|

市場調査レポート

商品コード

1693461

欧州の穀物種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Grain Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の穀物種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 249 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

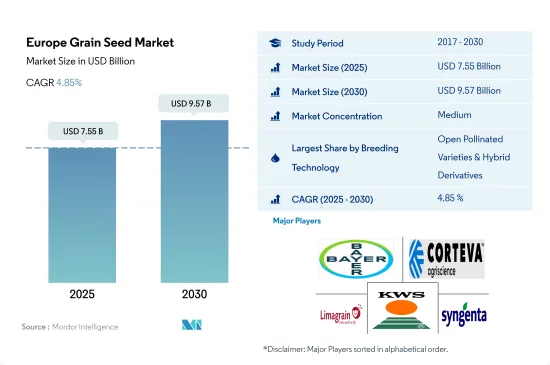

欧州の穀物種子市場規模は2025年に75億5,000万米ドルと推定・予測され、2030年には95億7,000万米ドルに達し、予測期間(2025~2030年)のCAGRは4.85%で成長すると予測されています。

OPVは病害虫に強いため使用量が増加

- 欧州では、露地受粉種子が数量でも金額でも市場を独占しています。非遺伝子組み換え雑種は2022年の穀物種子市場全体の33.8%を占めました。非遺伝子組み換えハイブリッドのシェアは、穀物の作付面積の拡大、有機農産物への需要の高まり、一人当たりの消費量の増加により、2017年から2022年の間に16.3%増加しました。

- 有機農業と慣行農業の栽培面積の増加は、非遺伝子組み換えハイブリッドの成長を促進する主な要因です。例えば、欧州における穀物の有機栽培面積は、2017年から2021年の間に24.4%増加しました。2021年の有機栽培面積は1,780万ヘクタールでした。

- 2022年には、昆虫抵抗性は遺伝子組み換えハイブリッドで栽培される唯一の形質であり、ハイブリッド種子市場額の1.5%に寄与しました。欧州で耐虫性作物(トウモロコシ)を栽培している主な国はスペインとルーマニアです。

- トウモロコシは、欧州で遺伝子組み換え種子による栽培が承認されている唯一の作物です。遺伝子組換え耐虫性トウモロコシの市場価値は2017年から2022年の間に26.1%増加しました。

- 2022年に欧州で開放受粉品種とハイブリッド派生品種を使用して栽培された主要作物は、小麦とその他の穀物・穀類でした。これらは欧州のOPV種子市場全体の56.5%と38.4%を占めています。

- この地域では、家畜飼料としてのGM作物によって補われている畜産物の需要が増加しているため、商業用種子の使用量は増加すると推定されます。したがって、新たな害虫の出現に伴い、昆虫抵抗性遺伝子組み換えハイブリッド種子市場は予測期間中に同国で成長すると予測されます。

- したがって、有機食品に対する需要の高まりと新たな害虫や昆虫が、この地域で最も速い速度でハイブリッド種子市場を牽引すると推定されます。

フランスは穀物種子市場を独占し、トウモロコシは同国で栽培されている主要作物です。

- 欧州では、穀物種子分野が種子市場全体に大きく貢献しています。2022年には金額ベースで欧州種子市場の55.4%を占めました。この地域はトウモロコシ種子市場で大きなシェアを占めており、2022年には世界のトウモロコシ種子市場の8.7%を占めました。

- フランスはトウモロコシの主要生産国です。とうもろこしはフランス全土で栽培されており、フランス南部地域がその大部分を生産しています。アキテーヌ地方は国内のトウモロコシ生産全体の21%を占め、フランスのミディピレネー州は2022年に13%を占める。この作物は国内で4月から5月の間に植えられ、9月から11月の間に収穫されます。フランスは欧州におけるソルガムきびの主要生産国および輸出国でもあり、2022年には欧州のソルガムきび種子市場の28.7%を占めています。欧州で取引されるソルガムきびの大部分は地元産です。

- イタリアは欧州の主要なコメ生産国です。同国のコメ種子市場は、2022年の欧州コメ種子市場の34.9%を占める。北部のピエモンテ州、ロンバルディア州、ヴェネト州では水が豊富で、湿潤な場所でも稲作が可能なため、ほとんどの稲作が行われています。イタリアの米の品種はほとんどがジャポニカ種で、残りはインディカ種です。

- 欧州における小麦の主要生産国はドイツとフランスであり、2022年の欧州小麦種子市場の52.3%を占めています。小麦の輸出需要は増加傾向にあり、同地域の小麦需要の増加が見込まれます。

- 輸出需要の増加、消費需要の増加、穀物・穀類の栽培面積の増加などの要因が、同地域の種子市場の成長を促進すると予想されます。

欧州の穀物種子市場動向

加工産業からの需要増加と穀物価格の上昇が作物栽培面積の増加を促進

- 欧州では穀物・穀類が主要な作物栽培面積を占めています。2022年の穀物・穀類の栽培面積は1億3,404万haで、主食としての穀物に対する旺盛な需要と生産価格の上昇により前年比1.6%増加しました。トルコ、イタリア、ロシア、フランス、ドイツなどの主要穀物・穀類生産国では、2017年と2018年に作付面積が減少しました。減少の主な理由は、予期せぬ大雨、雹害、作付けシーズン前の降水量の増加、油糧種子へのシフトなどです。

- 欧州では、ロシアが穀物・穀類の栽培面積で主要国であり、2022年の栽培面積の32.8%を占めました。作付面積が多いのは、黒海との貿易上の優位性と、トウモロコシや小麦などの主要穀物の栽培に適した気候条件のためです。しかし、2021年の作付面積は、同国の大麦と小麦の作付面積に影響を与えたアイスクラスト現象により、2020年に比べ3%減少しました。

- ウクライナとトルコも穀物・穀類の主要栽培国で、2022年の作付面積はそれぞれ全体の12.04%と8.3%を占めました。ウクライナは、近隣欧州諸国への小麦とトウモロコシの主要輸出国のひとつです。ウクライナでは、2022年に小麦が730万ヘクタール、トウモロコシが580万ヘクタールで、穀物・穀類部門の80.7%を占めています。

- 従って、人間消費用需要の増加、バイオ燃料用混合産業、輸出市場からの有利な市場価格により、予測期間中に穀物・穀類の栽培面積は増加すると予想されます。

気候要因と病害管理が、この地域における小麦とトウモロコシのハイブリッド品種の採用を促進している

- ここ数年、欧州の大部分では小麦とトウモロコシの収量が減少しています。この減少は主に、国にもよるが、過去5年から15年の間に多くの国々で気候の不確実性と変動性がこれらの作物に与えた影響によるものです。さらに、ストレスの多い環境条件や、病気や害虫などの生物学的ストレスが、作物に大きな被害をもたらしています。例えば、病害の重症度が高い感受性遺伝子型は、穀物収量の30%以上を損失しています。そのため、生産者はこうした損失を最小限に抑えるため、抵抗性品種へとシフトしています。

- Syngenta、Groupe Limagrain、KWS SAATのような企業は、SY Insitor、Graham、LG Typhoon、LG Princeのような病害虫抵抗性小麦品種を提供し、セプトリア、さび病、OWBM(オレンジコムギハモグリバエ)などのような病害による収量ロスに対処しています。さらに2021年には、バイエルとRAGT Semencesが共同で、最新の育種手法、高性能種子製品システム、高度なデジタルソリューションを用いてハイブリッド小麦種子を開発しました。

- 欧州の農家の間では、宿根に強いトウモロコシ品種への需要が高まっています。これらの品種は悪天候に耐え、宿根による作物の損失を減らすことができます。コルテバ・アグリスサイエンスは、P7179やP7326のような、強風時の立性改善品種を提供しています。

- 気候条件の変化や高収量生産への需要の高まりを受け、早生、高でんぷん・乾物含量、耐病性形質を持つトウモロコシ品種は、予測期間中により多くの支持を集めると予測されます。

欧州の穀物種子産業の概要

欧州の穀物種子市場は適度に統合されており、上位5社で47.93%を占めています。この市場の主要企業は以下の通り。 Bayer AG, Corteva Agriscience, Groupe Limagrain, KWS SAAT SE & Co. KGaA and Syngenta Group(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 最も人気のある形質

- 小麦とトウモロコシ

- 育種技術

- 列作物

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非遺伝子組み換え雑種

- 遺伝子組み換え雑種

- 昆虫抵抗性ハイブリッド

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 作物

- トウモロコシ

- 米

- ソルガム

- 小麦

- その他の穀物

- 生産国

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- BASF SE

- Bayer AG

- Corteva Agriscience

- Florimond Desprez

- Groupe Limagrain

- InVivo

- KWS SAAT SE & Co. KGaA

- RAGT Group

- Syngenta Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92523

The Europe Grain Seed Market size is estimated at 7.55 billion USD in 2025, and is expected to reach 9.57 billion USD by 2030, growing at a CAGR of 4.85% during the forecast period (2025-2030).

OPVs witness increased usage because they offer resistance to pests and diseases

- In Europe, the open-pollinated seed segment dominated the market in terms of volume and value. Non-transgenic hybrids accounted for 33.8% of the total grain seed market value in 2022. The non-transgenic hybrids' share increased by 16.3% between 2017 and 2022 due to the expansion of planting area under grains, rising demand for organic produce, and rising per capita consumption.

- An increase in area under organic farming and conventional farming are major factors driving the growth of non-transgenic hybrids. For instance, the organic farming area under cereals in Europe increased by 24.4% between 2017 and 2021. The organic area under farming was 17.8 million hectares in 2021.

- In 2022, insect resistance was the only trait grown under transgenic hybrids, and it contributed to 1.5% of the hybrid seed market value. Major countries growing insect-resistant crops (corn) in Europe are Spain and Romania.

- Corn is the only crop approved for cultivation using transgenic seeds in Europe. The market value of transgenic insect-resistant corn increased by 26.1% between 2017 and 2022.

- Wheat and other grains and cereals were the major crops grown in Europe using open-pollinated varieties and hybrid derivatives in 2022. They accounted for 56.5% and 38.4% of the total OPV seeds market value in Europe.

- The usage of commercial seeds is estimated to increase as the demand for livestock products, compensated by GM crops as animal feed, has been increasing in the region. Thus, with the emergence of new insect pests, the insect-resistant transgenic hybrid seed market is projected to grow in the country during the forecast period.

- Therefore, rising demand for organic food and emerging pests and insects are estimated to drive the hybrid seed market at the fastest rate in the region.

France dominated the grain seed market with corn being the major crop growing in the country

- In Europe, the grain seed segment was the major contributor to the overall seed market. It accounted for 55.4% of the European seed market in terms of value in 2022. The region had a major share of the corn seed market, which accounted for 8.7% of the global corn seed market in 2022.

- France is the leading producer of corn. Corn is grown across France, with the country's southern region producing the majority of the crop. The Aquitaine region accounted for 21% of overall corn production in the country, while the French state of Midi-Pyrenees accounted for 13% in 2022. The crop is planted in the country between April and May and harvested between September and November. France is also a primary producer and exporter of sorghum in Europe, and it accounted for 28.7% of the European sorghum seed market in 2022. The majority of sorghum traded in Europe comes from local sources.

- Italy is the major rice producer in Europe. The rice seed market in the country accounted for 34.9% of the European rice seed market in 2022. Most rice production is done in the northern Piemonte, Lombardia, and Veneto regions since water is abundant there, and the rice crop can be grown in wet places. Most rice varieties in Italy are Japonica, with the rest having Indica.

- Germany and France were the major producers of wheat in Europe, which together accounted for 52.3% of the European wheat seed market in 2022. The export demand for wheat is moving in an upward trend, which is anticipated to increase the demand for wheat in the region.

- Factors such as higher export demand, increase in the consumption demand, and increased area under cultivation of grains and cereals are expected to drive the seed market growth in the region.

Europe Grain Seed Market Trends

Increased demand from processing industries and increasing prices of cereals are driving the area under crop cultivation

- Grains and cereals occupied the major area under cultivation of crops in Europe. The area under cultivation of the grains and cereals in 2022 accounted for 134.04 million ha, which increased by 1.6% from the previous year due to strong demand for cereals as a staple food and an increase in output prices. The acreage declined in 2017 and 2018 in major grains and cereals-producing countries such as Turkey, Italy, Russia, France, and Germany. The major reasons for the decline include unexpected heavy rainfall, hail damage, higher precipitation prior to planting season, and shifting toward oilseeds.

- In Europe, Russia was the major country in terms of acreage under grains and cereals, which accounted for 32.8% of the acreage in 2022. The higher acreage was because of the trade advantage with the Black Sea and favorable climatic conditions for cultivating primary cereals such as corn and wheat. However, the acreage declined in 2021 by 3% compared to 2020 due to the ice crusting event affecting barley and wheat crop acreage in the country.

- Ukraine and Turkey are also the major cultivating countries of grains and cereals, which accounted for 12.04% and 8.3% of the overall acreage in 2022, respectively. Ukraine was one of the major exporters of wheat and corn to neighboring European countries. In Ukraine, wheat and corn accounted for 7.3 million hectares and 5.8 million hectares in 2022, respectively, which together accounted for 80.7% of the area under the grains and cereals segment in the country.

- Therefore, increasing demand for human consumption, blending industries for biofuel, and favorable market prices from export markets are anticipated to increase the area under grains and cereals during the forecast period.

Climatic factors and disease management are driving the adoption of hybrid varieties of wheat and corn in the region

- In the last few years, large parts of Europe have witnessed a decline in the yield performance of wheat and corn. The decline is primarily attributed to the impact of climate uncertainties and variability on these crops in many countries over the last 5 to 15 years, depending on the country. Moreover, stressful environmental conditions and biotic stresses, such as diseases and pests, have led to considerable damage to crops. For instance, susceptible genotypes with high disease severity have resulted in more than 30% of grain yield losses. Therefore, growers are shifting toward resistant varieties to minimize these losses.

- Companies such as Syngenta, Groupe Limagrain, and KWS SAAT are offering disease and pest-resistant wheat varieties such as SY Insitor, Graham, LG Typhoon, and LG Prince to address yield losses caused by diseases like Septoria, rusts, OWBM (orange wheat blossom midge), and others, in field conditions. Additionally, in 2021, Bayer and RAGT Semences collaborated to develop hybrid wheat seeds using the latest breeding methodologies, high-performing seed product systems, and advanced digital solutions.

- The demand for corn varieties that are resistant to lodging has increased among European farmers. These varieties can endure adverse weather conditions and reduce crop losses caused by lodging. Corteva Agriscience offers varieties like P7179 and P7326, which have improved standability during strong winds.

- Corn cultivars with early matured, high starch and dry matter content, and disease-resistant traits are projected to gain more traction during the forecast period, subjected to the changing climatic conditions and the increasing demand for high-yield production.

Europe Grain Seed Industry Overview

The Europe Grain Seed Market is moderately consolidated, with the top five companies occupying 47.93%. The major players in this market are Bayer AG, Corteva Agriscience, Groupe Limagrain, KWS SAAT SE & Co. KGaA and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Wheat & Corn

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Insect Resistant Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Corn

- 5.2.2 Rice

- 5.2.3 Sorghum

- 5.2.4 Wheat

- 5.2.5 Other Grains & Cereals

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Poland

- 5.3.6 Romania

- 5.3.7 Russia

- 5.3.8 Spain

- 5.3.9 Turkey

- 5.3.10 Ukraine

- 5.3.11 United Kingdom

- 5.3.12 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Florimond Desprez

- 6.4.6 Groupe Limagrain

- 6.4.7 InVivo

- 6.4.8 KWS SAAT SE & Co. KGaA

- 6.4.9 RAGT Group

- 6.4.10 Syngenta Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms