|

市場調査レポート

商品コード

1693462

欧州の飼料用種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Forage Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の飼料用種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

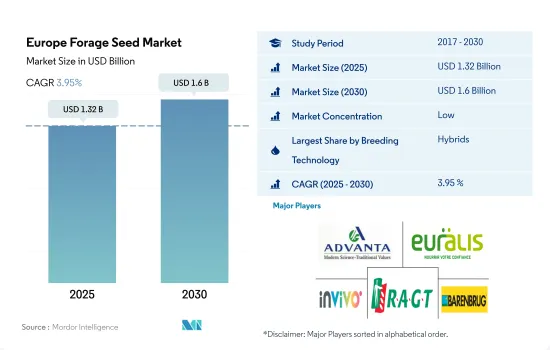

欧州の飼料用種子市場規模は2025年に13億2,000万米ドルと推定・予測され、2030年には16億米ドルに達し、予測期間中(2025~2030年)のCAGRは3.95%で成長すると予測されています。

ハイブリッド飼料用種子は、収量の増加、耐病性、幅広い適応性などの特性により、市場を独占しています。

- 2022年には、ハイブリッド種子が欧州の飼料用種子市場を独占し、市場の約88%を占めました。同年の露地受粉品種は12%でした。ハイブリッド種の高いシェアは、高収量、耐病性、高樹勢、幅広い適応性などの形質と関連しています。この地域では遺伝子組換え作物の栽培が禁止されているため、非遺伝子組換えハイブリッド品種のみが栽培を認められています。

- 2022年には、耕作面積が広くハイブリッド種の採用率が高いため、飼料用トウモロコシがハイブリッド分野で62.9%の主要シェアを占めました。トウモロコシのハイブリッド種子の数量は2022年に2021年比で2.1%増加したが、これは主に大規模な商業用酪農場からの飼料需要の増加によるものです。

- アルファルファは、高い種子交換率と畜産業界からの高い需要により、2022年の欧州ハイブリッド飼料用種子市場で36%のシェア値を占め、予測期間中にハイブリッド種子の販売がさらに増加する可能性があります。

- 欧州は非遺伝子組換えハイブリッド飼料用トウモロコシの最大生産国のひとつであり、2022年の欧州飼料用種子市場におけるシェアは88%に達します。この地域における非遺伝子組み換えハイブリッド飼料用トウモロコシ種子の需要は、その高い栄養価により予測期間中にさらに増加する可能性があります。

- OPVの栽培面積ではドイツが主要国です。同国では自生牧草地が多いため、2022年には欧州の飼料用OPVとハイブリッド誘導体の総面積の33.2%を占めていました。OPVの使用は栽培コストを下げるため、将来的にOPVの使用を後押しする可能性が高いです。

- そのため、ハイブリッドおよびOPV種子品種の両方が、畜産部門からの需要増加により予測期間中に成長すると予想されます。

ドイツは、加工産業からの高い需要と飼料需要の増加により、飼料用種子の販売でリードしています。

- 欧州は飼料作物の重要な生産国のひとつです。2022年には、金額ベースで欧州の種子市場の8.8%、世界の飼料用種子市場の26.7%を占める。この市場を牽引しているのは、動物人口の増加と食肉消費量の増加です。

- 高い飼料品質と収穫期間の短縮に対する需要の高まりに対応するため、企業は生産者の利益のために新しい種子品種を開発してきました。例えば、農家は現在、DKC 3218、DKC 3204、Debalto、Marcamoなどのアルファルファ品種を利用できます。

- 2022年の飼料用種子の市場シェアはフランスが28.6%で欧州で最も高く、次いでドイツが20.4%でした。促進要因としては、飼料製品に対する需要の高まり、畜産製品に対する消費者の需要、畜産人口の増加、放牧用地の縮小などが挙げられます。

- 英国は最も急成長している国のひとつで、畜産農家からの飼料需要が高く、バイオ燃料生産と豚の頭数が増加していることから、予測期間中のCAGRは5.9%と予測されます。

- イタリア、オランダ、ポーランドなどの他の国も飼料作物に対する需要が大きく、これらの国の収穫面積は2017年から2022年にかけて6.8%増加しました。

- 飼料用種子市場を管理する欧州種子協会の規制は、種子サイクル、土壌条件、時間的インセンティブのリターンの予測不可能性を高めるために、飼料用種子生産への投資を増加させるのに役立ちました。したがって、この地域の飼料用種子市場は、予測期間中にCAGR 3.9%を記録すると予測されます。

欧州の飼料用種子市場の動向

家畜用の高品質飼料需要の増加と適切な気候が飼料栽培を促進

- 欧州は、多様な景観と飼料栽培に適した気候を有することから、世界有数の飼料生産国です。この地域の飼料栽培総面積は2022年には910万haに達し、家畜の飼料需要の増加により2017年から2022年の間に4.6%増加しました。例えば、2022年には、有機飼料需要の増加により、欧州の有機飼料生産量は25万トンを超えます。

- 飼料作物の中では、飼料用トウモロコシとアルファルファの栽培面積が最も大きいです。これらは2022年の欧州の飼料栽培面積のそれぞれ63.5%と35.4%を占めているが、これはエネルギー含有量が高く消化が容易なことから、この地域での需要が高いためです。近年、欧州における飼料用ソルガムの栽培面積は、家畜飼料やアルコール、バイオ燃料の生産に対する需要の増加により、絶えず拡大しています。栽培面積が増加しているもう一つの理由は、この地域の一部で干ばつが増加していることです。そのため、農家はソルガム栽培に移行しています。ソルガムにはもともと干ばつ耐性があるからです。組織による取り組みが栽培面積の拡大に役立っています。例えば、フランス全国トウモロコシ・ソルガム種子生産連盟(FNPSMS)とPZPK(ポーランド)は、スペイン、フランス、ドイツ、ブルガリアにおいて、トウモロコシとソルガムの利点とその栽培を推進しています。

- ドイツとフランスは欧州の主要地域を占めており、農地が広く、気候も適していることから、2022年にはこの地域の飼料栽培全体の25.6%と18.6%をそれぞれ占めています。そのため、この地域では家畜飼料の需要が増加しており、農家は需要を満たすために飼料作物の栽培面積を拡大する必要に迫られていると推定されます。

ハイブリッド飼料用種子は、幅広い適応性と早熟形質で人気を集めています。

- アルファルファと飼料用トウモロコシは、欧州全土で広く栽培されている人気の飼料作物です。家畜産業における重要性から、育種技術を通じてアルファルファの収量と品質を向上させるための科学的取り組みが行われています。気候の変化に伴い、作物に最も影響を与える環境要因も変化しています。その結果、地域の条件に適応する、均一性が高く適応性の広いアルファルファ品種への需要が高まり、農家に広く採用されています。

- バイエル、DLF、バレンブルグなどの企業は、アルファルファ(DKC 3218、DKC 3204、Debalto、Marcamo)や飼料用トウモロコシ(Daisy、Fado、Power 4.2)など、多くの品種のアルファルファや飼料用トウモロコシを英国に導入しています。これらの品種は、多様な環境条件に耐え、様々な土壌タイプに適応し、圃場ストレスや暑熱条件に耐える能力を有しています。

- 早生でデンプン含量が高い特性を持つ種子の需要は、急速に伸びると推定されます。これらの品種は生育期間が短いため、農家はより早く収穫することができ、飼料用トウモロコシに含まれる高いデンプン含量は飼料としての栄養価を高める。さらに、EU委員会は農家の要求に応えるため、REFORMA(2016~2020年)という新しいプロジェクトを開始しました。このプロジェクトは、高度な育種技術を開発し、アルファルファやその他の飼料作物の新品種を導入することを目的としています。

- 病害抵抗性、高乾物含量、昆虫抵抗性、長期保存性、耐乾性などの形質を持つ丈夫な品種のアルファルファや飼料用トウモロコシの需要は、予測期間中に大幅に増加し、収量損失を補い、消費要件を満たすために生産性を向上させると予測されます。

欧州の飼料用種子産業の概要

欧州の飼料用種子市場は断片化されており、上位5社で30.24%を占めています。この市場の主要企業は以下の通りです。 Advanta Seeds-UPL, Euralis Semences, InVivo, RAGT Group and Royal Barenbrug Group(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 最も人気のある品種

- アルファルファと飼料用トウモロコシ

- 育種技術

- 畑作物

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非遺伝子組み換え雑種

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 作物

- アルファルファ

- 飼料用トウモロコシ

- 飼料用ソルガム

- その他の飼料作物

- 国名

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- Bayer AG

- DLF

- Euralis Semences

- Groupe Limagrain

- InVivo

- KWS SAAT SE & Co. KGaA

- RAGT Group

- Royal Barenbrug Group

- S&W Seed Co.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92524

The Europe Forage Seed Market size is estimated at 1.32 billion USD in 2025, and is expected to reach 1.6 billion USD by 2030, growing at a CAGR of 3.95% during the forecast period (2025-2030).

Hybrid forage seeds dominated the market due to their traits such as increased yield, disease resistance, and widely adaptable nature

- In 2022, hybrids dominated the European forage seed market and accounted for about 88% of the market. Open-pollinated varieties accounted for 12% in the same year. The high share of hybrids is associated with traits such as high yield, disease resistance, high vigor, and wider adaptability. Only non-transgenic hybrid varieties are approved for cultivation due to the ban on genetically engineered crops in the region.

- In 2022, forage corn held the major share of 62.9% in the hybrids segment due to the large area under cultivation and higher adoption of hybrids. The volume of corn hybrid seeds increased by 2.1% in 2022 compared to 2021, primarily due to increased forage demand from large commercial dairy farms.

- Alfalfa held a share value of 36% in the European hybrid forage seed market in 2022 due to the high seed replacement rate and high demand from the livestock industry, which may further increase the sales of hybrid seeds during the forecast period.

- Europe is one of the largest producers of non-transgenic hybrid forage corn, contributing an 88% share value of the European forage seed market in 2022. The demand for non-transgenic, hybrid forage corn seeds in the region may increase further during the forecast period due to their high nutritional value.

- Germany was the major country in terms of area under OPVs. In 2022, the country had a 33.2% area of the total European forage OPVs and hybrid derivatives due to the prevalence of native pastures in the country. The use of OPVs lowers cultivation costs, which is likely to boost their use in the future.

- Therefore, both hybrid and OPV seed varieties are anticipated to grow during the forecast period due to increased demand from the livestock sector.

Germany is leading in forage seed sales with high demand from the processing industry and increasing demand for animal feed

- Europe is one of the significant producers of forage crops. In 2022, the market accounted for 8.8% of the European seed market and 26.7% of the global forage seed market by value. The market is being driven by the increasing animal population and rising meat consumption.

- To meet the growing demand for high forage quality and shorter harvest time periods, companies have been developing new seed varieties for the benefit of growers. For instance, farmers now have access to alfalfa varieties such as DKC 3218, DKC 3204, Debalto, and Marcamo.

- France had the highest sales of forage seeds in Europe, with a market share of 28.6% in 2022, followed by Germany, with 20.4%. The driving factors include growing demand for feed products, consumer demand for livestock products, an increase in the livestock population, and shrinking land for grazing animals.

- The United Kingdom is one of the fastest-growing countries, with a projected CAGR of 5.9% during the forecast period due to high demand for forage from livestock farmers and the country witnessing an increase in biofuel production and pig population.

- Other countries such as Italy, the Netherlands, and Poland also have a significant demand for forage crops, and the area harvested in these countries increased by 6.8% from 2017 to 2022.

- The European Seed Association's regulation, which governs the forage seed market, helped increase investments in forage seed production to enhance the unpredictability of the seed cycle, soil conditions, and time incentive returns. Therefore, the forage seed market in the region is estimated to register a CAGR of 3.9% during the forecast period.

Europe Forage Seed Market Trends

An increase in the demand for quality feed for livestock and a suitable climate are driving the forage cultivation

- Europe is one of the largest producers of forages in the world, as it has diverse landscapes and a suitable climate for forage cultivation. The total forage cultivation area in the region reached 9.1 million ha in 2022, which increased by 4.6% between 2017 and 2022 due to increasing feed demand from livestock. For instance, in 2022, organic forage production in Europe exceeded more than 250,000 metric ton due to the increasing demand for organic feed.

- Among forage crops, forage corn and alfalfa have the largest area under cultivation. They accounted for 63.5% and 35.4% of the European forage cultivation area in 2022, respectively, due to their high demand in the region driven by their high energy content and easy digestibility. In recent years, the area of forage sorghum in Europe has constantly grown due to its increasing demand for animal feed and the production of alcohol and biofuels. Another reason for the increasing area under cultivation is the rising drought in some parts of the region. Therefore, farmers are shifting to sorghum farming as it has inherent drought tolerance. The initiatives by organizations are helping in the expansion of areas under cultivation. For instance, the French National Federation of Maize and Sorghum Seed Production (FNPSMS) and the PZPK (Poland) are promoting the benefits of maize and sorghum and their cultivation in Spain, France, Germany, and Bulgaria.

- Germany and France held the major areas in Europe, and they accounted for 25.6% and 18.6% of the overall forage cultivation in the region in 2022, respectively, due to their significant agricultural land and suitable climate. Therefore, the growing demand for animal feed in the region is estimated to put pressure on farmers to expand the area under forage crops to meet the demand.

Hybrid forage seeds are gaining traction with wider adaptability and early matured traits

- Alfalfa and forage corn are popular forage crops extensively cultivated across Europe. Due to their significance in the livestock industry, scientific efforts are being made to enhance the yield and quality of alfalfa through breeding techniques. As the climate changes, so do the environmental factors that impact crops the most. Consequently, demand for high uniformity and wider adaptability alfalfa cultivars that adapt to regional conditions has increased and are widely employed by farmers.

- Companies such as Bayer, DLF, and Barenbrug have introduced many varieties of alfalfa and forage corn in the United Kingdom, such as Alfalfa (DKC 3218, DKC 3204, Debalto, and Marcamo), as well as forage corn (Daisy, Fado, and Power 4.2). These varieties possess the ability to withstand diverse environmental conditions, adapt to various soil types, and withstand field stress and heat conditions.

- The demand for seeds with early maturity and high starch content characteristics is estimated to grow rapidly. These varieties offer a shorter growing period, allowing farmers to harvest sooner, and the high starch content in forage corn enhances its nutritional value for animal feed. Moreover, the EU Commission initiated a new project called REFORMA (2016-2020) to address farmers' requirements. This project aims to develop advanced breeding techniques and introduce new cultivars of alfalfa and other forage crops.

- The demand for robust varieties of alfalfa and forage corn with traits such as disease resistance, high dry matter content, insect resistance, long shelf life, and drought tolerance is projected to increase significantly during the forecast period to compensate for yield losses and increase productivity to meet consumption requirements.

Europe Forage Seed Industry Overview

The Europe Forage Seed Market is fragmented, with the top five companies occupying 30.24%. The major players in this market are Advanta Seeds - UPL, Euralis Semences, InVivo, RAGT Group and Royal Barenbrug Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Alfalfa & Forage Corn

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Alfalfa

- 5.2.2 Forage Corn

- 5.2.3 Forage Sorghum

- 5.2.4 Other Forage Crops

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Poland

- 5.3.6 Romania

- 5.3.7 Russia

- 5.3.8 Spain

- 5.3.9 Turkey

- 5.3.10 Ukraine

- 5.3.11 United Kingdom

- 5.3.12 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Bayer AG

- 6.4.3 DLF

- 6.4.4 Euralis Semences

- 6.4.5 Groupe Limagrain

- 6.4.6 InVivo

- 6.4.7 KWS SAAT SE & Co. KGaA

- 6.4.8 RAGT Group

- 6.4.9 Royal Barenbrug Group

- 6.4.10 S&W Seed Co.

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms