|

市場調査レポート

商品コード

1693456

北米の飼料用種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)North America Forage Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の飼料用種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 213 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

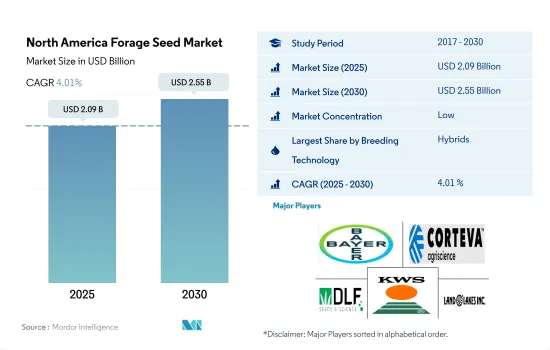

北米の飼料用種子市場規模は2025年に20億9,000万米ドルと推定され、2030年には25億5,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは4.01%で成長すると予測されます。

さまざまな産業における飼料の開発と急速なハイブリッド開発が北米の飼料用種子市場を牽引しています。

- 2022年には、非遺伝子組み換えハイブリッド飼料用種子がこの地域のハイブリッド飼料用種子市場の96.8%を占める最大のサブセグメントでした。これは、トランスジェニック形質が家畜と動物の健康に及ぼす影響が認識されているためです。さらに、遺伝子組み換えハイブリッドに関連するコストも、農家が遺伝子組み換えハイブリッドの採用を思いとどまる主な要因の1つです。

- しかし、農家が飼料を消化しやすくする形質を持つ遺伝子組み換え飼料作物を栽培するようになり、動向に変化が生じています。したがって将来的には、遺伝子組み換え作物分野は、遺伝子組み換えでないハイブリッド作物とともに成長すると予想されます。

- アルファルファとトウモロコシは飼料作物の中で最もハイブリッド化されており、それぞれ2022年のハイブリッド飼料用種子市場の16.9%と4.3%を占めています。

- 米国は北米ハイブリッド飼料用種子市場の主要国で、2022年には55%を占める。同国の圧倒的なシェアは、高い代替率と農家からの高い需要のためです。さらに、同国の農家は農場規模が大きいため、ハイブリッド種子を購入する余裕があります。しかし、カナダは遺伝子組み換えハイブリッドの使用に比較的反対であり、大多数の農家が飼料作物を輪作作物とみなし、省農地作物やOPVを好むため、OPVの使用に関してはカナダが最も重要な国でした。

- したがって、遺伝子組み換えハイブリッドに関連する利点を理解する農家の認識へのシフトと、酪農や加工産業からの需要を満たすための収量向上のための新しいハイブリッドの開発が、予測期間中にCAGR 3.8%でこの地域のハイブリッド・セグメントを牽引すると推定・予測されます。

カナダは最も成長著しい国であり、政府からの支援も増加しているため、市場を独占しています。

- 飼料としての飼料需要の増加、食肉消費、気象条件により、2022年の北米種子市場の8.1%を飼料用種子分野が占める。同地域では、飼料作物は栄養分の供給や土壌活力の回復、灌漑に必要な水の減少、先進技術を用いた栽培への投資といった利点から好まれています。

- 飼料用種子の需要はカナダで高く、2022年には8億6,360万米ドルを占めました。同国のシェアが高いのは、飼料としての飼料の需要が高いことと、同国の牛の頭数が増加しているためです。さらに、同国の商業用飼料用種子の栽培面積は、他の北米諸国と比較して2022年には310万haでした。

- カナダでは、アルファルファが主要な飼料作物であり、政府の支援や酪農・食肉加工産業による家畜の飼料需要の増加などの要因により、2022年には飼料用種子市場の23%を占めました。例えば、2021年にカナダ政府は、アルファルファ生産者に、より高い収量を生産し、アルファルファの冬の生存率を向上させるのに役立つ先進技術を装備させるために約260万米ドルを投資しました。

- 米国も主要国のひとつであり、2022年には6億8,600万米ドルを計上し、牛の頭数も増加しています。例えばFAOによると、米国の牛の数は2017年の9,360万頭から2021年には9,380万頭に増加します。

- したがって、加工・酪農産業からの飼料需要の増加、少ない水条件での栽培能力、より高い利益などが、予測期間中にCAGR 4.1%で同地域の飼料用種子市場を牽引すると予測されます。

北米の飼料用種子市場の動向

家畜頭数の増加と飼料用種子市場からの需要の増加が栽培面積の増加につながっています。

- 北米で栽培されている主な飼料作物には、アルファルファ、飼料用トウモロコシ、飼料用ソルガムなどがあります。2022年のこの地域の総栽培面積に占める飼料作物の割合は約13.9%でした。飼料作物の総栽培面積は2017年から2022年の間に約6.6%増加しました。この増加は主に、酪農家やその他の畜産部門からの高品質な飼料要求に対する需要の増加に起因すると考えられます。

- 米国は北米で最大の飼料作物栽培面積を有し、約1,430万ヘクタールで、2022年の同地域の飼料作物栽培面積の約60.1%を占めました。これは主に、大規模な畜産部門があるため、同国の飼料作物に対する需要が高いことに起因しています。例えば、米国では2022年時点で約8,930万頭の牛と子牛が飼育されています。このような大規模な畜産人口が、同国における飼料栽培全体を牽引すると予想されます。

- アルファルファはこの地域で栽培されている主要な飼料作物であり、2022年の栽培面積は約1,150万ヘクタールでした。アルファルファの栽培面積が大きいのは、主にこの作物に適した土壌と気候条件、そして高い収益によるものです。さらに、米国、カナダ、メキシコなどの国々では、除草剤耐性、抗生物質耐性、リグニン含有量の変化など様々な改良形質を持つ遺伝子組み換え(GM)アルファルファの商業栽培が承認されています。これにより、この地域の農家はアルファルファ作物の栽培を奨励すると予想されます。

- 様々な畜産業における需要の増加と、米国などの国々における家畜人口の多さが、予測期間中に飼料作物全体の作付面積を押し上げると予想される主な要因です。

悪天候下での高収量を目的とした耐病性、耐虫性、耐乾性アルファルファ種子の採用が増加中

- アルファルファは北米で栽培されている主要な飼料作物です。アルファルファの需要の高い形質は、耐病性、耐虫性、そして畜産業向けの飼料/サイレージの品質を向上させるための幅広い適応性です。より広い適応性は、気象条件の変化や早熟による高収量への要求から、生産者が採用した最大の形質です。さらに、タンパク質含量の増加、四季を通じた生育、リグニン含量の低減といった他の形質も今後普及が見込まれ、飼料の品質が向上します。

- アルファルファの一般的な形質には、枯れ病や根腐れ病に対する耐病性、異なる季節や土壌条件への幅広い適応性、干ばつ耐性、昆虫や線虫に対する耐性などがあります。例えば、アルファルファ品種の形質を提供・販売している主な企業は、Ampac Seed Company(Attention II)、KWS SAAT SE &Co.KGaG(HarvXtra、Standfast)、バイエルクロップサイエンス(Roundup-Ready)、シンジェンタAG(NEXGROW)、DLF(Fortune)などがあります。

- ネブラスカ州、カンザス州、オクラホマ州、テキサス州、ニューメキシコ州、オレゴン州などでは2022年以降、深刻な干ばつが続いています。2023年には、これらの州の土地の約12%が極端な干ばつに見舞われていました。したがって、干ばつ耐性形質は予測期間中に人気を集めると予想されます。

- 家畜飼料の改善に対する需要の増加や、病気に対する耐性や収量の増加といった多くの利点といった要因が、この地域における市場の成長を促進すると予想されます。

北米の飼料用種子産業の概要

北米の飼料用種子市場は断片化されており、上位5社で37.48%を占めています。この市場の主要企業は以下の通りです。 Bayer AG, Corteva Agriscience, DLF, KWS SAAT SE & Co. KGaA and Land O'Lakes Inc.(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 最も人気のある形質

- アルファルファ

- 育種技術

- 畑作物

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非遺伝子組み換え雑種

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 作物

- アルファルファ

- 飼料用トウモロコシ

- 飼料用ソルガム

- その他の飼料作物

- 生産国

- カナダ

- メキシコ

- 米国

- その他北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- Ampac Seed Company

- Bayer AG

- Corteva Agriscience

- DLF

- Groupe Limagrain

- KWS SAAT SE & Co. KGaA

- Land O'Lakes Inc.

- Royal Barenbrug Group

- S&W Seed Co.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92518

The North America Forage Seed Market size is estimated at 2.09 billion USD in 2025, and is expected to reach 2.55 billion USD by 2030, growing at a CAGR of 4.01% during the forecast period (2025-2030).

Application of forages in different industries and the rapid hybrid development are driving the forage seed market in North America

- In 2022, the non-transgenic hybrid forage seed was the largest sub-segment which accounted for 96.8% of the hybrid forage seeds market in the region. This is because of the perceived effect of transgenic traits on livestock and animal health. Additionally, the cost associated with transgenic hybrids is also one of the major factors to discourage farmers from adopting GM hybrids.

- However, there is a change in the trend as farmers cultivate transgenic forage crops with traits that make feed easy to digest. Therefore, in the future, the transgenic segment is anticipated to see growth along with non-transgenic hybrids.

- Alfalfa and corn are the most hybridized among the forage crops which accounted for 16.9% and 4.3% of the hybrid forage seed market in 2022 respectively as they have more demand in the processing industry in pellet feeds and ethanol production, respectively in the region.

- The United States was the major country concerning the North American hybrid forage seed market which accounted for 55% in 2022. The dominant share of the country was because of the high replacement rate and higher demand from farmers. Moreover, farmers in the country can afford to buy hybrid seeds owing to their large farm sizes. However, Canada was the most significant country concerning the usage of OPVs as Canada is relatively against the usage of transgenic hybrids and the majority of farmers see forage crops as rotational crop and prefers farm-saved and OPVs.

- Therefore, the shift in farmers' perception towards transgenic hybrids realizing the benefits associated with it, and the development of new hybrids to improve yield to meet demand from dairy and processing industries are estimated to drive the hybrid segment in the region at a CAGR of 3.8% during the forecast period.

Canada dominates the market as it is the fastest-growing country, with increasing support from the government

- The forage seed segment accounted for 8.1% of the North American seed market in 2022 due to increased demand for forage as feed, meat consumption, and weather conditions. In the region, forage crops are preferred for benefits such as providing nutrients and restoring soil vigor, less water required for irrigation, and investments in cultivation using advanced technologies.

- The demand for forage seeds was higher in Canada, accounting for USD 863.6 million in 2022. The higher share of the country was due to the high demand for forage as feed and the increase in the cattle population in the country. Moreover, the area under commercial forage seeds in the country was 3.1 million ha in 2022 compared to other North American countries.

- In Canada, alfalfa was the major forage crop, which accounted for 23% of the forage seed market in 2022 due to factors such as the government's support and an increase in the demand for feeding animals by the dairy and meat processing industries. For instance, in 2021, the Canadian government invested about USD 2.6 million to equip alfalfa growers with advanced technologies that help produce higher yields and improve alfalfa's winter survival rates.

- The United States was also one of the major countries, registering USD 686 million in 2022 and a rising cattle population. For instance, according to FAO, the number of cattle in the United States increased from 93.6 million in 2017 to 93.8 million in 2021.

- Therefore, the increasing demand for forages from processing and dairy industries, the ability to cultivate in less water conditions, and higher profits are estimated to drive the forage seed market in the region at a CAGR of 4.1% during the forecast period.

North America Forage Seed Market Trends

Rising cattle populations and growing demand from the forage seed market have led to an increase in the cultivation area

- The major forage crops grown in North America include alfalfa, forage corn, and forage sorghum. Forage crops accounted for about 13.9% of the region's total cultivation area in 2022. The total forage area increased by about 6.6% between 2017 and 2022. This increase could be mainly attributed to the increased demand for the quality forage requirement from dairy farmers or other livestock sectors.

- The United States held the largest area under forage crops in North America, with about 14.3 million hectares, accounting for about 60.1% of the region's forage crop area in 2022. This was mainly attributed to the high demand for the forage crops in the country due to the large livestock sector. For instance, there were about 89.3 million heads of cattle and calves in US farms as of 2022. This large livestock population is anticipated to drive the overall forage cultivation in the country.

- Alfalfa is the major forage crop cultivated in the region; it had a cultivation area of about 11.5 million hectares in 2022. The large cultivation area of alfalfa was mainly due to the well-suitable soil and climatic conditions for the crop and higher returns. Moreover, the commercial cultivation of transgenic (GM) alfalfa with various improved traits such as herbicide tolerance, antibiotic resistance, and altered lignin content in countries such as the United States, Canada, and Mexico has been approved. This is anticipated to encourage the farmers to cultivate alfalfa crops in the region.

- The increasing demand for the various livestock industries and the large livestock population in countries such as the United States are the major factors anticipated to drive the overall forage crop acreage during the forecast period.

The adoption of disease-resistant, insect-resistant, and drought-resistant alfalfa seeds for high yield during adverse climatic conditions is rising

- Alfalfa is a major forage crop cultivated in North America. The high-demand traits of alfalfa are disease resistance, insect resistance, and wider adaptability for improving the quality of the feed/silage for the livestock industry. Wider adaptability was the largest trait adopted by growers as there have been changes in weather conditions and demand for high yields with early maturity. Furthermore, other traits such as increasing protein content, growing throughout the seasons, and reducing lignin content are expected to gain popularity in the future, increasing forage quality.

- Popular traits of Alfalfa include disease resistance to wilts and root rots, wider adaptability to different seasons and soil conditions, drought tolerance, and resistance to insects and nematodes. For instance, major companies offering and marketing the traits of alfalfa varieties are Ampac Seed Company (Attention II), KWS SAAT SE & Co. KGaG (HarvXtra, Standfast), Bayer Crop Science (Roundup-Ready), Syngenta AG (NEXGROW), and DLF (Fortune) for resistance to diseases such as Colletotrichum trifolii and Verticillium wilt.

- Drought tolerance is the second-most popular trait among growers, as states such as Nebraska, Kansas, Oklahoma, Texas, New Mexico, and Oregon have been experiencing severe drought since 2022. About 12% of the land in these states was experiencing extreme drought in 2023. Therefore, the drought-tolerant trait is expected to gain popularity during the forecast period.

- Factors such as the increased demand for improving animal feed and a large number of benefits such as resistance to diseases and increasing yield are expected to drive the market's growth in the region.

North America Forage Seed Industry Overview

The North America Forage Seed Market is fragmented, with the top five companies occupying 37.48%. The major players in this market are Bayer AG, Corteva Agriscience, DLF, KWS SAAT SE & Co. KGaA and Land O'Lakes Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Alfalfa

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Alfalfa

- 5.2.2 Forage Corn

- 5.2.3 Forage Sorghum

- 5.2.4 Other Forage Crops

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Ampac Seed Company

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 DLF

- 6.4.6 Groupe Limagrain

- 6.4.7 KWS SAAT SE & Co. KGaA

- 6.4.8 Land O'Lakes Inc.

- 6.4.9 Royal Barenbrug Group

- 6.4.10 S&W Seed Co.

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms