|

市場調査レポート

商品コード

1693475

アフリカの穀物種子:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Africa Grain Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカの穀物種子:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

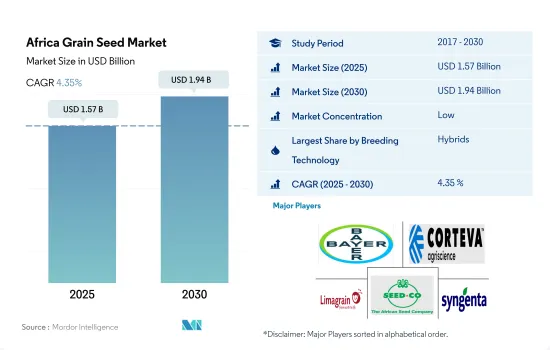

アフリカの穀物種子市場規模は2025年に15億7,000万米ドルと推定・予測され、2030年には19億4,000万米ドルに達し、予測期間(2025~2030年)のCAGRは4.35%で成長すると予測されます。

遺伝子組み換え種子の承認と高収量ハイブリッド種子の需要増加が市場成長を牽引すると推定される

- ハイブリッド品種が市場を独占し、2022年には59.4%のシェアを占めたのに対し、開放受粉品種は40.6%のシェアを占めました。これは主に、作物の収量と生産性を向上させるためにハイブリッド品種の利用が増加したためと考えられます。

- 2022年には、コメと小麦が引き続き、アフリカで露地受粉品種とハイブリッド派生品種を使用して栽培されている2つの主要作物であり、アフリカにおけるそれぞれの市場の98.6%と98.4%を占めています。耐病性で高収量の露地受粉品種の研究開発が活発化していることが、市場成長の原動力になると予想されます。

- ハイブリッドセグメントでは、2022年の同地域の穀物・穀類市場の60.4%を非トランスジェニックハイブリッド種子が、39.6%をトランスジェニック種子が占めています。

- 遺伝子組み換え作物の使用を承認しているのは、47カ国のうち南アフリカ、ブルキナファソ、スーダン、エジプト、ナイジェリアの5カ国のみです。遺伝子組み換え作物は、アフリカの近代農業に徐々に溶け込みつつあります。アフリカでは、昆虫抵抗性の遺伝子組み換えハイブリッドが金額ベースで遺伝子組み換え種子市場の78.2%を占め、除草剤耐性のハイブリッドは2022年に21.8%を占めました。南アフリカは、耐虫性と除草剤耐性形質においてアフリカの穀物種子市場を独占しています。除草剤耐性品種が承認されたのは南アフリカだけです。

- トウモロコシは、アフリカで栽培されている穀物作物で除草剤耐性形質を持つ唯一の作物です。除草剤耐性遺伝子組み換え穀物の市場規模は、予測期間中にCAGR 2.4%を記録すると推定されます。

- 遺伝子組み換え種子の承認と高収量ハイブリッドの需要増加が市場の成長を促進すると予想されます。

南アフリカは穀物栽培面積が大きいためアフリカ最大の穀物種子市場

- 2022年、穀物・穀類はアフリカの連作作物種子市場の約62.6%を占めました。穀物の市場シェアが高い主要理由は、消費量の増加と耕作面積の増加です。

- 南アフリカはアフリカの穀物種子市場の主要シェアを占めており、2022年には市場の約34.6%を占めます。これは、新しく改良された種子品種の入手可能性、市場へのアクセス、トウモロコシのような収益性の高い作物の栽培増加によるものです。南アフリカの市場シェアは予測期間中に拡大すると予測されます。

- ケニアとガーナは穀物種子市場の急成長国で、予測期間中にCAGR 6.6%を記録すると予測されます。米は主要な穀物作物であり、これらの国では需要が高いです。

- トウモロコシはアフリカの穀物種子市場で最大のシェアを占め、2022年には市場の49.1%を占めます。南アフリカがアフリカのトウモロコシ市場の主要シェアを占めており、耕作面積の増加、GMトウモロコシの栽培承認、世界参入企業による地方に適したハイブリッド品種の入手が可能なことから、2022年には金額ベースで50.3%を占めました。

- エチオピアとナイジェリアは、この地域で最も急成長している小麦市場であり、予測期間中にCAGR 5.8%を記録すると予想されます。収益性の高い作物の栽培面積の増加と消費の拡大が、これらの国々での市場成長の原動力となっています。

- アフリカにおける栽培面積の増加と穀物消費の増加は、予測期間中にアフリカの穀物種子市場を牽引すると予測される要因です。

アフリカの穀物種子市場動向

トウモロコシはアフリカで栽培されている最大の連作作物であり、政府の支援と主要食料源としてのトウモロコシの重要性により増加しています。

- 穀物と穀類は主食作物であるため、この地域で栽培されている主要作物です。これらの作物の栽培面積は2022年に1億2,650万ヘクタールを占め、2017~2022年の間に3.2%増加しました。恵まれた気候条件、主食としての消費需要の増加、飼料産業からのトウモロコシ需要、輸出の可能性が、この地域の農業従事者がより多くの穀物を栽培する原動力となっています。

- トウモロコシはこの地域で栽培されている主要な穀物作物であり、2022年には穀物作物の栽培面積の34.0%を占めます。トウモロコシの栽培面積は2016~2022年の間に10.7%増加したが、これはトウモロコシが高い収量を生み出す能力があり、この地域の加工と飼料産業からの消費需要が大きいためです。さらに、ソルガムはこの地域の主要な主食作物のひとつです。ソルガムの栽培面積は2017~2022年にかけて2.1%増加したが、これは消費の増加と、健康上の利点からソルガムを含む雑穀作物への需要が高まっているためです。

- アフリカでは、コメの栽培面積は2016年の1,510万ヘクタールから2022年には1,600万ヘクタールに増加しました。コメはアフリカの40カ国で栽培されており、アフリカの人口の大半の主食となっています。アフリカライスセンターによると、アフリカの米生産量は前年比成長率6%で増加しており、予測期間中はさらに増加すると予想されています。この地域で栽培されている他の穀物には、小麦、大麦、オート麦、雑穀、ライ麦などがあります。改良種子が入手可能になったことで、栽培に必要な水が少なくて済むため、生産者は小麦よりも大麦を多く栽培するようになりました。したがって、家庭での消費と家畜への給餌のための穀物需要の増加が、アフリカでの穀物栽培面積を押し上げると予想されます。

病害抵抗性は、アフリカのトウモロコシと小麦の栽培において人気のある形質です。これは、この地域では昆虫と病害が作物の生産性と農業の持続可能性に大きな影響を与えるためです。

- トウモロコシはアフリカで栽培されている重要な穀物作物です。高収益作物であり、食品、飼料、その他の産業からの需要が高いです。そのため、環境破壊や生物・生物ストレスに打ち勝つための耐病性、幅広い適応性、早熟性、干ばつ耐性を備えた種子の需要が高まっている

- 2020年、国際トウモロコシ・コムギ改良センター(CIMMYT)はアフリカ地域で5年間の長期プロジェクト(2020~2025)AGG(Accelerating Genetic Gains in Maize and Wheat)を開始しました。このプロジェクトは、育種の効率と精度を向上させる革新的な方法を用いて、農業従事者のニーズに的を絞った、気候に強く、病害虫に強く、栄養価の高い品種を生産するものです。

- アフリカでは、Bayer Ag、Limagrain、Seed Co.などの企業が、トウモロコシの灰色葉斑病、トウモロコシと小麦のさび病、小麦のセプトリア葉枯病、その他のうどんこ病抵抗性品種など、幅広い品種を導入しています。

- エチオピア、エジプト、ケニアはアフリカの主要小麦生産国です。小麦では、葉さび病が深刻な収量損失を引き起こす主要な病害です。耐病性を持つ品種は収量損失を最小限に抑えます。そのため、この地域では葉さび病抵抗性品種の需要が高まると予想されています。さらに、国内需要の増加に伴い、農業従事者はより幅広い適応性形質を持ち、高タンパク・高グルテン含量を持つ小麦品種の栽培にも注力しています。

- したがって、作物を保護するための耐病性形質の開発は、将来的に種子市場を成長させ、生産者の利益を増加させるのに役立つと予測されます。

アフリカの穀物種子産業概要

アフリカの穀物種子市場はセグメント化されており、上位5社で36.52%を占めています。この市場の主要企業は、Bayer AG、Corteva Agriscience、Groupe Limagrain、Seed Co Limited、Syngenta Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 最も人気のある品種

- トウモロコシと小麦

- 育種技術

- 列作物

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非トランスジェニックハイブリッド

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- 昆虫抵抗性雑種

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 作物

- トウモロコシ

- 米

- ソルガム

- 小麦

- その他の穀物

- 生産国

- エジプト

- エチオピア

- ガーナ

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他のアフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- BASF SE

- Bayer AG

- Capstone Seeds

- Corteva Agriscience

- Groupe Limagrain

- S& W Seed Co.

- Seed Co Limited

- Syngenta Group

- Zambia Seed Company Limited(Zamseed)

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92538

The Africa Grain Seed Market size is estimated at 1.57 billion USD in 2025, and is expected to reach 1.94 billion USD by 2030, growing at a CAGR of 4.35% during the forecast period (2025-2030).

Approval of GMO seeds and increased demand for high-yielding hybrids is estimated to drive the market's growth

- Hybrid varieties dominated the market and held a share of 59.4% in 2022, whereas open-pollinated varieties held a share of 40.6%. This could be mainly attributed to the increased utilization of hybrids to increase the yield and productivity of the crops.

- In 2022, rice and wheat remained the two major crops grown in Africa using open-pollinated varieties and hybrid derivatives, accounting for 98.6% and 98.4% of the respective markets in Africa. The increased research and development of disease-resistant and high-yielding open-pollinated varieties are expected to drive the market's growth.

- Under the hybrids segment, non-transgenic hybrids accounted for 60.4% and transgenic seeds accounted for 39.6% of the region's grains and cereals market in 2022.

- Only five of the 47 countries approved the use of GMO crops, which are South Africa, Burkina Faso, Sudan, Egypt, and Nigeria. GMOs are gradually integrating into modern African agriculture. In Africa, insect-resistant transgenic hybrids accounted for 78.2% of the transgenic seed market in terms of value, and herbicide-tolerant hybrids accounted for 21.8% in 2022. South Africa dominates the African grain seed market in insect-resistant and herbicide-resistant traits. Herbicide-tolerant varieties were approved only in South Africa.

- Corn is the only grain crop cultivated in Africa with the herbicide-tolerant trait. The market value of GM herbicide-tolerant grains is estimated to record a CAGR of 2.4% during the forecast period.

- Approval of genetically modified seeds and increasing demand for high-yielding hybrids are expected to drive the market's growth.

South Africa is the largest grain seed market in Africa due to the large area of grain cultivation in the country

- In 2022, grains and cereals accounted for about 62.6% of the African row crop seed market. The primary reason for the higher market share of grains was the increase in their consumption and the increasing acreage under cultivation.

- South Africa holds the major share of Africa's grain seed market, accounting for about 34.6% of the market in 2022. This was because of the availability of new and improved seed varieties, access to the market, and an increase in the cultivation of highly profitable crops, such as corn. The market share of South Africa is projected to grow during the forecast period.

- Kenya and Ghana are the fastest-growing grain seed markets, which are anticipated to register a CAGR of 6.6% during the forecast period. Rice is the major grain crop, which is in high demand in these countries.

- Corn held the largest share of the African grain seed market, accounting for 49.1% of the market in 2022. South Africa holds the major share of the African corn market, which accounted for 50.3% by value in 2022 due to more area under cultivation, the approval of GM corn for cultivation, and the availability of hybrid varieties from global players suitable for local areas.

- Ethiopia and Nigeria are the fastest-growing wheat markets in the region, which is anticipated to record a CAGR of 5.8% during the forecast period. The increasing area under cultivation of profitable crops and the growing consumption are driving the growth of the market in these countries.

- The increasing cultivation area in Africa and the increasing consumption of grains are the factors anticipated to drive the African grain seed market during the forecast period.

Africa Grain Seed Market Trends

Corn is the largest row crop cultivated in Africa and increasing due to government support and the significance of corn as a main food source

- Grains and cereals are the major crops cultivated in the region as they are staple food crops. The area under cultivation for these crops accounted for 126.5 million hectares in 2022; there was an increase of 3.2% between 2017 and 2022. Favorable climatic conditions, higher consumption demand as a staple food, corn demand from the feed industries, and export potential drive farmers to grow more grains in the region.

- Corn is the major grain crop cultivated in the region, which accounted for 34.0% of the grain crop's area in 2022. The cultivation area of corn increased by 10.7% during 2016-2022 because of its ability to generate higher yields and greater demand for consumption from the processing and feed industries in the region. Moreover, Sorghum is one of the major staple food crops in the region. The area under cultivation of sorghum increased by 2.1% from 2017 to 2022 due to the increase in consumption and the growing demand for millet crops, including sorghum, due to their health benefits.

- In Africa, the cultivation area of rice increased from 15.1 million hectares in 2016 to 16.0 million hectares in 2022. Rice is cultivated in 40 African countries, and it is a staple food for the majority of the population in Africa. According to the Africa Rice Center, rice production in Africa is increasing at a Y-o-Y growth rate of 6%, which is anticipated to increase further during the forecast period. The other grains cultivated in the region include wheat, barley, oats, millets, and rye. The availability of improved seeds has helped growers cultivate more barley than wheat, as less water is required to cultivate. Therefore, increasing the demand for grains for home consumption and feeding livestock is anticipated to boost grain cultivation area in Africa.

Disease resistance is a popular trait in African corn and wheat cultivation due to the significant impact of insects and diseases on crop productivity and agricultural sustainability in the region

- Corn is an important grain crop cultivated in Africa. It is a high-profit crop with high demand from food, feed, and other industries. Therefore, there is an increasing demand for seeds with disease resistance, wider adaptability, early maturity, and drought tolerance to overcome environmental damage and biotic and abiotic stresses.

- In 2020, the International Maize and Wheat Improvement Center (CIMMYT) initiated a five-year long-term project (2020-2025) AGG (Accelerating Genetic Gains in Maize and Wheat) in the African region. This project uses innovative methods that improve breeding efficiency and precision to produce climate-resilient, pest- and disease-resistant, highly nutritious varieties targeted to farmers' needs.

- In Africa, companies such as Bayer Ag, Limagrain, and Seed Co. have introduced a wide range of cultivars that are resistant to grey leaf spot disease of corn, rusts in maize and wheat, Septoria leaf blight in wheat, and other powdery mildew resistant cultivars.

- Ethiopia, Egypt, and Kenya are the major wheat-producing countries in Africa. In wheat, leaf rust is the major disease that causes severe yield losses. The varieties with disease-resistant qualities minimize yield loss. Therefore, the demand for leaf rust-resistant varieties is anticipated to rise in the region. Moreover, with the growing domestic demand, farmers have also been focused on cultivating wheat cultivars with wider adaptability traits and high protein and gluten content.

- Therefore, developing disease-resistant traits to protect the crop is projected to help grow the seed market and increase the growers' profit in the future.

Africa Grain Seed Industry Overview

The Africa Grain Seed Market is fragmented, with the top five companies occupying 36.52%. The major players in this market are Bayer AG, Corteva Agriscience, Groupe Limagrain, Seed Co Limited and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Corn & Wheat

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Corn

- 5.2.2 Rice

- 5.2.3 Sorghum

- 5.2.4 Wheat

- 5.2.5 Other Grains & Cereals

- 5.3 Country

- 5.3.1 Egypt

- 5.3.2 Ethiopia

- 5.3.3 Ghana

- 5.3.4 Kenya

- 5.3.5 Nigeria

- 5.3.6 South Africa

- 5.3.7 Tanzania

- 5.3.8 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Capstone Seeds

- 6.4.5 Corteva Agriscience

- 6.4.6 Groupe Limagrain

- 6.4.7 S&W Seed Co.

- 6.4.8 Seed Co Limited

- 6.4.9 Syngenta Group

- 6.4.10 Zambia Seed Company Limited (Zamseed)

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms