|

市場調査レポート

商品コード

1693454

北米の穀物種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)North America Grain Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の穀物種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 205 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

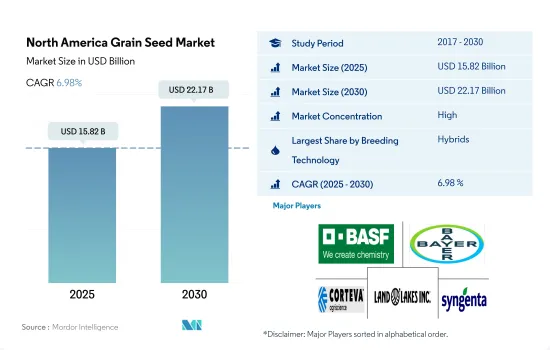

北米の穀物種子市場規模は2025年に158億2,000万米ドルと推定・予測され、2030年には221億7,000万米ドルに達し、予測期間(2025-2030年)のCAGRは6.98%で成長すると予測されます。

育種技術の進歩と高品質農産物に対する消費者の嗜好の高まりによりハイブリッドが市場を席巻

- 北米では、ハイブリッド分野が穀物種子市場を独占し、2022年には金額ベースで76.6%のシェアを占めました。ハイブリッド種子は特定の生育条件に合わせて作られるため、農家は特定の地域や環境で優れた性能を発揮する品種を選ぶことができます。

- ハイブリッドのうち、主な生産作物はトウモロコシで、2022年の穀物種子市場の約92.8%を占めています。これは、ハイブリッドトウモロコシ種子が開放受粉品種に比べて常に高い収量を生み出し、農家の生産性と収益性を向上させるためです。

- 新しい植物育種技術により、種子や植物細胞のDNAを改変することで、所望の形質を持つ新しいハイブリッド品種の開発が可能となっています。植物育種における革新は、農家が日々現場で直面する課題の解決に役立っています。これがハイブリッド種子市場の原動力となっています。

- 開放受粉種子は、より包括的な遺伝的多様性を示し、異なる消費者の嗜好にアピールできる風味、色、サイズのバリエーションを可能にします。その結果、有機栽培農家から再生農法に対する需要が高まっています。

- 小麦は、穀物・穀類部門ではトウモロコシに次いで2番目に多く栽培されている作物で、開放受粉品種を使用しています。2022年の開放受粉品種の穀物種子市場金額の40.6%を占めています。これは、開放受粉品種が高収量と地域環境への適応性を提供する幅広い形質と遺伝的多様性を提供し、小麦農家にとって価値あるものとなり得るからです。

- 開放受粉品種は収量が高く、同じ生産量を得るのに必要な生産面積が少ないため、ハイブリッド種子の需要が増加しており、これが同市場におけるハイブリッド種子の成長を促進すると予想されます。

米国がこの地域の穀物種子市場を独占、トウモロコシと小麦が主要作物

- 2022年には、穀物・穀類が北米の種子市場の57.6%を占めました。2022年の同地域における穀物・穀類の栽培面積は8,270万ヘクタールで、加工施設の増加や、穀物・穀類が食生活の主食であることから自給自足の導入を推進する政府により、2021年比で1.3%増加しました。

- 米国は世界第2位の穀物・穀類の生産国で、トウモロコシと小麦が主な貢献国です。米国のトウモロコシ種子セグメントは、2022年の米国種子市場全体の53.9%を占めています。

- 小麦、オート麦、大麦はカナダで栽培されている主な穀物で、2022年には1,400万ヘクタール以上を占め、4,500万トン以上の穀物を生産します。カナダは第5位の小麦生産国で、消費に必要な量以上の小麦を生産しています。カナダは小麦を80カ国以上に輸出しています。

- 2022年、メキシコの穀物種子市場は9億6,100万米ドルの市場価値を占め、国際商品価格の高騰と小規模生産者に基礎穀物の生産を奨励する政府プログラムにより、2019年比で25.4%増加しました。これらの要因は、メキシコの穀物総生産量、特に米と小麦の生産量を押し上げています。

- その他北米地域の穀物・穀類種子市場は、2022年の穀物・穀類種子市場額の3.3%を占める。2022年の総栽培面積は230万ヘクタールで、キューバやコスタリカなどの主要生産国における熱帯暴風雨やサイクロンの影響で2017年から3.8%減少しています。

- 政府支援の増加と継続的な主食需要は、CAGR 6.8%で、予測期間中に同地域の種子市場を押し上げると予測されます。

北米の穀物種子市場の動向

北米では加工産業からの需要が増加しているため、トウモロコシを主体とする穀物・穀類地域が拡大

- 北米では、2022年の穀物・穀類分野の耕作面積は8,270万haで、主食としての穀物需要が堅調なことから前年比1.3%増加しました。2022年には、穀物・穀類の中でトウモロコシが4,560万ヘクタールで栽培されています。これは主に、この地域の他の作物と比べて収量が高く、トウモロコシの栽培に適した土壌と農業気候条件を備えているためです。カナダを除き、この地域の主要国ではトウモロコシの生産地が大半を占めています。これは、トウモロコシが家畜飼料、エタノール生産、主食消費、バイオ燃料生産など多くの用途があり、それがこの作物の国内需要を牽引しているからです。

- 小麦はこの地域で2番目に多く栽培されている作物で、2022年には2,500万haで栽培されています。ノースダコタ州は小麦生産量第1位で、2022年には約2億9,990万ブッシェルを生産します。さらに、この地域最大の国である米国は、2022年に約5,550万haの穀物・穀類を生産しています。主な穀物生産州は、カンザス、ノースダコタ、モンタナ、ワシントン、オクラホマ、アイダホ、テキサス、オレゴン、ミネソタ、サウスダコタです。

- カナダでは、穀物・穀類の栽培面積は2022年から2017年の間に11.2%増加し、小麦と大麦の栽培面積が増加しました。2022年の穀物・穀類生産面積の60.8%を小麦が占める。小麦が同国で消費される主食であることから、需要が増加し、農家の嗜好がトウモロコシや他の穀物から小麦にシフトしたためです。このように、この地域では加工産業からの穀物や穀類作物に対する需要が増加しており、市場成長の原動力となっています。

耐病性形質と幅広い適応性形質の利用の増加が、この地域の穀物種子市場の成長を促進しています。

- 北米ではコメとトウモロコシが最もハイブリッド化された作物であり、投入コストを削減し、干ばつなどの厳しい気候条件下でも高収量を実現するさまざまな形質に対する大きな需要を記録しています。

- 耐病性形質は、この地域の生産者が最も求めているトウモロコシの形質です。これらの形質は、トルコギキョウ、白斑病、灰色葉斑病、さび病、ゴス萎凋病、炭疽病茎腐敗病から作物を守るために使用されています。昆虫抵抗性や幅広い適応性といった他の形質も、トウモロコシ作物に感染する主な昆虫である、カツオブシムシ、アワノメイガ、ホソクビハムシなどのガ類、次いで、オフシーズンに生育し、土壌条件が異なる、グラブやゾウムシなどの甲虫類から保護するために、高い需要があります。例えば、ウィンフィールドやデカルブといった製品ブランドには、こうしたトウモロコシの形質が含まれています。

- コメは北米、特に米国で最も多く生産され、輸出されている作物のひとつです。作物の収量を30%~40%増やし、生産量を増やすことで高い利益を得るため、生産者は、病害抵抗性、生物的ストレス耐性、幅広い適応性、干ばつ耐性などの形質を持つ稲の種子品種を求めています。バイエルAGのArizeのような種子会社が提供する形質は、細菌性病害への抵抗性、早熟性、生物的ストレス下での大量生産を実現します。

- トウモロコシとコメの消費量の増加、ハイブリッドの利用可能性の増加、病気に対する耐性と収量の増加に対する高い需要などの要因が、この地域における市場の成長を促進すると予想されます。

北米の穀物種子産業の概要

北米の穀物種子市場はかなり統合されており、上位5社で75.62%を占めています。この市場の主要企業は以下の通りです。 BASF SE, Bayer AG, Corteva Agriscience, Land O'Lakes Inc. and Syngenta Group(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 最も人気のある品種

- コメとトウモロコシ

- 育種技術

- 列作物

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非遺伝子組み換え雑種

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- 昆虫抵抗性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 作物

- トウモロコシ

- 米

- ソルガム

- 小麦

- その他の穀物

- 生産国

- カナダ

- メキシコ

- 米国

- その他北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- BASF SE

- Bayer AG

- Corteva Agriscience

- DLF

- Groupe Limagrain

- KWS SAAT SE & Co. KGaA

- Land O'Lakes Inc.

- S&W Seed Co.

- Syngenta Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92516

The North America Grain Seed Market size is estimated at 15.82 billion USD in 2025, and is expected to reach 22.17 billion USD by 2030, growing at a CAGR of 6.98% during the forecast period (2025-2030).

Hybrids dominate the market due to advancements in breeding technologies and growing consumer preference for quality produce

- In North America, the hybrid segment dominated the grain seed market, with a share of 76.6% in terms of value in 2022. Hybrids are tailored to specific growing conditions, allowing farmers to choose varieties that perform well in their particular region or environment.

- Among hybrids, the major crop produced is corn, which accounted for about 92.8% of the grain seed market in 2022. This is because hybrid corn seeds consistently produce higher yields compared to open-pollinated varieties, resulting in increased productivity and profitability for farmers.

- New plant breeding techniques are allowing the development of new hybrid varieties with desired traits by modifying the DNA of the seeds and plant cells. Innovations in plant breeding are helping address the challenges farmers face in the field every day. This, in turn, drives the hybrid seed market.

- Open-pollinated seeds exhibit a more comprehensive range of genetic diversity, allowing for flavor, color, and size variations that can appeal to different consumer preferences. As a result, there is a growing demand from organic growers for regenerative agricultural practices.

- Wheat is the second most cultivated crop in the grains and cereals segment, using open-pollinated varieties after corn. It accounted for 40.6% of the grain seed market value of open-pollinated varieties in 2022. This is because open-pollinated varieties offer a wider range of traits and genetic diversity that offer high yield and adaptability to the local environment, which can be valuable for wheat farmers.

- There is an increasing demand for hybrid seeds due to the high yield and less production area required for the same output by open-pollinated varieties, which is expected to drive the growth of hybrid seeds in the market.

The United States dominated the grain seed market in the region, with corn and wheat being major crops

- In 2022, grains and cereals accounted for 57.6% of the North American seed market. The total acreage under grains and cereals in the region in 2022 was 82.7 million hectares, which increased by 1.3% compared to 2021 due to an increase in the number of processing facilities and governments pushing the adoption of self-sufficiency as grains and cereals are a staple food in the diet.

- The United States is the second-largest producer of grains and cereals globally, with corn and wheat being the major contributors. The US corn seed segment accounted for 53.9% of the overall US seed market in 2022.

- Wheat, oats, and barley are the major cereals cultivated in Canada, accounting for more than 14 million hectares in 2022 and producing more than 45 million metric ton of grains. Canada is the fifth-largest producer of wheat, producing more than what is required for consumption. Canada exports wheat to more than 80 countries.

- In 2022, the Mexican grain seed market accounted for a market value of USD 961 million, which increased by 25.4% compared to 2019 due to high international commodity prices and government programs incentivizing small growers to produce basic grains. These factors are boosting Mexico's total grain production, particularly of rice and wheat.

- The grains and cereals seed market of Rest of North America accounted for 3.3% of the region's grains and cereals seed market value in 2022. The total acreage in 2022 was 2.3 million hectares, which has decreased by 3.8% since 2017 due to tropical storms and cyclones in the major producing countries, such as Cuba and Costa Rica.

- The increasing government support and continuous demand for staple food are estimated to boost the seed market in the region during the forecast period, with a CAGR of 6.8%.

North America Grain Seed Market Trends

Corn-dominated grains and cereals area in the North America as there is an increased demand from the processing industries

- In North America, the area under cultivation of grains and cereals segment in 2022 accounted for 82.7 million ha, which increased by 1.3% from the previous year due to solid demand for cereals as a staple food. Corn was cultivated under 45.6 million ha in 2022 among all the grains and cereals. It is mainly attributed to high yields compared with other crops in the region and has suitable soil and agroclimatic conditions for the cultivation of corn. Except in Canada, the region's major countries have the majority of land under corn production because corn has many applications, such as animal feed, ethanol production, staple consumption, and biofuel production, which is driving the demand for the crop in the country.

- Wheat was the second-largest crop grown in the region, cultivated under 25.0 million ha in 2022. North Dakota was ranked the first leading wheat production state, with about 299.9 million bushels produced in 2022. Furthermore, Being the largest country in the region, the United States had around 55.5 million ha under the production of grains and cereals in 2022. The major grains-producing states are Kansas, North Dakota, Montana, Washington, Oklahoma, Idaho, Texas, Oregon, Minnesota, and South Dakota.

- In Canada, the area under grains and cereals increased by 11.2% between 2022 and 2017, with the increase under wheat and barley. Wheat accounted for 60.8% of the grains and cereals production area in 2022. The acreage increased due to the rise in demand and the shift in farmers' preference from corn and other cereals to wheat, as wheat is the primary staple consumed in the country. Thus, increased demand for grains and cereal crops in the region from processing industries drives market growth.

Increasing usage of disease resistant and wider adaptability traits are driving the growth of grain seed market in the region

- Rice and corn are the most hybridized crops in North America, registering significant demand for different traits that reduce the cost of inputs and have a high yield in severe climatic conditions such as drought.

- Disease-resistant traits are the most demanded corn traits by the growers in the region. These traits are being used by them to protect the crop from turcicum, white spot diseases, gray leaf spot, common rust, goss wilt, and Anthracnose stalk rot diseases. Other traits such as insect resistance and wider adaptability also have a high demand to protect from major insects infecting maize crops are moths, such as cutworms, armyworms, and borers, followed by beetles such as grubs and weevils, which grow in the off-season and different soil conditions. For instance, product brands such as Winfield and Dekalb contain these corn traits.

- Rice is one of the largest produced and exported crops from North America, particularly the United States. To earn high profit by increasing the yield of the crop by 30%-40% and higher production, the growers are demanding rice seed varieties with traits such as disease resistance, abiotic stress tolerance, wider adaptability, and drought tolerance. The traits offered by seed companies such as Bayer AG's Arize provide resistance to bacterial diseases, early maturity, and produce high quantities during abiotic stress.

- Factors such as the increased consumption of corn and rice, an increase in the availability of hybrids, and high demand for resistance to diseases and increasing yield are expected to drive the market's growth in the region.

North America Grain Seed Industry Overview

The North America Grain Seed Market is fairly consolidated, with the top five companies occupying 75.62%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Land O'Lakes Inc. and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Rice & Corn

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.1.2.3 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Corn

- 5.2.2 Rice

- 5.2.3 Sorghum

- 5.2.4 Wheat

- 5.2.5 Other Grains & Cereals

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 DLF

- 6.4.6 Groupe Limagrain

- 6.4.7 KWS SAAT SE & Co. KGaA

- 6.4.8 Land O'Lakes Inc.

- 6.4.9 S&W Seed Co.

- 6.4.10 Syngenta Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms