畜産業で高い需要があるため、最大のシェアを占めています。この需要に応えるため、生産者はオフシーズンに作物を栽培し、通常の栽培よりも栽培期間を1~2週間短縮します。例えば、Land O'Lakes社は、干ばつ耐性と早熟の特徴を持つ約44の製品を提供しています。

- 病害による損失の増加を防ぎ、短期間で生産性を向上させるため、耐病性、早熟性、干ばつ耐性などの形質を持つ種子が市場の成長を後押ししています。

アジア太平洋地域の飼料種子産業の概要

アジア太平洋地域の飼料用種子市場は適度に統合されており、上位5社で58.53%を占めています。この市場の主要企業は以下の通りです。 Advanta Seeds-UPL, Bayer AG, Land O'Lakes Inc., PGG Wrightson Seeds(DLF)and Royal Barenbrug Group(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 最も人気のある品種

- アルファルファと飼料用トウモロコシ

- 育種技術

- 畑作物

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非遺伝子組み換え雑種

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 作物

- アルファルファ

- 飼料用トウモロコシ

- 飼料用ソルガム

- その他の飼料作物

- 国名

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- Ampac Seed Company

- Bayer AG

- Cates Grain and Seeds Ltd

- Corteva Agriscience

- Groupe Limagrain

- Kaveri Seeds

- Land O'Lakes Inc.

- PGG Wrightson Seeds(DLF)

- Royal Barenbrug Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

The Asia-Pacific Forage Seed Market size is estimated at 718.5 million USD in 2025, and is expected to reach 821.5 million USD by 2030, growing at a CAGR of 2.72% during the forecast period (2025-2030).

Hybrids dominated the region's forage seed market due to higher yield and palatability to animals

- In Asia-Pacific, hybrid seeds dominate the forage seed market in terms of volume and value compared to open-pollinated varieties and hybrid derivatives. In 2022, hybrid forage seeds held an 80.6% share of the region's forage seed market, which showed a significant growth of 22.3% between 2017 and 2022. It is due to the high yield, early maturity, and higher palatability to livestock.

- In 2022, non-transgenic hybrid seeds dominated the market among the hybrid seed segment, with more than 99% in the region. This is mainly due to the large use of non-transgenic seeds compared to GMO seeds because of the perceived effects of transgenic traits on livestock and animal health and the ban on transgenic crops in major countries, including India.

- In 2022, among the non-transgenic hybrid seeds, alfalfa was the major crop, holding a 19.9% value share in the market, followed by forage corn with 10.1%. This is due to the larger area under alfalfa cultivation and the ban on transgenic alfalfa in some countries such as India, Bangladesh, and Pakistan.

- Open-pollinated varieties and hybrid derivatives accounted for a 19.4% share of the region's forage seed market in 2022. Alfalfa leads the segment, which accounted for a 45.6% share of OPV in the region. Due to the high-volume seed requirements and lack of hybrid innovations, OPVs are more prevalent in forage crops such as alfalfa, forage sorghum, and other forages in the Asia-Pacific region.

- India is the fastest-growing country, with 36.1% of the region's OPV share. The lower share compared to hybrids is mainly due to low productivity.

- Therefore, non-transgenic forage seeds under hybrid seeds dominate the market. With the aforementioned facts, the market is anticipated to grow during the forecast period.

Japan dominated the forage seed market in the region, with a higher area under cultivation due to increased livestock population in the country

- In 2022, Asia-Pacific accounted for 15.1% of the global forage seed market. The market value increased by 19.4% between 2017 and 2022 due to the increased demand for forage from feed processing industries.

- Japan is the largest consumer of forage seeds and held a market share of 48.8% of the region's forage seed market in 2022, mainly due to increased cultivation and rising demand from the feed industry.

- In India, alfalfa is the major crop consumed, accounting for 25% of the Asia-Pacific forage seed market in 2022. The higher demand was due to the high production area and increased cattle population. For instance, the cattle population increased from 300 million heads in 2017 to more than 305 million heads in 2021, mainly due to the increased demand for dairy and meat products. Therefore, increased demand is estimated to increase the area under cultivation, thus driving the seed market.

- In 2022, apart from Japan, other countries such as India, Australia, and China together held the maximum market share value of 44.6%, mainly due to the higher cattle population in these countries and higher demand for feed.

- In Japan, the Ministry of Agriculture, Forestry and Fisheries (MAFF) set a goal of increasing forage self-sufficiency from 77% to 100% by 2030. To support forage production in the country, MAFF provides support payments to growers who plant forage and feed crops. Therefore, the demand for seeds is projected to rise in the country in the coming years.

- Factors such as government support to increase production, the rising adoption of commercial seeds, and the growing demand for forage seeds are estimated to boost the market in the region during the forecast period.

Asia-Pacific Forage Seed Market Trends

An increase in demand for high-quality fodder from dairy farms and easier maintenance of forage crops is driving the area under cultivation

- The major forage crops grown in the Asia-Pacific region include alfalfa, forage sorghum, forage corn, and other grasses. Forage crops accounted for about 1.7% of the region's total row crop cultivation area in 2022. The total forage area decreased from 2016 to 2019 due to the crop shift to other profitable crops, including soybeans and corn. However, the increasing demand for forage from livestock and the development of the dairy industry caused the increase in area from 2020 to 2022. Therefore, the area increased by about 3.2% between 2020 and 2022.

- Alfalfa is one of the major forage crops cultivated in the region, with an area of 6.5 million hectares in 2022. The area under alfalfa increased by 0.4% between 2017 and 2022. Increase in acreages due to its exceptional capacity to produce abundant amounts of protein and attractive forage under various weather and soil conditions. Additionally, In 2022, the area under forage sorghum cultivation was 2.9 million hectares. India accounted for 93.4% of forage sorghum cultivation in the region, with 2.7 million ha in 2022. High livestock population and rising demand for animal forage are the main factors leading to increased cultivation. For instance, the number of cattle in India increased from 190.4 million stocks in 2017 to 193.4 million in 2021.

- In Asia-Pacific, India has the largest area under forage crops, accounting for 52.9% of the forage crop acreage because of the country's high demand from the livestock industry. Therefore, these factors force farmers to expand the area under forage crops to meet the demand, thereby increasing the sales of forage seeds.

Increasing demand for fodder in livestock farming is driving the usage of hybrid forage seeds having disease resistant, wider adaptability, and early maturity traits

- Alfalfa and forage corn are the major forage crops because of their benefits to livestock rearing, such as more digestibility and high protein. They also allow farmers to attain greater yields without sacrificing quality. Wider adaptability for alfalfa was the largest adopted trait as there have been weather changes, high demand for early maturity, and low lignin content in a single product to minimize the usage of different inputs.

- The most common and harmful fungal diseases of alfalfa are fusarium and brown spot. They can reduce the productivity of plants by 30% or more. Therefore, the demand for alfalfa varieties with disease-resistant traits increases for alfalfa growers to achieve higher productivity. Additionally, alfalfa with low lignin traits is cultivated in Japan as the low-lignin trait alfalfa is highly digestible, and it offers a 15-20% increase in yield. Therefore, the demand for alfalfa with low lignin traits is expected to increase in the region during the forecast period.

- Forage corn with high yield potential, drought tolerance, disease tolerance, early maturity, and lodging tolerance traits are in high demand. Among these traits, the early maturity trait had the largest share as it has a high demand in the livestock industry. To meet this demand, the growers cultivate the crop in the off-season and reduce the cultivating period to normal cultivation by 1-2 weeks than normal cultivation. For instance, Land O' Lakes provides about 44 products with drought tolerance and early maturity traits.

- To prevent the increasing losses from diseases and increase productivity in a shorter period, the seeds with traits such as disease resistance, early maturity, and drought tolerance are fueling the market's growth.

Asia-Pacific Forage Seed Industry Overview

The Asia-Pacific Forage Seed Market is moderately consolidated, with the top five companies occupying 58.53%. The major players in this market are Advanta Seeds - UPL, Bayer AG, Land O'Lakes Inc., PGG Wrightson Seeds (DLF) and Royal Barenbrug Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Alfalfa & Forage Corn

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Alfalfa

- 5.2.2 Forage Corn

- 5.2.3 Forage Sorghum

- 5.2.4 Other Forage Crops

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 Bangladesh

- 5.3.3 China

- 5.3.4 India

- 5.3.5 Indonesia

- 5.3.6 Japan

- 5.3.7 Myanmar

- 5.3.8 Pakistan

- 5.3.9 Philippines

- 5.3.10 Thailand

- 5.3.11 Vietnam

- 5.3.12 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Ampac Seed Company

- 6.4.3 Bayer AG

- 6.4.4 Cates Grain and Seeds Ltd

- 6.4.5 Corteva Agriscience

- 6.4.6 Groupe Limagrain

- 6.4.7 Kaveri Seeds

- 6.4.8 Land O'Lakes Inc.

- 6.4.9 PGG Wrightson Seeds (DLF)

- 6.4.10 Royal Barenbrug Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms