|

市場調査レポート

商品コード

1693403

マレーシアのシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Malaysia Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| マレーシアのシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 156 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

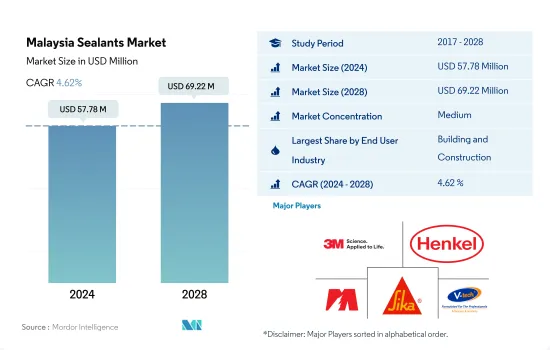

マレーシアのシーラント市場規模は2024年に5,778万米ドルと推計され、2028年には6,922万米ドルに達し、市場推計・予測期間(2024-2028年)のCAGRは4.62%で成長すると予測されます。

マレーシアのアウトソーシング先および医療機器製造ハブとしての台頭がシーラント需要を大幅に押し上げる

- マレーシアのシーラント市場は主に建設業界が牽引しており、防水、耐候性シーリング、ひび割れシーリング、目地シーリングなど、建築・建設活動におけるシーラントの用途が多様であるため、その他のエンドユーザー産業セグメントがそれに続いています。建築用シーラントは、耐用年数が長く、様々な基材への塗布が容易なように設計されています。建設産業はマレーシア経済において重要な役割を果たしています。しかし、2020年にはパンデミックによる規制と原材料の不足のために建設活動が減少し、2021年には回復したため、国全体のシーラント需要を押し上げています。

- シーラントはヘルスケア産業でかなりの用途があり、主に医療機器部品の組み立てとシールに使用されています。医療グレードのシーラントは、ガラス、金属、プラスチック、塗装面など、さまざまな基材に独自の適用性を持っており、耐候性、耐熱性、老化防止などの重要な機能がシーラントの需要を押し上げる可能性が高いです。マレーシアは、東南アジア地域のメーカーにとって、アウトソーシング先や医療機器製造のハブとして台頭してきています。このため、予測期間中、同国のシーラント需要を押し上げるとみられます。

- その他のエンドユーザー産業分野は、電子・電気機器製造業におけるポッティングや保護材などの多様な用途により、マレーシアのシーラント市場で一定のシェアを獲得する可能性が高いです。シーラントはセンサーやケーブルなどの密封に使用されます。さらに、eコマース活動の急成長とコンシューマーエレクトロニクス分野の強力な市場ポジショニングが、マレーシアのシーラント市場を推進すると思われます。

マレーシアのシーラント市場動向

民間および産業界からの投資と今後のメガ建設プロジェクトが業界規模を拡大させる

- マレーシアの建設業界は、2022年から2028年の予測期間中に約3.37%のCAGRで推移すると予測されています。2019年、マレーシアの建設生産高は約1,463億7,000万MYRとなり、2018年からわずかな伸びを示しました。2019年のマレーシアの建設セクターは、負債額をカバーするためにいくつかのプロジェクトが停滞したため、成長が鈍化しました。いくつかのメガ建設プロジェクトの停止と売れ残り住宅在庫の増加により、2019年の建設業界はほぼ停滞したままでした。

- 2020年、マレーシアの建設部門は、土木、非住宅、住宅のマイナス成長により13.9%縮小しました。マレーシアの建設活動は2021年12月期に前年同期比12.9%縮小しました。2021年第3四半期と比較すると、住宅が減少し、非住宅と土木が減少しました。2021年までに、同国の建設生産高は5%減少しました。

- マレーシアは、民間建設と産業建設に多額の投資を行い、推進しています。2022年の民間・産業建設予測によると、住宅部門は2021年に6.08%増の226億2,800万マレーシア・リンギットを記録し、供給過剰の懸念が長引く中、2022年上半期には1.67%減少すると予想されました。予測期間中、全国で建設開発が拡大します。

電気自動車需要の拡大が同国の自動車産業に影響を与える

- マレーシアは多国籍自動車メーカーにとって魅力的な拠点であり続けています。ホンダ、トヨタ、日産、メルセデス・ベンツ、BMWは、増大する顧客需要に対応するためにマレーシアに進出している世界の自動車企業のひとつです。自動車産業はマレーシアの産業部門において重要な位置を占めており、GDPの4%以上を占めているほか、ASEAN第3位の自動車市場でもあります。マレーシアには現在、乗用車、商用車、オートバイ、スクーター、自動車部品・コンポーネントの製造・組立工場が28カ所あります。

- この産業が、エンジニアリング、補助部門、支援部門の成長に貢献していることは間違いないです。また、技能開発や技術・エンジニアリング能力の向上にも役立っています。マレーシアの自動車産業は、デジタル化と新しいビジネスモデルの出現という世界の動向と無縁ではないと思われます。2019年の同国の自動車生産台数は約57万1,632台であったが、2020年には48万5,186台に激減し、COVID-19の流行により15%減少しました。このため、2019年から2021年にかけての自動車生産台数の変動は約-16%であったのに対し、2020年から2021年にかけては-1%を記録しました。

- 電気自動車(EV)は、国内の自動車産業のロードマップにおいて、自動車の電力システムの将来にとって重要な技術として認識されています。EVはつい最近、マレーシアで大きな影響力を持つようになりました。しかし、マレーシアにはEVのインフラがなく、化石燃料への依存度が高いことが大きな障害となっています。

マレーシアのシーラント産業概要

マレーシアのシーラント市場は適度に統合されており、上位5社で45.69%を占めています。この市場の主要企業は以下の通り。 3M, Henkel AG & Co. KGaA, Mohm Chemical Sdn. Bhd., Sika AG and VITAL TECHNICAL SDN BHD(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 規制の枠組み

- マレーシア

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- ヘルスケア

- その他のエンドユーザー産業

- 樹脂

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他の樹脂

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- 3M

- Arkema Group

- Dow

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc.

- Mohm Chemical Sdn. Bhd.

- Sika AG

- Soudal Holding N.V.

- VITAL TECHNICAL SDN BHD

- Wacker Chemie AG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーリング剤産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、阻害要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92459

The Malaysia Sealants Market size is estimated at 57.78 million USD in 2024, and is expected to reach 69.22 million USD by 2028, growing at a CAGR of 4.62% during the forecast period (2024-2028).

Malaysia's growing emergence as an outsourcing destination and medical device manufacturing hub to substantially boost the sealants demand

- The Malaysian sealants market is primarily driven by the construction industry, followed by the other end-user industries segment due to the diverse applications of sealants in building and construction activities, such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing. Construction sealants are designed for longevity and ease of application on different substrates. The construction industry plays a vital role in the Malaysian economy. However, construction activities decreased in 2020 due to the COVID-19 pandemic-induced restrictions and scarcity of raw materials, which was restored in 2021, thus, boosting the sealants demand across the country.

- Sealants have considerable applications in the healthcare industry and are primarily used for assembling and sealing medical device parts. Medical-grade sealants have unique applicability to various substrates, such as glass, metal, plastic, painted surfaces, etc., and significant features such as weather-proofing, heat resistance, and anti-aging are likely to boost the demand for sealants. Malaysia is emerging as an outsourcing destination and medical device manufacturing hub for manufacturers in the Southeast Asian region. This, in turn, is expected to boost the sealants demand in the country over the forecast period.

- The other end-user industries segment is likely to obtain a decent share in the Malaysian sealants market owing to the diverse applications in the electronics and electrical equipment manufacturing industry for potting and protecting materials. They are used for sealing sensors and cables, etc. Moreover, the rapid growth of e-commerce activities, along with the strong market positioning of the consumer electronics segment, is likely to propel the Malaysian sealants market.

Malaysia Sealants Market Trends

Private and industrial investments along with the upcoming mega-construction projects will augment the industry size

- The Malaysian construction industry is expected to record a CAGR of about 3.37% during the forecast period from 2022 to 2028. In 2019, the construction output in Malaysia stood at approximately MYR 146.37 billion, exhibiting a slight growth from 2018. Malaysia's construction sector grew slower in 2019, as a few projects were stalled to cover the debt values. Owing to a halt in several mega-construction projects and an increasing inventory of unsold housing stocks, the construction industry remained almost stagnant in 2019.

- In 2020, the Malaysian construction sector contracted by 13.9% due to negative growth in civil engineering, non-residential, and residential buildings. Malaysia's construction activity contracted 12.9% Y-o-Y in the December quarter of 2021. Decreasing numbers were seen in residential buildings compared to the third quarter of 2021, with a decrease in non-residential buildings and civil engineering. By 2021, the construction output fell by 5% in the country.

- Malaysia promotes and makes significant investments in private and industrial construction. As per the 2022 construction forecast for private and industrial construction, the residential sector was expected to record a 6.08% increase to MYR 22,628 million in 2021 and a decline by 1.67% in the first half of 2022 as concerns over the supply overhang linger. The growing construction developments across the country over the forecast period.

Growing demand for electric vehicles will influence the country's automotive industry

- Malaysia remains an appealing base for multinational automakers. Honda, Toyota, Nissan, Mercedes-Benz, and BMW are among the global automobile corporations that have established operations in the country to capitalize on growing customer demand. The industry is a crucial part of the country's industrial sector, contributing above 4% of its GDP and remaining the third-largest automotive market in ASEAN. Malaysia currently has 28 manufacturing and assembly plants for passenger vehicles, commercial vehicles, motorcycles, and scooters, as well as automotive parts and components.

- The industry has undoubtedly aided the growth of engineering, auxiliary, and supporting sectors. It also helps with skill development and the advancement of technology and engineering capabilities. The automotive industry in Malaysia will not be immune to the global trend of digitalization and the advent of new business models. In 2019, the country produced about 5,71,632 units of vehicles, which drastically reduced to 4,85,186 units in 2020, with a 15% decline due to the COVID-19 pandemic. Due to this, the variation in automotive production between 2019 and 2021 was about -16%, whereas it was recorded at -1% between 2020 and 2021.

- The electric vehicle (EV) is recognized as a critical technology for the future of automotive power systems in the country's automotive industry's roadmaps. EVs have just recently emerged as a significant influence in Malaysia. However, in Malaysia, the absence of EV infrastructure and the country's heavy reliance on fossil fuels creates a considerable obstacle.

Malaysia Sealants Industry Overview

The Malaysia Sealants Market is moderately consolidated, with the top five companies occupying 45.69%. The major players in this market are 3M, Henkel AG & Co. KGaA, Mohm Chemical Sdn. Bhd., Sika AG and VITAL TECHNICAL SDN BHD (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Malaysia

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Dow

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Illinois Tool Works Inc.

- 6.4.6 Mohm Chemical Sdn. Bhd.

- 6.4.7 Sika AG

- 6.4.8 Soudal Holding N.V.

- 6.4.9 VITAL TECHNICAL SDN BHD

- 6.4.10 Wacker Chemie AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms