|

市場調査レポート

商品コード

1693465

アジア太平洋地域の穀物種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia-Pacific Grain Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の穀物種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 267 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

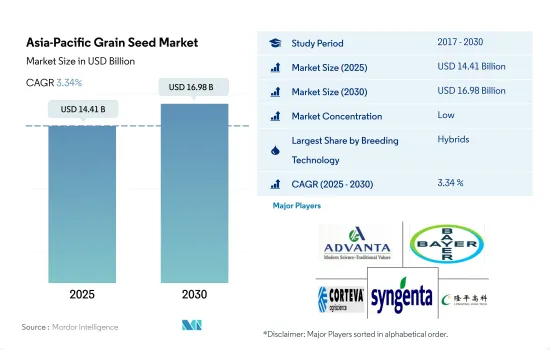

アジア太平洋地域の穀物種子市場規模は2025年に144億1,000万米ドルと推定され、2030年には169億8,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは3.34%で成長すると予測されます。

ハイブリッド種子は高収量と生物的・生物的ストレスに対する高い抵抗性により、穀物種子市場を独占しています。

- アジア太平洋地域では、ハイブリッド種子が穀物種子市場を独占しており、2022年のシェアは66.4%でした。これは主に、ハイブリッド種子の高い収量、改良された形質、生物・生物ストレスに対する高い耐性によるものです。

- この地域のハイブリッド種子市場では、穀物が金額ベースで2022年に58.2%の主要シェアを占めました。これは主に、穀物の栽培面積が大きく、植え付けに必要な種子の量が多いためです。穀物種子のシェアは、特にトウモロコシとコメにおいてハイブリッド種子の採用が増加していることから、予測期間中に増加すると予想されます。

- ハイブリッド種子では、非遺伝子組み換え種子分野が予測期間中最も急成長し、CAGR 3.1%を記録すると予測されます。これは、すべての作物で遺伝子組み換えハイブリッド種子が利用できないこと、インド、オーストラリア、パキスタンを含む多くの主要農業国で政府が遺伝子組み換え穀物作物の栽培を禁止していることによる。

- 開放受粉品種とハイブリッド派生品種は、2022年の穀物種子市場額の33.6%を占めました。開放受粉品種は自家受粉の特性から穀物作物では一般的であるが、ハイブリッド種の生産は比較的困難です。

- アジア太平洋地域では、穀物作物の中でコメが開放受粉品種の種子市場価値を支配しています。2022年の市場シェアはコメが58.1%、次いでトウモロコシ(15.3%)、小麦(14.1%)、その他の穀物・穀類(10.2%)、ソルガム(2.2%)となっています。

- ハイブリッド種子に対する需要の増加、高収量の可能性、栽培の増加が、予測期間中に市場を牽引すると予想される要因です。

ハイブリッド品種の開発と消費需要の高まりにより、穀物・穀類の栽培面積が増加しています。

- アジア太平洋地域では、中国が最大の穀物種子市場であり、2022年には金額ベースで62%を占め、市場規模は80億米ドルでした。中国は世界市場における穀物生産をリードしており、2021年の生産量は6億3,300万トンで、同年の世界の穀物生産の20.6%を占めました。2021年の穀物生産量では、トウモロコシが42.2%を占めています。トウモロコシ生産はエタノール生産に利用されています。

- 2022年、トウモロコシは穀類・穀物種子市場の約52.6%の主要シェアを占めました。家畜人口の増加と食肉需要の増加に伴い、トウモロコシ生産の大部分は家畜の飼料として使用されています。

- インドは最大の穀物生産国であり、世界最大の穀物製品輸出国でもあります。コメ(バスマティ種と非バスマティ種を含む)はインドの穀類総輸出量の87%以上を占め、2021~2022年の間に主要なシェアを占める。小麦を含むその他の穀類は、2021-2022年のインドからの穀類総輸出に占める割合はわずか12%です。作物の輸出ポテンシャルの向上により、種子の需要が増加すると推定されます。

- インドネシアの国内および世界の企業は、ここ数年でハイブリッド種子の導入に力を入れるようになり、市場収益を大幅に押し上げています。例えば、2021年、バイエル・インドネシアは、収量の増加と細菌性葉枯病(BLB)からの保護を同時に実現した画期的なハイブリッド稲種子であるArize(R)H 6444 Goldを発表しました。

- 穀物の消費と需要が増加し、輸入への依存が最小限になったことで、植林面積が拡大しており、予測期間中に穀物種子分野の成長を促進すると予想されます。

アジア太平洋地域の穀物種子市場動向

主食消費としての穀物・穀類の需要と、栽培に適した気候により、穀物・穀類はこの地域で最大のセグメントとなっています。

- 穀物と穀類は、その一部が主食であることから、この地域で栽培されている主要作物です。これらの作物の栽培面積は、2022年には同地域の連作作物総栽培面積の80.8%を占める。恵まれた気候条件、主食としての高い消費需要、飼料産業からのトウモロコシ需要、輸出の可能性が、この地域の農家がより多くの穀物を栽培する原動力となっています。2022年の穀物・穀類の栽培面積は6億7,650万ヘクタールで、2017年から1.6%増加しました。穀物・穀類の中でも米は、アジア太平洋地域が世界の主要生産地であることから、この地域で栽培されている主要な主食作物です。2022年の米栽培面積は1億4,320万ヘクタールで、2017年の1億3,800万ヘクタールから増加しました。夏期とモンスーン期の豊富な降雨量は、この地域の米栽培に理想的な条件を提供しています。

- 小麦もまた、この地域で栽培されている主要な穀物作物です。2022年のアジア太平洋地域の小麦栽培面積は9,750万ヘクタールで、2017年から1.5%増加しました。同地域ではインドと中国が主要な栽培面積を占めており、2022年にはそれぞれ310万ヘクタールと2,380万ヘクタールとなります。さらに、トウモロコシの栽培面積は2022年に6,760万ヘクタールとなり、穀物作物全体の10.0%を占める。トウモロコシの栽培面積を押し上げている要因は、高い収量を生産できることと、加工・飼料産業からの需要が大きいことです。

- この地域の他の主要穀物作物はソルガムと大麦です。大麦の主要生産国はオーストラリアです。大麦の栽培面積は2017年から2022年にかけて23%増加し、ビールの醸造や蒸留に使用され、高品質でクリーンな動物飼料として、世界的にオーストラリア産大麦の需要が増加しています。

干ばつ耐性と耐病性が、この地域の市場成長拡大に寄与する主な形質です。

- トウモロコシは高収益であるため、生産者が栽培する重要な作物です。生産者は、雑草防除、穀物品質の向上、早熟、宿根耐性、葉巻病や初期腐敗に対する抵抗性、異なる地域や気候条件への幅広い適応性などの形質に対して高い要求を持っています。例えば、BASF SEやシンジェンタなどの企業は、早腐れ病や葉の病気などの病気に対する抵抗性を高め、生産性を高めるのに役立つ形質を提供しています。これらの種子品種は、病害に抵抗するための他の散布剤や代替品が存在しないため、高い需要を目の当たりにしています。さらに、色、高さ、穂当たりの粒数といった他の主要な形質も、生産者にとって高収益をもたらすものとして人気があります。

- 中国とインドは世界的に主要なコメ生産国であり、苗立枯病、穀粒腐敗病、その他の細菌性病害などの病害に耐性のある種子に対する需要が高いです。例えば、Bayer AGのArize Tej Goldのようなブランドは苗立枯病に対する耐性を持ち、Vina SeedのThein Uu8品種はいもち病や鞘枯病のような様々な病気に対する耐性を持っています。さらに、この作物はTryporyza incertulasやGundhi bugsといった様々な害虫の影響を受ける。

- 干ばつ耐性形質は、種子企業によって生産される主要形質のひとつです。気候条件の変化が、生産者によるこの種子品種への高い需要につながっているからです。例えば、2022年、中国は通常の降雨条件よりも乾燥した条件に見舞われ、これは干ばつ耐性種子品種の需要を増加させるのに役立つと予想されます。

- 気候条件による水不足、害虫、作物の成長に影響を与える病気などの要因は、予測期間中に新しい種子品種の導入に役立つと予想されます。

アジア太平洋地域の穀物種子産業の概要

アジア太平洋地域の穀物種子市場は断片化されており、上位5社で19.76%を占めています。この市場の主要企業は以下の通り。 Advanta Seeds-UPL, Bayer AG, Corteva Agriscience, Syngenta Group and Yuan Longping High-Tech Agriculture(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 最も人気のある品種

- コメとトウモロコシ

- 育種技術

- 畑作物

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非遺伝子組み換え雑種

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- 昆虫抵抗性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 作物

- トウモロコシ

- 米

- ソルガム

- 小麦

- その他の穀物

- 生産国

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- Bayer AG

- Corteva Agriscience

- DCM Shriram Ltd(Bioseed)

- Groupe Limagrain

- Jiangsu Zhongjiang Seed Industry Co. Ltd

- Kaveri Seeds

- KWS SAAT SE & Co. KGaA

- Syngenta Group

- Yuan Longping High-Tech Agriculture Co. Ltd

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

The Asia-Pacific Grain Seed Market size is estimated at 14.41 billion USD in 2025, and is expected to reach 16.98 billion USD by 2030, growing at a CAGR of 3.34% during the forecast period (2025-2030).

The hybrid segment dominates the grain seed market due to high yield and a high degree of resistance to the biotic and abiotic stresses

- In Asia-Pacific, hybrid seeds dominate the grain seed market, with a share of 66.4% in 2022. This was mainly due to the higher yield, improved traits, and a high degree of resistance to the biotic and abiotic stresses of hybrid seeds.

- In the hybrid seed market of the region, grains held a major share of 58.2% in 2022 in terms of value. This was mainly due to the large area under grain cultivation and the large volume of seeds required for planting. The share value of grain seeds is expected to increase during the forecast period owing to the rising adoption of hybrids, especially in corn and rice.

- In hybrid seeds, the non-transgenic seed segment is estimated to be the fastest-growing segment during the forecast period, registering a CAGR of 3.1% due to the non-availability of transgenic hybrids for all the crops and the government ban on the cultivation of transgenic grain crops in many major agricultural countries including India, Australia, and Pakistan.

- Open-pollinated varieties and hybrid derivatives held 33.6% of the grain seed market value in 2022. Open-pollinated varieties are more common in grain crops due to their self-pollination characteristics, whereas the production of hybrids is comparatively difficult.

- In Asia-Pacific, among grain crops, rice dominates the open-pollinated variety's seed market value. Rice accounted for a 58.1% share of the market, followed by corn (15.3%), wheat (14.1%), other grains and cereals (10.2%), and sorghum (2.2%) in 2022.

- The increasing demand for hybrid seeds, their high-yielding potential, and the increasing cultivation are the factors anticipated to drive the market during the forecast period.

The development of hybrid varieties and higher consumption demand are increasing the area under cultivation of cereals and grains

- In Asia-Pacific, China has the largest grain seed market, and it accounted for 62% in terms of value in 2022, with a market value of USD 8.0 billion. China led the cereal production in the global market, with a volume of 633 million metric ton in 2021, and it accounted for 20.6% of the global cereal production in the same year. In 2021, corn had a major share of 42.2% of cereal production. The corn production is being used for ethanol production.

- In 2022, corn held the major share of around 52.6% of cereals and grains seed market. The majority of corn production was used in livestock feeding, with the increased livestock population and rising meat demand.

- India is the largest producer of cereal and also the largest exporter of cereal products globally. Rice (including Basmati and Non-Basmati) occupies the major share in India's total cereals export, with more than 87% during the 2021-2022 period. Other cereals, including wheat, accounted for only a 12% share of the total cereals exported from India during 2021-2022. An increase in the export potential of the crops is estimated to increase the demand for the seeds.

- Domestic and global players in Indonesia have increased their focus on the introduction of hybrid seeds over the past few years, which has significantly boosted market revenues. For instance, in 2021, Bayer Indonesia introduced Arize(R) H 6444 Gold, a revolutionary hybrid rice seed that simultaneously increased yields and protects against Bacterial Leaf Blight (BLB).

- With the increased consumption and demand for grains and the minimum dependency on imports, the plantation area is expanding, which is anticipated to fuel the growth of the grains seed segment during the forecast period.

Asia-Pacific Grain Seed Market Trends

The demand for grains and cereals as staple food consumption and the ideal climate for cultivation has made them the largest segment in the region

- Grains and cereals are the major crops cultivated in the region, as some of them are staple foods. The area under cultivation for these crops accounted for 80.8% of the total row crops area in the region in 2022. Favorable climatic conditions, higher consumption demand as a staple food, corn demand from the feed industries, and export potential drive farmers to grow more grains in the region. The area under grains and cereals accounted for 676.5 million hectares in 2022, which increased by 1.6% since 2017. Among the grains and cereals, rice is the major staple food crop cultivated in the region, as Asia-Pacific is the major global producer. In 2022, the area under rice cultivation was 143.2 million hectares, which increased from 138.0 million hectares in 2017. Abundant rainfall during the summer and monsoon seasons provides ideal conditions for rice growing in the region.

- Wheat is another major grain crop cultivated in the region. In 2022, Asia-Pacific wheat acreages accounted for 97.5 million hectares, an increase of 1.5% from 2017. India and China occupy the major cultivated areas in the region, with 3.1 million ha and 23.8 million hectares in 2022, respectively. Moreover, the acreage under corn cultivation was 67.6 million hectares in 2022, representing 10.0% of the total grain crop area. Factors driving the corn in terms of acreage are its ability to produce higher yields and greater demand from the processing and feed industries.

- Other major grain crops in the region are sorghum and barley. Australia is the major producer of barley. The area under barley cultivation increased by 23% from 2017 to 2022, increasing the demand for Australian barley globally for use in beer brewing and distilling and as a high-quality, clean animal feed.

Drought tolerant and disease resistance are the major traits helping in increasing the market growth in the region

- Corn is an important crop cultivated by growers because it is high-profiting. The growers have a high demand for traits such as weed control, improved grain quality, early maturity, lodging tolerance, resistance to leaf curl and early rots, and broader adaptability to different regions and climate conditions. For instance, companies such as BASF SE and Syngenta provide traits that help increase resistance to diseases such as early rots and leaf diseases and higher productivity. These seed varieties are witnessing high demand because no other sprays or alternatives exist to resist the diseases. Furthermore, the other major traits, such as color, height, and the number of grains per cob, are popular for high returns for growers.

- China and India are major rice producers globally and have a high demand for seeds resistant to diseases such as seedling blight, grain rot, and other bacterial diseases. For instance, brands such as Bayer AG's Arize Tej Gold provide resistance to seeding blight, and Vina Seed's Thein Uu8 variety provides resistance to different diseases such as blast and sheath blight. Furthermore, the crop is affected by different pests such as Tryporyza incertulas and Gundhi bugs.

- Drought tolerant trait is one of the major produced traits by seed companies as there have been changes in the climatic conditions which has led to high demand for this seed variety by the growers. For instance, in 2022, China suffered drier conditions than normal rainfall conditions, which is expected to help in increasing the demand for drought-tolerant seed varieties.

- Factors such as low water due to climatic conditions, pests, and diseases affecting the growth of crops are expected to help introduce new seed varieties during the forecast period.

Asia-Pacific Grain Seed Industry Overview

The Asia-Pacific Grain Seed Market is fragmented, with the top five companies occupying 19.76%. The major players in this market are Advanta Seeds - UPL, Bayer AG, Corteva Agriscience, Syngenta Group and Yuan Longping High-Tech Agriculture Co. Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Rice & Corn

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.1.2.3 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Corn

- 5.2.2 Rice

- 5.2.3 Sorghum

- 5.2.4 Wheat

- 5.2.5 Other Grains & Cereals

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 Bangladesh

- 5.3.3 China

- 5.3.4 India

- 5.3.5 Indonesia

- 5.3.6 Japan

- 5.3.7 Myanmar

- 5.3.8 Pakistan

- 5.3.9 Philippines

- 5.3.10 Thailand

- 5.3.11 Vietnam

- 5.3.12 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 DCM Shriram Ltd (Bioseed)

- 6.4.5 Groupe Limagrain

- 6.4.6 Jiangsu Zhongjiang Seed Industry Co. Ltd

- 6.4.7 Kaveri Seeds

- 6.4.8 KWS SAAT SE & Co. KGaA

- 6.4.9 Syngenta Group

- 6.4.10 Yuan Longping High-Tech Agriculture Co. Ltd

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms